Yeah correct currently companies are no longer seeing corporate training as discretionary expense, CEO highlighted the same in Q3 CC they are focusing on those verticals where there is some type of mandatory training, regulations or rate of change in technology is faster

2 Likes

Since B2G is now zero, will there be further incremental reduction in DSOs even from current 54 days or will it be more stable now?

Have they given the DSOs in CLG vs SNC anywhere?

Though this business is out of my circle of competence ( as I am a doctor), my two cents

All the things look about CLG are great, but I am seriously skeptical about the Long Term Growth when companies start using AI instead of the human force for the software related products. So what’s the need of training in such scenarios.

Yes. It may be in distant future just like the driverless cars. But it surely will HAPPEN.

Means just for info, recently EU allowed x-ray chest reporting by AI.

Means , I fell to see the LONG runway in this training business.

Please share your thoughts.

Dr. Vikas

In the long term, all of us are dead. There are no business which are disruption proof

Only question is whether business disrupts itself or gets disrupted

The link you have shared is unrelated to niit business model

In long term, doctors would be automated with ai. Driving. Perhaps coding as well

That long term may very well occur after we are dead.

So as i was saying, in the long term, all of us are dead. ![]()

What we need to think about is disruption in next 3-5 years. There are none for CLG CURRENTLY

Regarding DSO, they have indicated that snc has lower DSO which makes sense generally exports have higher DSO. But imo DSO should not be looked at alone. We have to see DSO in conjunction with overall working capital & fixed assets. That is where clg shines. 73% ex cash roce is unique (very hard to find business with such high roce)

We will probably get to know DSO after the demerger

Rwgardi why demerge X vs Y. Imo that is not a significant business decision which needs evaluation by investors. It might be like evaluating whether promoter is left handed or right handed and using that to predict

Reason that clg is doignnwell is because learning & development has huge outsourcing runway. Only 20% of fortune 500 do l&d outsourcing and even there, there is room to grow. In one of the earlier annual report they mentioned that only 4-5% of overall l&d spends are outsourced

Interestingly in covid times l&d spends went down but niit clg growth accelerated which shows increasing market share

14 Likes

Absolutely true Sahil.

That’s the thing with direct stock investing. Its not only probabilistic but also very individualistic.

After reading so many books on investing, nowadays I am in search for a 5-bagger at least in 10 years ( 100 baggers for retail investors looks very difficult as we can never know the management and can’t do the actual scuttlebutt )

This is one of the initial criteria that I use while stock screening. Means can the business become at least 5 x from the current level.

My personal thinking is this business may not become a 5 bagger from this level.

Again I may be proven wrong as Market is Supreme.

Regards,

Dr. Vikas

1 Like

Definitely a personal decision

25-30% growth would double money in 3 years. That is visibility i have

Don’t have 10 year visibility into my own life. Let alone investee companies.

6 Likes

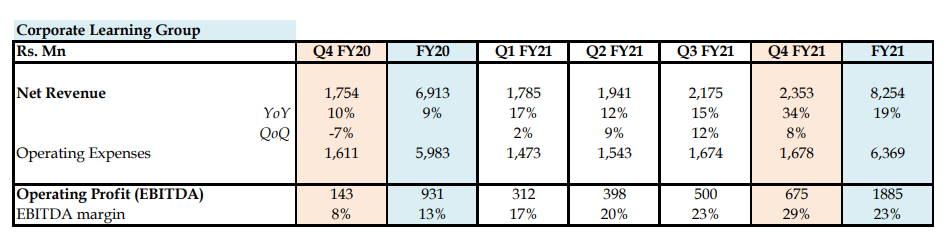

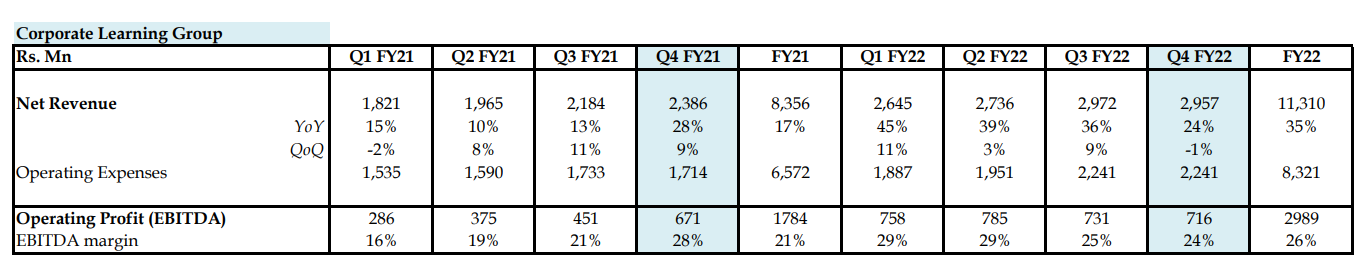

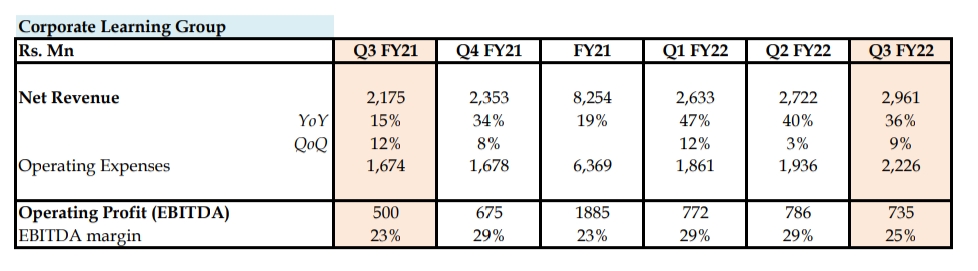

Q4 and FY22 numbers are out

One question: why is ‘reserves & surplus’ lower YoY when PAT is positive? In ‘statement of changes in equity’, isn’t change in reserves supposed to match (PAT-dividend)?

1 Like

NIIT Q4FY22 Conference Call Notes

Q4 is a Seasonally low quarter for both CLG and SNC

CLG -

Investing disproportionately in sales and marketing to get into new markets to achieve higher market access

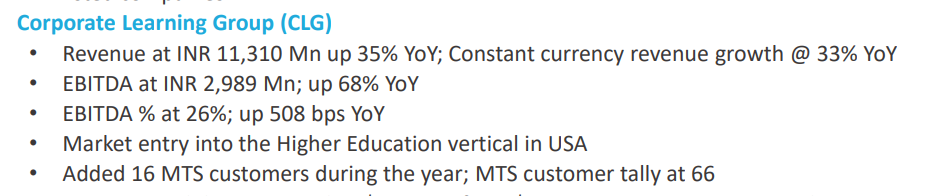

16 MTS customers added in FY22

Revenue visibility at $328 Million (2x sales)

Entered Higher Education vertical in USA.

Strong traction with 2 large Public Universities in USA.

Expects this vertical to be a material contributor in FY24.

Partial Travel has resumed and costs already being incurred, going to increase as we go ahead.

3 new MTS customers added in Life Sciences segment.

1 of which is in Bio Technology manufacturing segment.

2 Existing contracts expanded.

1st with Large Technology company.

2nd with Large Global GSI (Global systems integrator)

100% renewal track record maintained as all contracts that came up in Q4 were renewed.

66 MTS customers at the end of FY22

Customer spend that lowered in covid is still at lower levels and has stabilized.

Growth has majorly come from new wins, new capabilities added and proactive sales and marketing investments

Guidance of 20% Growth and 20% EBITDA margin going ahead

Despite current news flow, confident of Growth

5% QoQ growth expected in CLG in 1st quarter itself

SNC -

Sees a multi year growth cycle in demand for talent due to digital transformation.

Claims NIIT trained 10% of the Fresh IT graduates who went into the indian IT industry.

DSO at 48 days vs 57 days in Q3 vs 55 days in FY22.

3104 headcount (up 10% QoQ)

Corporate Training a $400 Billion market

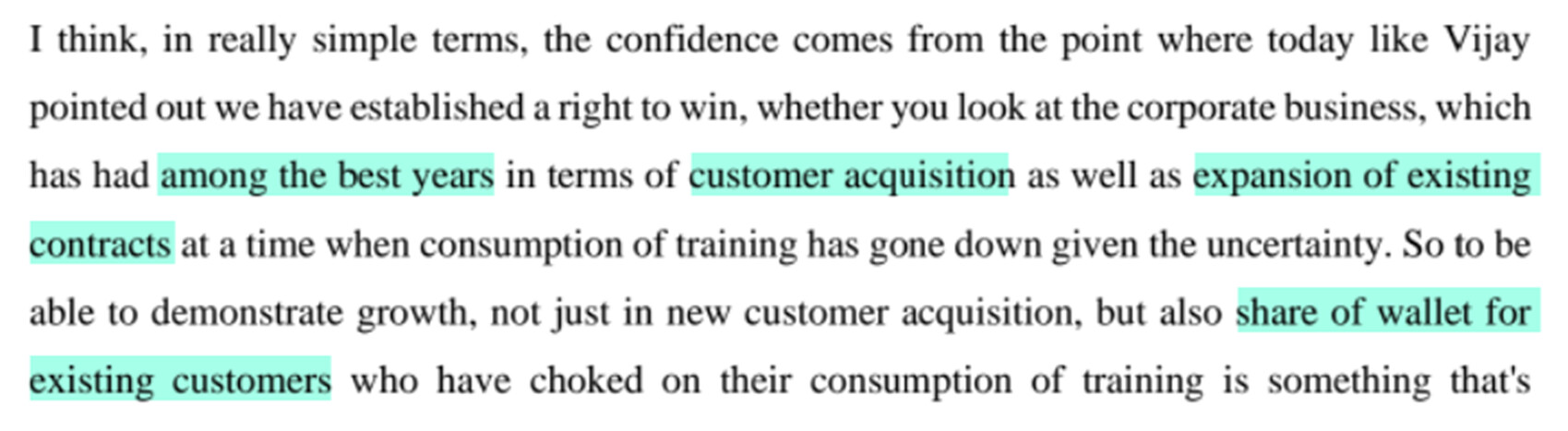

Established Right to Win.

SNC a $15-20 Billion Market

Demerger on track

SNC 50% growth expected in FY23

Profitability would be break even or small profit in FY23.

Organic growth of 53% in FY22 (excluding RPS)

Life sciences 15% of CLG business now.

Guidance of 20% EBITDA margin vs 24% in FY22 on account of -

- Higher people costs

- Resumption of travel costs and premises cost

- Disproportionate Investments in sales and marketing.

Recession compliments outsourcing in the long run as training is not core biz for organizations so they look to cut costs by outsourcing.

Short term might see some headwinds due to the environment.

But Long Term sees increased outsourcing.

Valuation of 2 business, decided by our shareholders

Real estate will remain with NIIT Ltd (SNC)

School buisness - No further investments just honouring contracts that were in place till the tenure.

High teens to 20% margin expected in snc over time after 4-5 years but would like to achieve scale and growth before focusing on profits.

In short term breakeven or along those lines.

Employee expenses down as provision of gratituity and leaves in accordance with latest interest rates (Annual Activity)

In Q4 started in person training again and expected to accelerate going forward.

Expected to come back to pre pandemic levels.

Still sticking to the 3x guidance in CLG.

But in cognisance of market environment has kept 20% growth guidance.

My concerns -

-

Employee costs are down QoQ while headcount is up 10% QoQ. Can anyone explain the provision and gratuity accounting that would cause such a deviation in costs?

-

They say we added 3 MTS customers but in Q3 MTS Count was at 65 vs 66 now.

-

In person training costs and travel costs would be a downer for margins, hope the 20% margin guidance is enough to absorb it.

-

Segregation of common assets like real estate between CLG and SNC is a concern. They say we will give real estate to SNC but they also said some properties are also shared by CLG and SNC both. So how will finances work in this case?

-

SNC faces serious competition from VC/PE funded startups like Scaler, Newton school, Pesto, UpGrad, Coding Ninjas etc. And I see no differentiated offering to say NIIT could win in this space.

Have you accounted for FY22 Buyback expense of 237 cr + subsequent tax on it of 23%?

7 Likes

Thanks for the summary.

I also have similar concern regarding Point 2 you mentioned. I have also mailed the IR team, will update if get an answer.

For FY21, they had 58 MTS Clients and this year finished with 66 Clients which makes 8 new addition (considering 0 churn as they mentioned). Similar trend has also happened historically. Net Addition is usually lower than what they mentioned as added.

(One possible reason could be that they are expanding the existing contract for subsidiaries and considering them as new additions while on total level they are considering it as one entity - This could also explain the dramatic increase of Revenue per Client this year)

If other members have any insight on this, kindly share.

This is already known but I believe market can punish the stock for at-least next few quarters. I believe 20% is sustainable. Historically, Travel Costs are usually ~5% of sales for NIIT which makes adjusted CLG EBITDA margins for this year ~21%.

Putting the higher education segment under CLG was bit of a surprise. I was presuming they are entering this through StackRoute US, which is providing content for Ohio University. We’ll have to see margins for this business.

3 Likes

Can you please share your working for this estimation? Would be very helpful

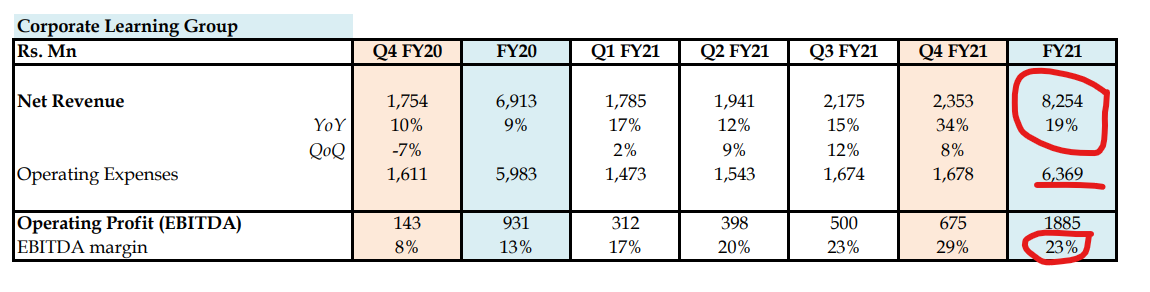

There was around 10 Cr discrepancy in CLG revenue of FY21 (earlier reported as INR 8254 Mn)…

(https://www.niit.com/authoring/Documents/FinancialResults/NIIT%20Web%20Data%20Sheet%20Q4%20FY21.pdf)

…but now shown as 8356

(https://www.niit.com/authoring/Documents/FinancialResults/NIIT%20Web%20Data%20Sheet%20Q4%20FY22.pdf)

Any idea on reason for this difference?

2 Likes

I really think that this is a good opportunity to add. Very rarely you get business which throw out a good amount of cash at these levels. Q4 is always a weak Qtr and this stock price reduction is illogical. Probably due to low float things look exaggerated.

Not just in niit most companies you can find these discrepancies this happens because after some time we realise that some revenue might have been underbooked or overbooked (returned sales, wrong selling price )

Government of India often revised it’s final figures years later for GDP, exports what not.

2 Likes

Excellent observation!

These numbers do not form part of the audit reviewed or audited accounts and given as an aid to understand the business segment better. So there is really no accountability to those who spew it!.

There may be many reasons why previous year numbers change when presented in the current year, as compared to the previous years. Some of them could be (a) Fx translation done on fx revenue at different rates (b) reclassification of some line items to make a like-to-like comparison that results in changes or (c) some changes in Gross to Net when arriving at Revenue. There could be more legitimate reasons. In every case management provides clear reasons for the same - no CFO would like to have two different numbers for the same line item. Confuses the hell even within management!

There may be another reason why these changes are made - and I am sure you have guessed it.

You see, the “EBIDTA” for FY 21 for CLG as presented in FY 21 was 23%.

The same EBIDTA for FY 21 for CLG as presented in FY 22 was 21%

Now if I think investors will value me on improvement in “EBIDTA” then you can now say that you delivered a 500 bps improvement with the now FY 21 figures, whereas it would have been only 300 bps if FY 21 figures were kept as FY 21. Can’t say this couldn’t have been a motive.

But as such these numbers do not change and there is always a basic level of integrity to data. People are smart to know that otherwise Feynman’s first principle ‘that you must not fool yourself and you are the easiest person to fool’ will apply!!

Disc: No investments

3 Likes

In Q3FY22 board meeting they had decided to reclassify the schools business from discontinued operations to continuing operations (mentioned in recent con call as well as in both results PDFs)

So they have merged the schools revenue with CLG since CLG is housed in NLSL now due to demerger.

Upto Q3FY22 the factsheet was consistent with previous factsheets but only in Q4 it has changed as the effect date of reclassification was from 28th January 2022 onwards.

A note in Q4 factsheet should’ve been there to clear the confusion.

4 Likes

Hi Sahil, not sure if this will be much helpful as this calculation mere speculation from my side but let me try to explain my assumptions and thought process.

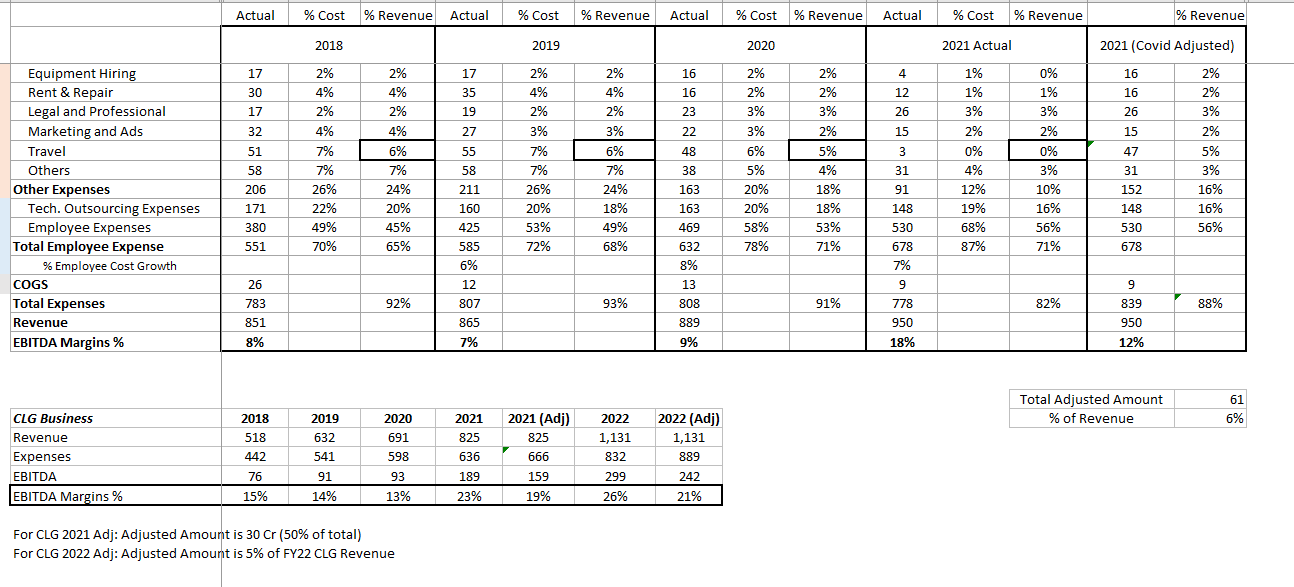

This is the breakdown of expenses sourced from the annual reports till 2021 along side calculation of breakdown in terms of % cost and % of revenue. Travel cost was constant ~5-6% which reduced to 3cr in 2021. I have created the last column where I’ve tried to adjust the temporary costs which includes 5% - travel cost and ~1.2% of other costs. Total Adjusted Amount comes out to be 61 Cr which is 6% of 2021 Revenue, which will bring the total EBITDA Margin for 2021 to 12%.

Since we don’t have Expenses breakup for CLG business specifically, I take an assumption to consider half split of Adjusted expenses between both segments. Below table shows the data for CLG Business where 2021 Adj considers half of adjusted amount (i.e. 50% of 60 Cr = 30) which will bring the Margins to 19%. Since we don’t have breakup of 2022 yet and some of the costs should be already back, conservatively I deduct 5% of revenues from the expenses in 2022 Adj which will provide us the EBITDA margins of 21 %.

Hence, I believe, it should remain >20% as per guidance. But as I said, there are assumptions in this calculation, and things could be different.

Also, as @dakshjain187 mentioned, now that School business is also included here in CLG for last 2 quarters, there could be more scope for adj. in this calculation.

5 Likes

Adding some insights that I think haven’t been covered in this thread yet:

This was a very important data point for me. Despite the large switching costs in changing training vendors, if corporates are moving to NIIT, it shows their capabilities.

“The highest level of expertise, the highest level of experience and the strongest sense of attention to our customers where they won’t get any of that or anywhere close to that from any of our competitors, and that’s the reason why so many customers have actually moved their contracts from incumbent providers to NIIT. Facebook or Meta had a long-standing relationship with Accenture and they moved their contract despite knowing that transition is very hard. Airbus had a 10 year long relationship with Conduit and they chose to move their contract to NIIT.”

and

“We have won more (deals/clients) than all of our competitors put together.”

-Mr Sailesh Lalla (https://www.youtube.com/watch?v=5UBuQnFqYIg)

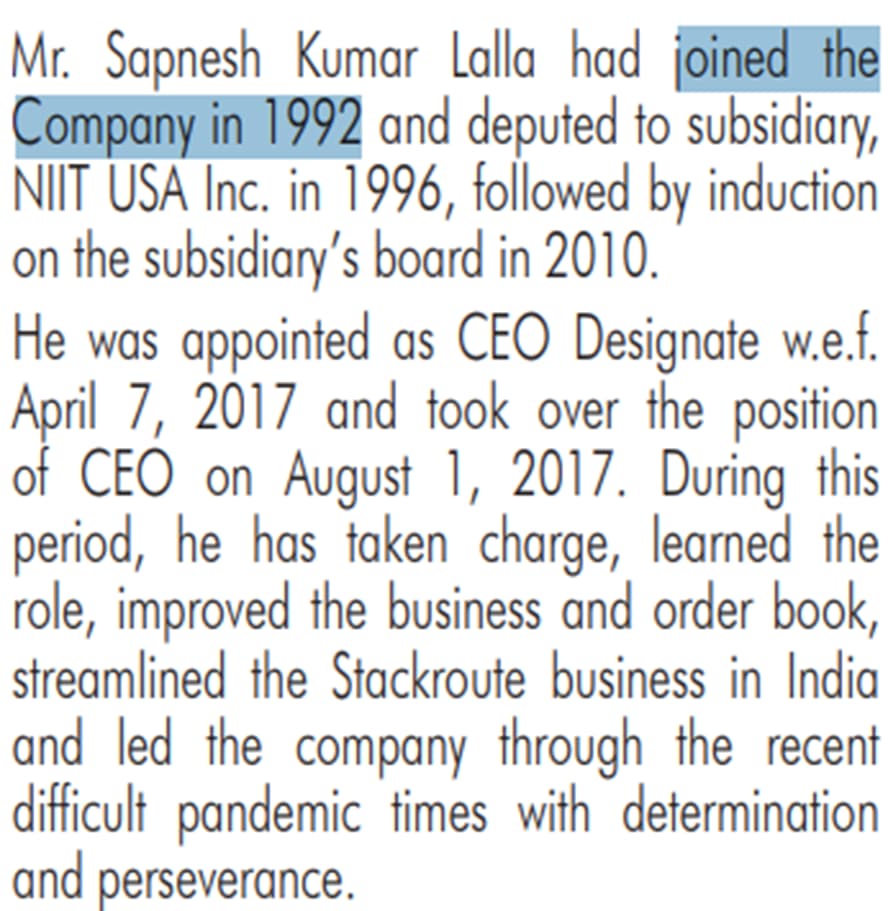

Sapneshji had been in the company for a long time before becoming CEO. Shows strong succession planning

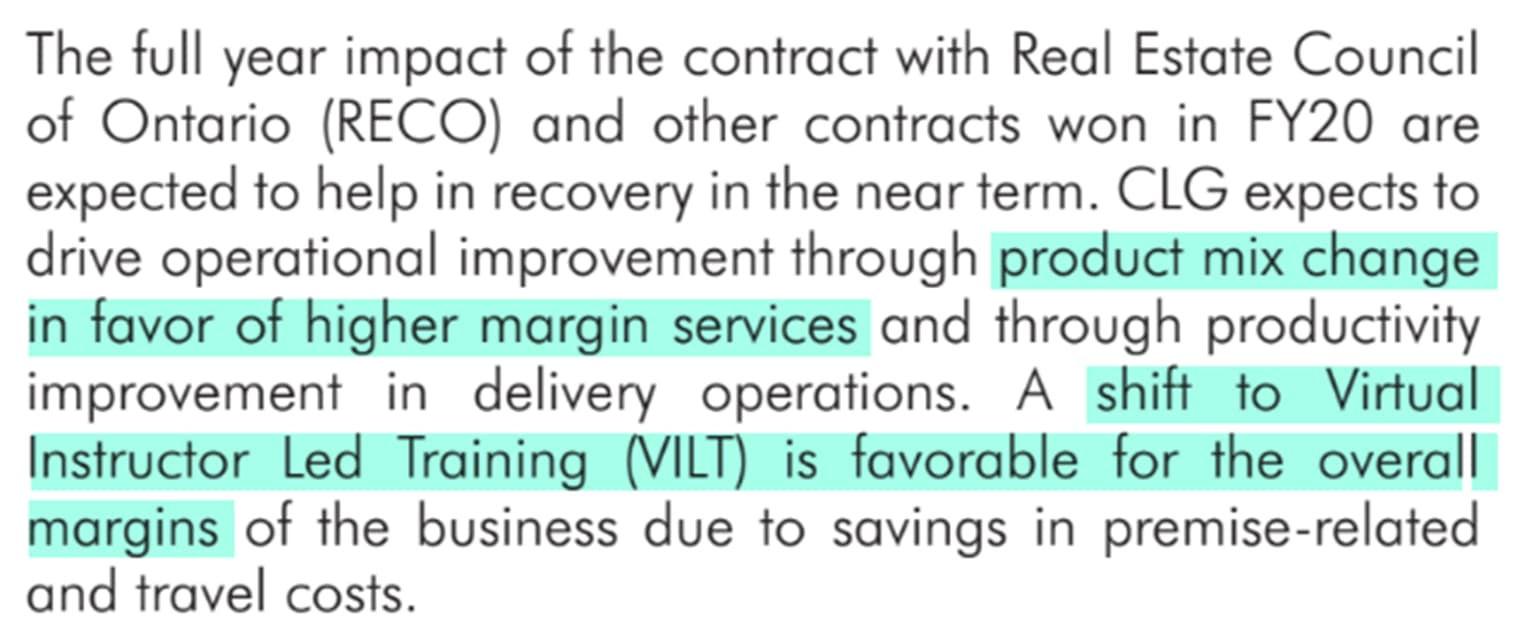

Product mix change

Margin Impact Visible Post Exiting B2G

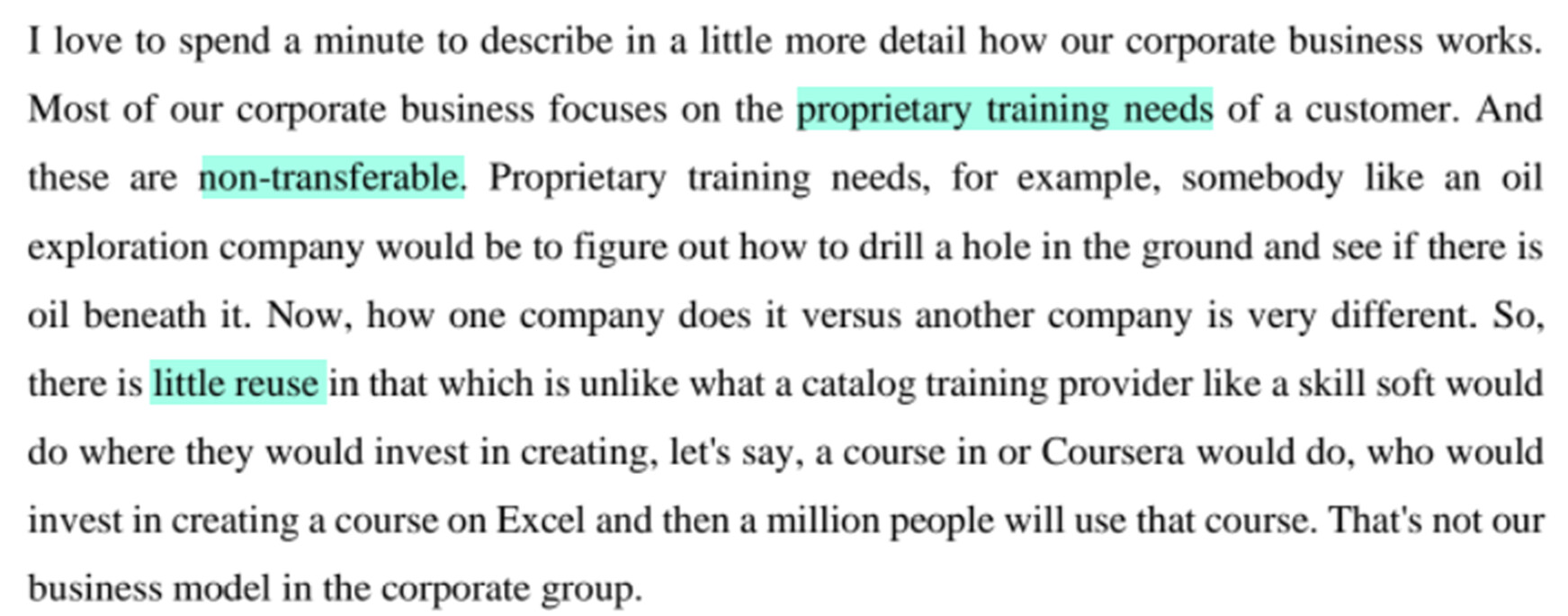

Due to highly customised training, there is little reusability

Was running some numbers and found this:

| FY | 17 | 18 | 19 | 20 | 21 | 22 |

|---|---|---|---|---|---|---|

| CLG Revenue (Rs Mn) | 4,534 | 5,183 | 6,324 | 6,913 | 8254 | 11,310 |

| CLG Customers | 34 | 39 | 46 | 54 | 58 | 66 |

| R/C (Rs Mn) | 133.35 | 132.90 | 137.48 | 128.02 | 142.31 | 171.36 |

Revenue per customer has started rising from FY21 and 22. I could think of two reasons- 1) expansion of contracts with existing customers (increasing wallet share)

and/or 2) larger deal sizes incrementally

Disc- added a tracking position

5 Likes

I was looking through the Q4 results and got curious if they lost customers in CLG business. Their FY21 customers tally was 58 while FY22 tally is 66 (net addition of 8) while as per Investor ppt they added 16 customers during the year.

1 Like

Last week a friend asked me to look into NIIT. His thesis was that NIIT is slated to grow at 20% for a long time and apparently outsourcing corporate L&D is a megatrend.

Somehow even after going through last 4 years of earnings transcripts I wasnt entirely convinced. I tried getting more data but in the absence of comparable peers I had to settle for inputs from 2 folks who have been involved in corporate L& D for a very long time. Aim was to corroborate what management has said and this is what i learnt -

Yes 20-25% of fortune 1000 companies outsource their L&D but this is not a small number. Most corporates want to outsource more but it’s not that simple. Unless you are a part of the organisation its very difficult to understand specific training needs. the exercise of outsourcing can then turn out to be time consuming and ineffective

NIIT may continue to gain market share as L&D is not core to the likes of Accenture, IBM etc but this does not say anything about their quality of service.

Neither had a very positive opinion about NIIT or the quality of their instructors but then again views can be biased due to past experience. For all you know NIIT this might be a new and better NIIT that they are unaware of. Please do your own diligence. I simply shared what I heard and understood.

7 Likes

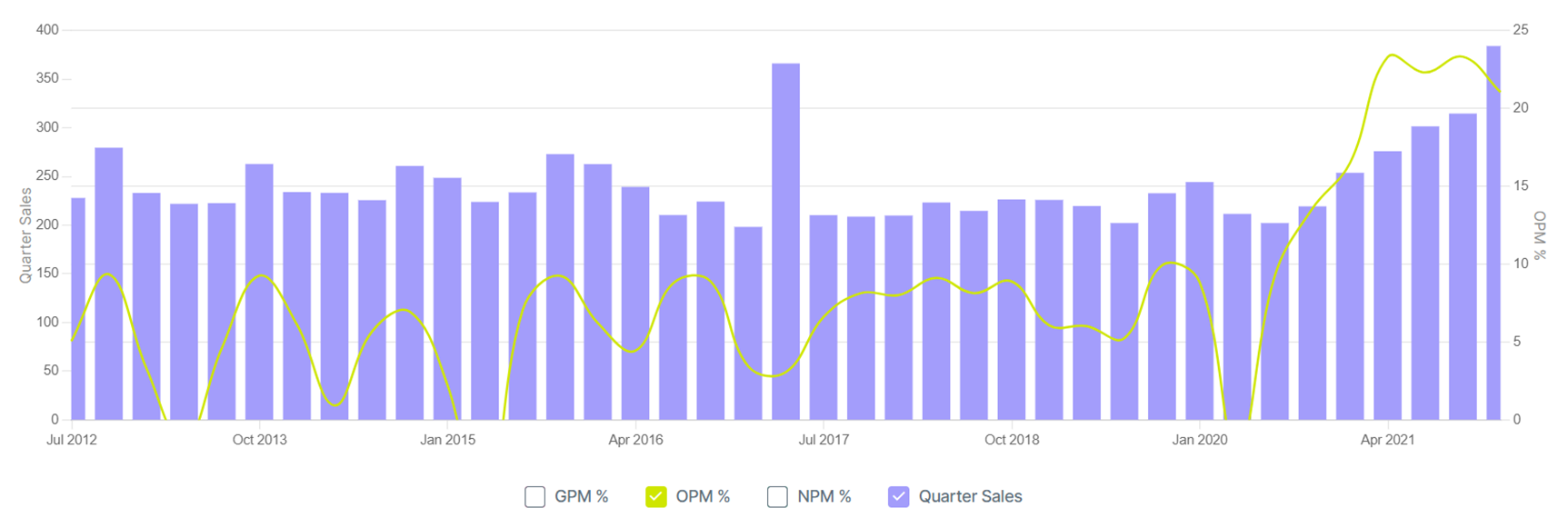

One more thing. This is from a concall in fy22

And this is from Fy19 I think

After interacting with a few people in HR it seems clear that L&D is a discretionary item and even after a recession or slowdown it takes its own sweet time to come back.

I have never worked in an office so I wouldn’t know. If you have an opposing view worth sharing please do.

6 Likes