A brief of the business overview, significant recent developments, key financials, and NIIT’s future outlook. Just want to summarise what has the company has done over the last year for anyone who is trying to gain a fresh perspective on the company.

1. Company overview

NIIT has two verticals, the first is the Corporate Learning Group (CLG), and the second the Skills & Careers business (SNC).

1.1. Corporate Learning Group

SNC provides managed training services (MTS), which includes Learning and Development (L&D) and talent outsourcing services to some of the biggest companies in North America, Europe, Asia, and Australia.

A case for MTS

In the dynamically changing, technologically driven, and digital business world, it is necessary for companies to keep training and upskilling their workforce to prevent obsolescence. All this training needs to be created, maintained, updated frequently for developments, and delivered to employees in an educational and interactive format. Mostly, companies employ dedicated L&D staff to do this, which is often underutilized, as their relevance is only for times when such a change occurs. While training demand fluctuates, the cost is largely fixed. Training is not their core activity, and therefore their efficiency and effectiveness are not consistent. A major benefit to outsourcing employee training and upskilling is thus, that it enables professional companies, such as NIIT, to undertake such ancillary activities, without having to employ a full-time training staff on a fixed income.

NIIT is currently the largest Indian player in the field, and in the top-5 companies globally providing MTS. CLG contributed 82% to NIIT’s consolidate annual revenue for FY 21-22, the revenue has grown 35% YoY to Rs. 11,310 million, with an EDIBTA growth of 68% YoY to Rs. 2,989 million. This exponential growth has been driven by customer addition, and an increase in wallet share from existing customers. During the last FY the CLG business has accelerated customer acquisition with an addition of 16 new customers for MTS, secured 4 renewals and expanded 6 contracts with existing customers. The company in total now has 66 MTS customers, and a revenue visibility of Rs. 26,240 million.

Globally corporate spending on MTS is over USD 370 million, of which less than 5% are outsourced. The economic slowdown since the start of COVID-19 and continuing due to the war in Ukraine and resultant inflation, rate hikes, supply side bottlenecks etc. has led to a contraction in L&D spending. Thus, resulting in such companies shifting from the fixed income, in-house L&D teams, to outsourcing such non-core functions. NIIT has already benefited from this in FY 21-22 and is likely to continue benefitting through the economic slowdown.

1.2. Skills & Careers (SNC)

SNC as a business has truly transformed since the onset of COVID-19. This business has shifted from a capital intensive traditional learning delivery model of physical learning centers to a digital learning model. Now the SNC business may be viewed as an Edtech start-up.

The business provides professional courses for young adults and corporate customers in India and other select emerging economies, preparing them for careers in different industries. For working professionals, it provides programs to those who wish to upgrade their skills for career advancement. SNC has a range of offerings for digital skills, including programs for 5G, Cloud Technologies, Cyber Security, Game Development, Data Science, and Full Stack Product Engineering, as well as programs in Digital Marketing, Business Development, and Virtual Relationship Management for the Digital Enterprise.

Further, the SNC business also consists of two other initiatives:

- StackRoute - A deep skilling initiative by the SNC business that helps companies transform their existing talent, by providing programs in AI, ML, Data Science, Cloud Computing, Digital Marketing etc.

- Talent Pipeline as a Service (TPaaS) - An SNC initiative that provides job ready employees, with an integrated offering of sourcing, training and onboarding.

SNC reported a net revenue of Rs. 2,465 million, up 99% YoY, with an EBIDTA of Rs. 10 million for FY 21-22. The low EBIDTA is owed to the fact that the company has only recently shifted to its digital platform and is still expanding its offerings, thus ramped up its investments in digital learning through the year. Despite this the company was able to generate a positive EBIDTA. Once the digital transformation is complete, while taking into account the low operation expenses of running a fully digital platform, the EBIDTA for the SNC business is likely to be significantly higher.

1.3. Recent Developments

(i) Share Buyback: NIIT bought back 6.97% of the total outstanding shares at a price of Rs. 240 per share.

(ii) Divestment: NIIT divested from NIIT Technologies for a sum of Rs. 20,204 million.

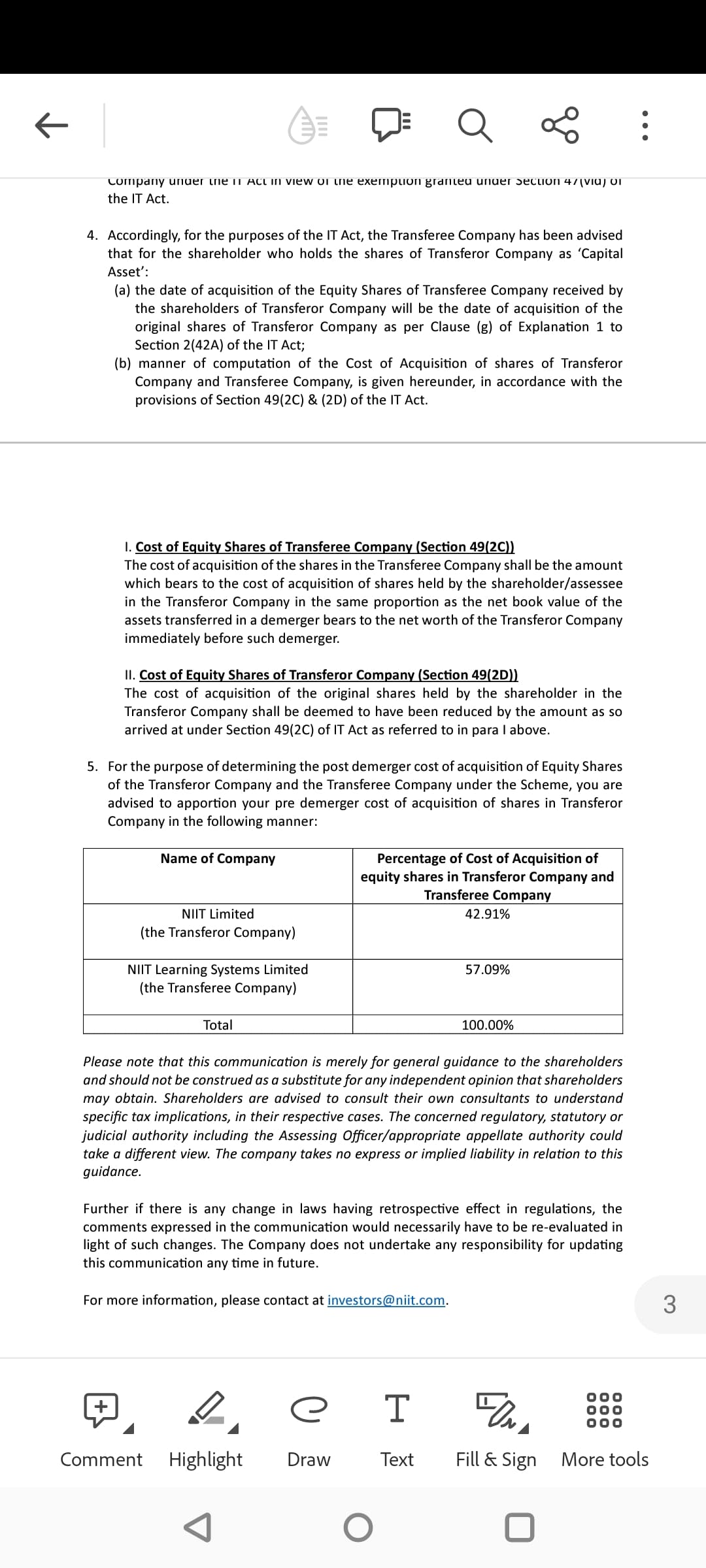

(iii) Composite Scheme of Arrangement: NIIT announced the reorganisation of the CLG and SNC businesses into separate publicly listed companies. The entirety of the CLG business will be transferred and vested into NIIT’s wholly owned subsidiary – NIIT Learning Systems Limited (NLSL) and every shareholder of NIIT will receive one share of NLSL for each share of NIIT held. NLSL shares would also be listed on BSE/NSE. The reasoning provided by the NIIT management for this is to (i) help the management teams provide undivided support to their respective customers, (ii) simplify decision making and capital allocation, and (iii) enhance the speed and agility in decision making to deal with competition and take actions in the best interest of the shareholders.

(iv) Acquisition of RPS Consulting: NIIT acquired 70% of RPS Consulting for a consideration of Rs. 827 million. RPS Consulting is a leading provider of training programs on emerging digital technologies for experienced tech professionals. The acquisition will allow NIIT to include technology training as a part of its MTS offering, for its global customers.

2. The Opportunity

2.1. Cash Reserves

The CLG business is a cash-cow. Despite the SNC business not generating any money yet, the company has cash reserves of Rs. 14,885 million, which is a decrease from the company’s cash reserves in FY 20-21 of Rs. 16,120 million. The reduction is due to a share buyback of Rs. 2,937 million and dividends amounting to Rs. 734 million. Net Cash from Operations for FY 21-22 was Rs. 2,898 million as opposed to Rs. 2,261 million for FY 20-21. The improvement is due to an increase in operating margins as well as increased efficiency in working capital. NIIT is able to generate 21% of its revenue as cash flow from operating activities.

The market cap of NIIT is approx. Rs. 50,000 million – thus its cash reserves of Rs. 14,885 million is approx. 30% of its entire market cap!

NIIT’s management has repeatedly stated in its FY 21-22 Annual Report as well as its Q3 and Q4 concalls that it is continuing to explore inorganic opportunities to add new capabilities and enter into desired markets and customer segments. In a time of liquidity crunch, where ed-tech start-ups are struggling to find investment to continue their growth journey, NIIT, due to its strong balance sheet and cash reserves, will be able to go shopping for companies that would grow its offering and enhance its value. The acquisition of RPS consulting is reflective of the managements capabilities in making such inorganic investments in a strategic manner. The cash reserves will also be utilised to fuel organic growth by reinvestments into expanding both the businesses.

2.2. Return on Invested Capital

I think a mistake is made by those trying to fundamentally analyse NIIT, by looking at the returns it is able to generate on invested capital. The ROCE of NIIT is 16.5% - which is nothing extraordinary. However, it should be noted that ROCE is the percentage of EBIT that is generated by the capital employed. Capital employed in nothing but the difference between total assets and current liabilities. Total assets include cash reserves. Therefore, despite a high EBIT, it seems that NIIT has a low ROCE, due to its high cash reserves (amounting to 30% of its total market cap).

Thus, a better way to analyse NIIT would be to deduct the cash reserves from its ROCE calculation – giving the Operating ROCE. Doing the same, the Operating ROCE for NIIT is 81.13% for FY 21-22!

As NIIT continues to add to its inorganic expansion, its cash reserves will decrease while EBIT is likely to increase – this would significantly increase the ROCE of the company in the future.

3. Conclusion

NIIT stock as of 20.07.2022 is trading at Rs. 370.75 per share at a market cap of Rs. 49,700 million. At a P/E of 22.18 and P/B of 3.35.

The stock has corrected from a high of Rs. 658 per share due to worries over recession in the West and a resultant fear over a reduction in discretionary expenditure by companies. On 18.07.2022, the stock corrected by over 7% after Apple released its report – highlighting worries over recession in America. However, as discussed in Section 1.1 above, a cut in discretionary spending is likely to result in companies moving to outsource more of their L&D, which is beneficial to NIIT.

Additionally, for a technology driven company with a high EBIDTA %, solid cash reserves and free cash flow, marginal debt, sales growing at 44% annually, profits growing at 39% annually for the last 5 years, Operating ROCE of 81.13%, and a likely significant expansion over the next few years with inorganic and organic investments – a P/E of 22 and a P/B of 3.3 is extremely reasonable.

Additionally, the scheme of arrangement leading to the creation of two publicly traded entities is likely to lead to value unlocking of both the CLG and SNC businesses. The CLG business will be seen as a highly profitable, cash generating and rapidly expanding business with a long runway for future growth. Whereas the SNC business will be one of the only listed Edtech companies, with hyper-growth and profitability.

For the above mentioned reasons, I believe that the NIIT as a company will have significant future growth, with a long runway, and is currently available at a good price, and can thus provide decent returns to its shareholders.