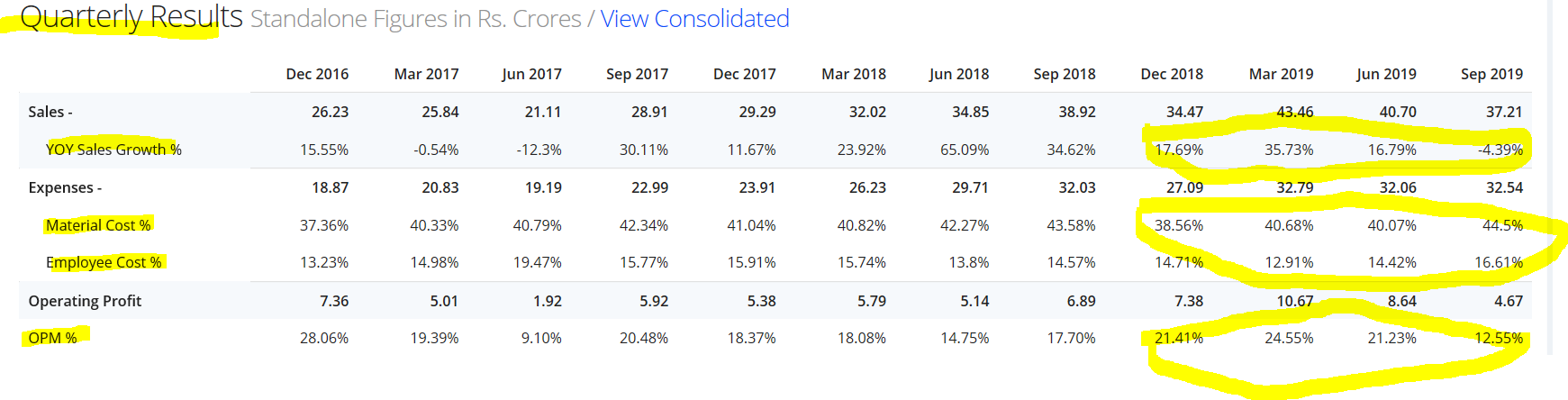

Numbers are bad.

After seeing Sequent and Lasa numbers, i was expecting a decent set from NGL , but cost of materials consumed as reported by NGL is higher than previous quarters. Needs to be digged more.

Sequent Scientific operating margins remained strong and even Lasa is expected to be profitable going forward.

Employee Benefit Expenses are also increasing.

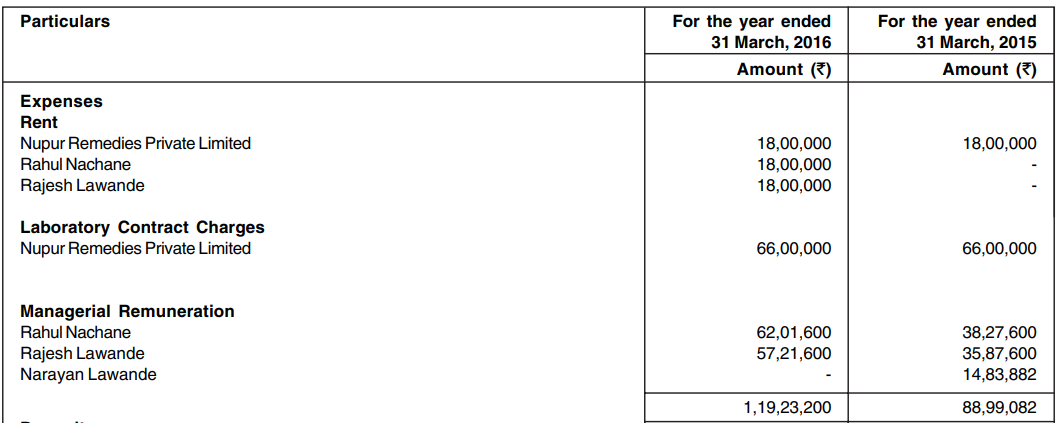

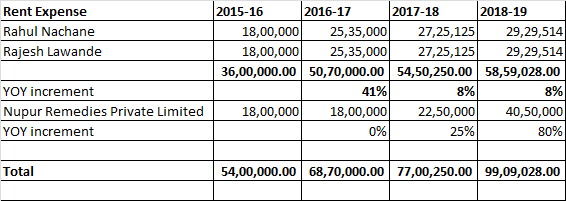

Rent Expense 2015-16 2016-17 2017-18 2018-19

Rent Expense 2015-16 2016-17 2017-18 2018-19