Some highlights from NIIT Annual Report FY22:

CLG EBITDA grew 68% YoY to Rs. 2,989 million. The EBITDA margin was 26%, up 508 basis points YoY. Growth was driven by ramp-up by new customer addition and increase in wallet-share from existing customers despite spend levels on training remain at lower levels during the year. Investments in sales and marketing and new capabilities over the last few years have resulted in significant recovery and growth over the last two years, despite the continuing impact of the pandemic. During the year, the business accelerated new customer acquisition with the addition of 16 new Managed Training Services (MTS) customers, secured 4 renewals and expanded 6 contracts with existing customers. The business ended the year with 66 MTS customers, as compared to 58 at the end of the previous year. As of March 31, 2022, the Revenue Visibility stood at USD 328 million, versus 287 million at the end of FY21.The company has maintained a record of 100% renewals over the last two years. SNC showed smart recovery during the year due to strong actions by the Company and pickup in hiring by the IT and Banking sectors. This recovery was led by NIIT’s flagship offerings StackRoute and TPaaS. Margins were back in black for the year despite ramp-up in investments for growth.

India has over 38 million students enrolled in higher education, the number of college graduates entering the work-force is second highest in the world. With over 5 million people employed by the IT/ITES industry and a similar number in BFSI, college students, fresh graduates, and working professionals in India represent a large untapped opportunity.

The process for the demerger is underway and expected to be completed in H1 of FY24.

Global companies are increasing the use of technology, especially around augmented reality (AR) and virtual reality (VR), to drive L&D transformation. NIIT is taking the lead in helping companies in this area.

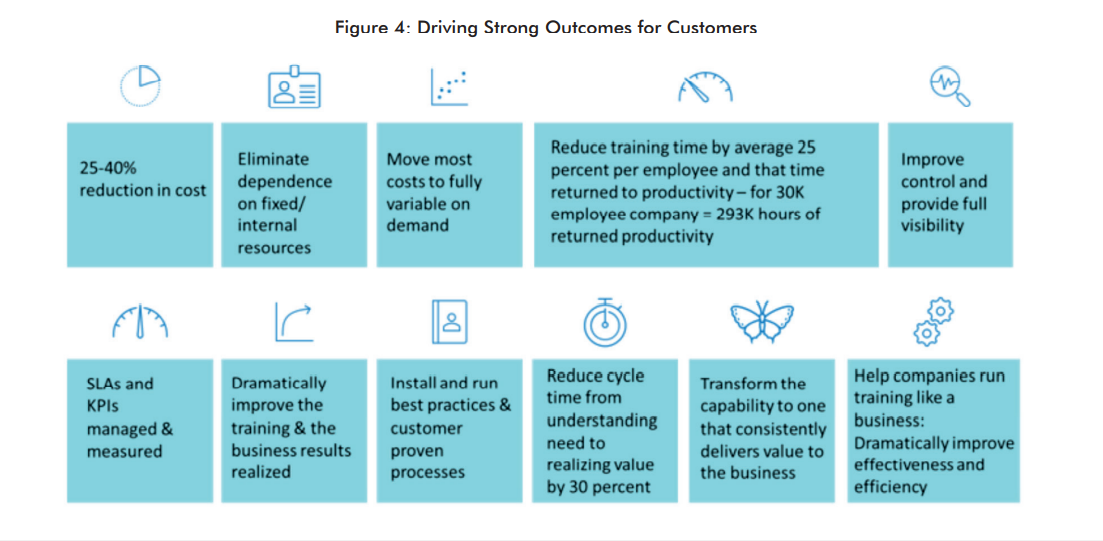

NIIT’s Corporate Learning Business is focused on the

following sectors:

• Technology & Telecom

• Energy & Commodities

• Life Sciences

• Banking, Financial Services, and Insurance

• Aerospace

• Higher Education (Market Entry)

Companies in the selected sectors are amongst the highest consumers of training in terms of amount spent on training per employee per annum

Even with a Gross Enrollment Ratio in higher education of 27.1%, India has over 38 million learners enrolled in over 40,000 colleges and 1,000+ universities. The enrollment is expected to cross 50 million by the assessment year 2025 (AY25). During the year, the IT/ITES industry witnessed strong hiring with a net addition of 445 thousand taking the total employment to 5.1 million. Banks witnessed a strong hiring demand, with over 100K employees added to the workforce in FY22. Banks in India have close to 1.5 million employees, with similar numbers in the Insurance and other Financial Services industries. Together, they represent a multi-billion market for technical and professional skills training per annum.

StackRoute has now been adopted by several corporate customers to develop their top talent, including a leading global systems integrator and 2 of the top 5 IT services companies in India. StackRoute has achieved industryleading completion rates (over 10x of the industry average) and strong outcomes for its learners, resulting in improved recognition from employers and increased bill rates.

StackRoute and TPaaS grew 137% YoY in FY22 and contributed 41% to the SNC revenue. The average remuneration level of NIIT’s graduates from its new-age digital programs has been more than twice that of college graduates who get placed directly from college campuses. ( It’s true you can check it from LinkedIn NIIT graduates get 5lakh p.a where Average package of top 5 five IT companies is in the range of 3.2 lakhs to 4 lakhs for mid tier cities)

99% growth YoY in the SNC business and 35% YoY growth in the CLG business. Excluding the acquisition of RPS Consulting, SNC grew 51% YoY and overall revenue grew 37% YoY.

The top 10 customers contributed about 61% of the CLG revenue in FY22, compared to 59% last year. The Company has maintained a healthy contract renewal rate and strong velocity of adding new customers despite the pandemic. Also, the mix of revenue from the different geographies, sectors and diversified offerings ensures that the Company is well-positioned to manage a slowdown in a particular sector or in a specific geography.