So when we are talking of changing strategy, we are talking about pivoting from the smaller

bank sizes to a larger addressable bank, which are banks above $20 billion or $50 billion up to

$200 billion, which is typically around 100 accounts.

Opening Remark:

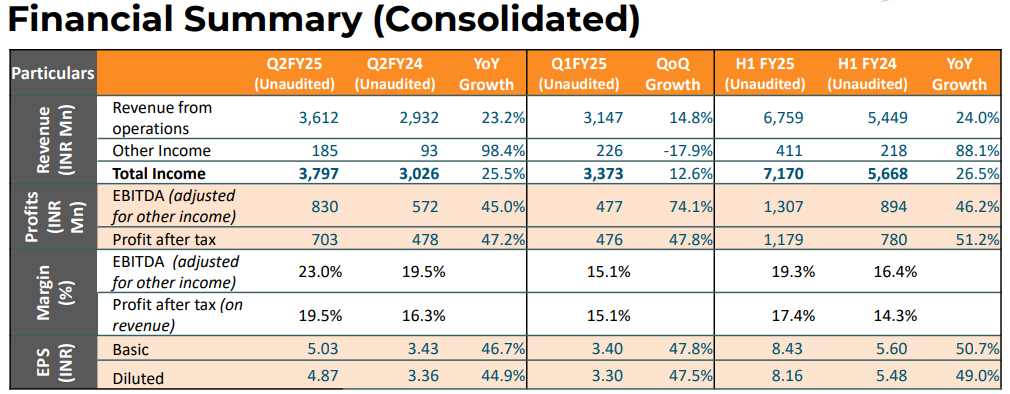

Q1 Revenue 25% growth. PAT at 48 cr. growth of 58% YoY. Margin at 15%.

Marketing and sales investment continue and increased.

Q1 is weakest quarter, though seasonality is reduced.

Q1 Annuity revenue is 201 cr.

More than 10 cr order from Indonesian state bank, Malaysian government bank, US Retail bank , Qatar bank. Large Indian company selected Newgen for loan originating system.

New Product:

Generative AI hyper personalization platform specifically for banking sector, will improve profitability and customer experience world wide. It help banks to have upscale and cross sell opportunity. Very few products like it and excitement in market.

It is essential to launch new products to have growth.

It take 3 to 4 years to give numbers for new products. Marvin is Gen AI Horizontal product. LumYn is target for hyper personalization.

Guidance:

PAT Margin guidance at 20% to have not much churn. productivity increase.

Deal size increasing by 20 to 25%. Hope to trend continue.

Annuity and implementation split will be same.

Continue with margin and spend on marketing and sales.

General comments:

Partnership revenue is 20% and direct at 80%. Same level.

Generally get 10-15 deals/Quarter, Q1 get 13 deals.

Leadership in traditional market, aspiration to have it in US and Europe. US have early signs of revival but still do not have big momentum. Expenses are write off and not capitalized.

Generally 15 to 20% revenue from new logos.

Q1 hired 500 campus people from Jan 2024. Cash at 850 cr.

Q1 20%, Q2 20%, Q3 30%, Q4 30% revenue bring in broad.

ESOP will not have incremental effect on P&L it is similar, what done in last 3 years.

Revenue growth: Newgen reported strong revenue growth of 25% Y-o-Y for Q1 FY 25. This growth was driven by good business growth across all regions, with EMEA, India, and APAC showing growth.

Seasonality: Historically, Newgen’s business has been seasonal, with Q1 being the leanest quarter. However, the impact of seasonality is slowly reducing.

New client additions: Newgen added 13 new logos in Q1, indicating strong customer acquisition.

Upselling and cross-selling: Upselling and cross-selling to existing customers are significant contributors to revenue growth.

Product innovation: Newgen launched a new product, Newgen LumYn, an AI-powered hyper-personalization platform designed for the banking sector.

Profitability: Newgen delivered healthy growth in profits and expanded margins. Profit after tax was at INR48 crores for the quarter, witnessing a growth of 58% Y-o-Y.

Global expansion: Newgen is focusing on increasing its global reach, especially in mature markets like the US and Europe. They partnered with Finastra to offer better banking solutions and expand their market base.

Investments: Newgen is continuing to invest in R&D and sales and marketing initiatives to support future growth.

Employee growth: Newgen has been hiring aggressively to support its growth plans. They hired around 500 campus recruits in Q1 and are also doing some lateral hiring.

Product Offerings: Newgen is focusing on expanding its horizontal product offerings (NewgenONE, LumYn, Marvin) which cater to broader functionalities. They are also expanding their vertical offerings to include areas like Trade Finance, Supply Chain Finance, and Insurance.

Sales Strategy: The GTM strategy is primarily verticalized, with sales teams focused on named accounts in Banking, Insurance, Financial Services, and Government. Horizontal product sales are driven through partnerships and inbound leads.

Impact of New Products: The newly launched LumYn and Marvin are expected to contribute to the top line and bottom line in the long term (3-4 years) as the sales funnel matures. They are not expected to have a significant impact in the near future.

In addition, the company clarified that ESOPs are granted to a broad base of employees and the financial impact is not expected to be significant.

Overall, the transcript paints a positive picture of Newgen’s financial performance and future prospects. The company is experiencing strong revenue growth, expanding its margins, and investing in new products and global expansion.

Follow me on X for many other company updates: x.com

Interesting. $500M equals around INR 4000 Cr. With guidance of 23-24% EBITDA and 20% PAT (Q1FY25), PAT could be around 800 Cr. If PE normalizes to 30-35x (for a very fast growing asset light company), valuation could possibly be around 24000-28000 Cr in FY27. And if (less likely) current valuations hold, this be 48000 Cr!! Still ~2-3x from current levels!

Newgen 's USA journey just started now. That’s THE Market. With rate cuts coming, and all IT companies, r telling that BFSI CIOs in USA r loosening the purse…things will be become better for them.

Till now, whatever results came, came mainly from India, APAC and Middle East…long runaway ahead…

Yes that is correct. Their non-reliance on EU-USA geography is what kept them going good during the recessionary times (2021-present?). The likes of InfoBeans are struggling even today.

This is my first contribution to ValuePickr and I hope you will like it

Also, just to continue with the above discussion, I feel this is just the start for Newgen. US market opening up after yesterday’s rate cut will surely bring in more business plus it is just a midcap stock with exposure to AI and other fast-growing tech solutions. Much better bet for growth investors than Infy/Tcs!

As someone who has collaborated with them in the past, I’ll demystify some of the hype around their business.

They make document management platform where you basically manage documents in digital format. It’s a highly competitive space and which reflects in Newgen’s modest margins for a product business.

As for their patents, one shouldn’t read too much into them. I have been working in the technology sector for last twenty years and can tell you that majority of the patents tend to be flimsy and used for marketing purposes.

On a big picture level, their business will do well as world is going paperless and advantage with small IT companies is the small base. So even if they don’t gain any market share, increasing segment pie will ensure the steady growth in their topline. But one should keep an eye on valuations. For 25% margins, and a commoditized product business, 70+ P/E is a bit stretched.

Disc- Identified this stock as a value buy when it was 300 in 2022 and invested.

Unlike software service companies, product companies have the advantage of operating leverage to play out. In my view Newgen has the probability to play out operating leverage if they get pie of share from US market and Trade Finance product is a bonus if it clicks out.

Going by their history, They’ve usually reported +30% in H2 comparing H1.Going by this i think newgen has good quarters ahead and should do better than last year.

I’m in the software business so understand your point. It may not always be true but generally it’s usually the case with companies with unique advantage (e.g. network effect, monopoly etc). With NewGen there is no clear trend in their margin trajectory and their OMs have been ups and downs.

There are other factors one need to look into to assess how much operating leverage a software company can unlock with growing sales than making a broad-brush determination.

For example, what’s software revenue component in a typical deal size and how much is services? Higher portion of the first is good while more of the latter is bad.

Second, how does software licensing model influence marginal cost of addressing additional scope and scale for a given customer?

Finally, how much of the company’s business comes through repeat, single source or tenders? In the latter, margins again tend to be lower.

As I mentioned, having seen their offering up close, I don’t think NewGen really has any moat. There are plenty of document management system providers in the market who offer similar software. And that’s reflected in their uneven and lower margins (20-24%) for a very long time although revenue growth has been in decent double digit.

But that doesn’t make things bad for NewGen per se. If I were to choose between a great company in a bad sector and a not so great company in a great sector, I’d always invest in the latter because I get the advantage of rising tide.

Newgen in my view falls in the second category. It has got tide under it with growing digitalization in the world. So I expect stock to do well in the near future and that’s reason I continue to hold it while being aware of its strengths and limitations.

Hemant, Newgen isn’t just focused on document management systems; it also offers a low-code platform that allows both clients and Newgen itself to rapidly build products for various verticals, such as loan management, supply chain finance, customer onboarding, and more.

If you’ve been following Newgen for some time, you might recall that after COVID, a regulatory change in the U.S. created a demand for specific software. In just a month, Newgen developed a solution using its low-code platform to meet this requirement, making an entry into several smaller U.S. banks. In the U.S., Newgen’s competition includes Pega Systems, Appian for low code platform. Cracking the U.S. market would be a major win for Newgen, as it would be the only Indian product company competing directly with likes of Pega in this space.

Just a couple of days ago, Newgen announced on the NSE that it has been featured in the Gartner Magic Quadrant 2024 for low-code platforms. I haven’t been able to find the 2024 Gartner document yet to determine quadrant. In 2023, only two Indian companies were in Gartner quadrants for low code.

One of the things I really admire about Newgen is its employee retention. I have a couple of friends who have been working there for over 10 years, which speaks volumes about their employee retention policy.

And yes, valuation is definitely high, which is for everything in this market, but I am hoping it to crack US market, and if it does, I hope that it shows real product business operating leverage kick in.

Disclosure - Invested. Biased. Holding from Rs 250 level.

Low code platform merely means that a customer can expand the software functionalities or build new applications using user friendly libraries (for example using drag and drop features to build a new process). That itself is not unique and most of the product companies call their platform as low code (like many have started calling them AI-enabled).

The main solution they offer is content management where you can digitize, review, govern and manage your content through its lifeycle. Most of the content in the organizations tend to be in unstructured format (pdf, word, ppt, jpeg, email etc) which accounts for roughly 90% of the total digital content that an organization creates. So that’s a big opportunity itself. Which is why I’m saying that they are currently in a good space. But that doesn’t mean their offering is differentiated or moated.

It’s a highly competitive space and range bound operating margins reflect that and you don’t see any operating leverage playing out in last 6-8 years although revenues have been steadily increasing.

Pls don’t think I’m criticizing Newgen or undermining their solutions. I’m just saying that one should take buzzwords like GenAI, lowcode, open architecture etc with a pinch of salt. As long as there is demand growth from end consumers all players in this space will do well including Newgen.

Disc- Also invested in the stock but not biased.

Being in the Software Industry for 20+ years, I can comment on the nature of low code platforms. This is usually prefered by a novice who barely started his career. If you ask any software development expert they will not prefer the low code platform. Earlier MS Access based software were used to build quickly POC for vendors with little effort. Once the POC gets approved software companies used to go for full fledge development life cycle. With advancement in technology the low code platforms got siginificant feature addition which helps the begginers to develop some what enhanced softwares with little skills. Low code platform is highly competitive and easily replacable.

Earlier in this thread some one mentioned about the employee retention, need to check if they stick with the company due to lack of skills or stickiness of the business and performance hike they get compared with other industry

Choice of low code-no code is not made by the novice programmer or the experts as you indicated.

Mature organisations restrict even the list of programming languages to be used, let alone the Enterprise grade platforms like NewGen. Salesforce, ServiceNow, MS Power Apps, Adobe AEP and so on all provide low-code capabilities.

The mistake is to look low code as center of gravity of such platforms including NewGen. It’s a valuable enabler that complements the core capability, making it easier to configure and customise, but not the primary capability being sold.

These platforms can at the max compared with opinionated frameworks that come with a built-in philosophy. The philosophy helps organisations to reduce the decision fatigue. Ability to quickly code is a bonus.

Congratulation Pankaj … I am too invested in it since 200 level before bonus issue. Since I had given significant weightage, so it has rewarded significantly.

What is important about Newgen, When other IT companies were struggling around 2022, it was performing consistently. As long as it is performing, I will hold it.

Newgen didn’t perform in 2022 and it struggled more than other IT companies falling some 40% in a year. Stock turned around in 2023 along with other IT small caps stocks.

Performances in my write up means quarter results of Newgen. Check that in 2022. I invested after watching it’s result not the chart.

As long as it is giving good results, I am not worried.

Newgen was performing good in terms of sales and profit .also when other iT stocks were falling it gave good returns so pl explain what excatly you mean .i think busniess doing good every quarter growth is visible