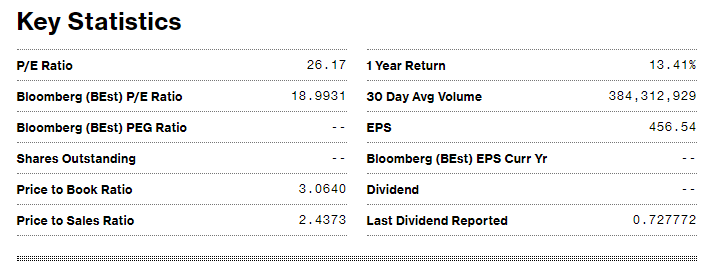

Bloomberg data untrustworthy, since above pic shows 27.44 pe vs 18.5143 est pe (fwd), with Nifty at 11748 which mathematically requires 1 yr fwd EPS to rise to 634.5 ie ~50% increase when EPS seems declining.

Their est PE 18.5143 goes to 4 decimal places; such a joke, though maybe they deserve a clap for humour

Method of calculations has been changed post June 2009

Post June 2009 PE NSE Started Calculations based on Free Float Market Cap instead of Full Market Cap prior to this.

Free Float is available at NSE website.

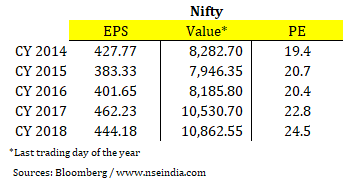

I’m providing you forward data of Nifty Stocks

Hope that may help you NIFTY 50 SHAREHOLDING PATTERN.pdf (90.1 KB)

My take on various factors that can distort the true market valuation/PE multiples

factor1:One 2009 Business standard article stating effect of free float methodology on index calculation by NSE

factor2:Add to that effect of RBI guideline for banks to reduce promoter holding of banks in phased manner thus increasing Free float of banks ,in below article The RBI licensing guidelines for new private sector banks 2013, calls for promoter holding to be brought down in phases, first to 40 per cent at the end of five years from the date of commencement of business operations.

Subsequently, it needs to be brought down to 20 per cent at the end of 10 years and 15 per cent at the end of 12 years. The 2016 guidelines calls for reduction in promoter shareholding to 15 per cent in 15 years.

FACTOR3:Add to above that banks can be valued at PE but P/B is better matrix

FACTOR4:Add to above that that NSE etc use standalone instead of consolidated earning to calculate PE , some detail in below articles

FACTOR5:Also the swing effect of earning from-ve to +ve for some companies like axis bank/ICICI/SBI as discussed in below link/tweet

FACTOR6:Also the argument about timing the market effectively

My Conclusion: Its better to focus on valuations of individual companies that we want to invest in than focus on all these mumbo jumbo

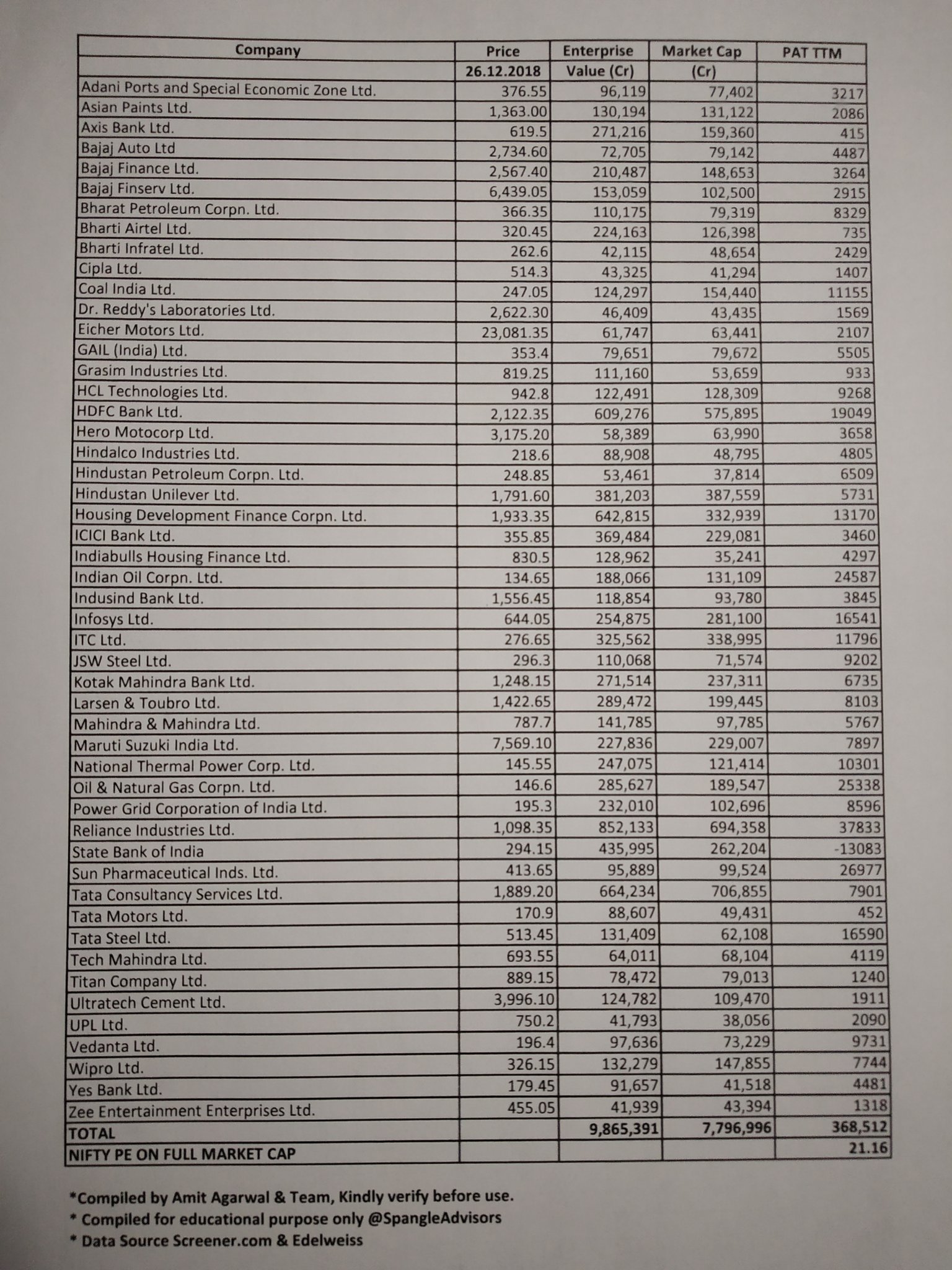

The TTM numbers, assuming them to be for Dec 2018, do not seem to match with declared results. Easy ones to pick are Tata Motors for instance, which declared a big loss resulting a TTM loss, but the figures you posted show a profit. Similarly for some of the others I saw.

I had attached an excel spreadsheet along with EPS computation showing figures for each Nifty constituent. Nifty PE Q3 FY19 for valuepickr_corrected.xlsx (27.8 KB). . You may compare with this sheet, which directly comes from SE filings.

I’m totally agree with you.

It’s a myth which has been created by some Analysts and Fund Managers.

Nobody care to tell us entire matrix of calculations is not comparable and it’s showing miscalculated pictures of real Market Valuations.

We should stick with the individual stocks.

Markets are far better valued now on

P/BV

Market Cap to GDP

Capacity Utilization

Debt level of Cos

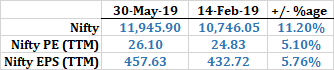

My computation shows TTM Nifty PE at 26.10 on May 30, 2019 vs 24.83 about 3.5 months ago on Feb 14, 2019. Nifty grew by 11.20% and its earnings per share by 5.76% during the same period.

The numbers from Bloomberg is close on NIfty EPS and look like this:

Thank you @diffsoft. This is very useful to understand relative heat. Do you have reference figures (computed by you or took for reference from another source for comparison) for nifty from 2007, prior to previous major bear market ? If yes, please share.