Sharing my notes from AGM:

In feb 2019 we started the new plant. In next 3-4 quarters we should be able to reach optimum utilisation.

Macro tech - we have acquired this co for backward integration - production of intermediates. The company had EC (which is very valuable these days) and 38 cubic metre capacity. We are refurbishing the plant as per our standards to start utilising the same. This investment should help us increase our margins.

Trial batches of 4 products going on. Plan to commercialise in coming quarters.

Zero liquid discharge at Tarapur. Will do one more plant in current year and then 1 more plant next year.

China should come back in a year. We are not manufacturing about 4 products of our 21–22 product basket as production stopped in China. As China comes back, we can manufacture them.

Last year we did about 35% growth - about 15% would be due to price increase rest volume. Till 2017 prices were going down then they started rising since 2017 and it took us sometime to increase the prices as customer resistance is always there.

We have weekly off on Friday at our plant. It is necessary as we are a pharma grade company and we take lot of caution on cleanliness etc. Consistency and quality won’t be possible otherwise. Last year due to demand we started working on Fridays too and paid overtime to workers. Since the new plant came online, we have started taking weekly off on old plant.

Our capacity was 150 cubic meter and with new plant it will be 250 cubic meter. Peak production can be 225-250 Cr.

Cost of operations at new plant is being charged to P&L.

It will take sometime to increase production at new plant as we have been working on new products since last couple of years and as of now validation/trial batches are going on. The new products are for Poultry industry. This is much bigger industry but the overall realisations are very low. We generally operate in APIs of about 4-5000 Rs per kilo while this market has molecules of 500 per kilo. We have been able to find some molecules which are high value and fit into our value range. But it will take some time. 40% would be old customers rest we will have to develop.

As EC is getting very difficult, this time we have already taken EC for our new Tarapur plant in pipeline. We have done the minimum required civil work. Will start working on that once we utilize 50% of new plant. Look to invest 40-50 Cr in this new Tarapur plant.

Overall 10-15% growth is normal and achievable. We don’t want to give any guidance as a policy.

Customer acquisition time is 3 months to 5 years. 3 months for a customer from a country like Bangladesh and 5 years for a customer from a country like Europe.

R&D team has grown from 4-5 people to 30 people in 10 years. 2.5% of sales as expense on R&D. May increase to 3%. It has helped to improve process, new product development.

We sell to European customers, who sell end product to un-regulated market.

We intent to remain focused on in-regulated market for next few years.

R&D - new product happens on 1. Customer request 2. Similar chemistry 3. Own research.

New plant takes 24-30 months to get commissioned.

Industry margins at EBIDTA levels are about 18-23%. Last year was a very good year and generally don’t sustain. We can do couple of % points more than industry.

We don’t have a 10 year plan, we don’t have a 5 year plan either. We work on 2-3 year view.

Human API - not significant. We had done some products but couldn’t get success as mindset is different.

This is a highly technical industry. Long vendor approval process. It starts with sharing samples. Then ask for more samples. Then stability study. If approved then we start selling. It takes 3-5 years to scale up a product.

We are very conservative company - its easy to spend money but difficult to manage and generate returns.

Bad debts are hardly 60 lac since start.

Receiving money more imp than selling.

We did 4 new products in last 2 years but couldn’t scale up. Macro tech acquisition should help us in improving the intermediate problem.

Top 3 products would contribute about 45% of turnover. Largest product would be about 18% of turnover.

Market potential - why aren’t there large cos in vet industry from India - the market is not as big as it is thought to be - large part is human side. And some part is very low value or too competitive. We are in a niche where few molecules are of high value and we go to 7 to 10 steps (reactions) to product them. So such kind of area is not very large. In some of the molecules we have good market share. There is good competition too - usually 5-6 players are there for each molecule.

On questions of increase in salary - its an enabling resolution. The salary will be capped at about 7-8% of PBT. We don’t intend to overshoot.

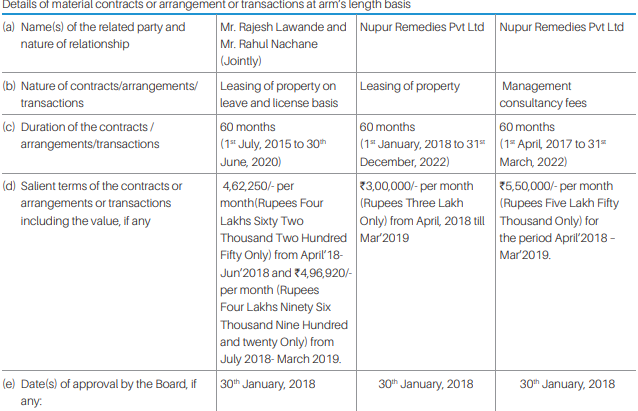

On questions of substantial increase in rent to related party - the R&D is carried out on premises owned by group company. It’s a 5000 sq ft property at jogeshwari. We also took a office 2500 sq ft at Ville Parle for corporate need. If you calculate the market value, the rent is very reasonable and at less than market rate. If the co had to invest in these properties lot of investment would be required.