In my short experience with the market.

Its actions are extreme at both the ends…i feel like participants are simply scared nowadays.

even after order announcement newgen continues to take beating !

From here on I am okay to add more if it goes down further or if it goes up.

D- Starting position ~1060

Well, a bit of fear is necessary in the market as they say bull markets are born out of deep pessimism and die on euphoria and this applies to stocks also.

So when you see strong consensus buy calls on a stock, expect correction and when everyone is afraid to touch a stock, load up on that (assuming all other things being equal).

Mean reversion is immutable reality of equity investing.

I’m invested in Newgen from very low levels so with the returns I have made I don’t’ mind this correction. But I’d still caution people not to rush into buying this as valuations are still expensive. If someone really fancies this, then they can take small positions and then add gradually. I don’t expect further significant corrections from these levels.

9 Likes

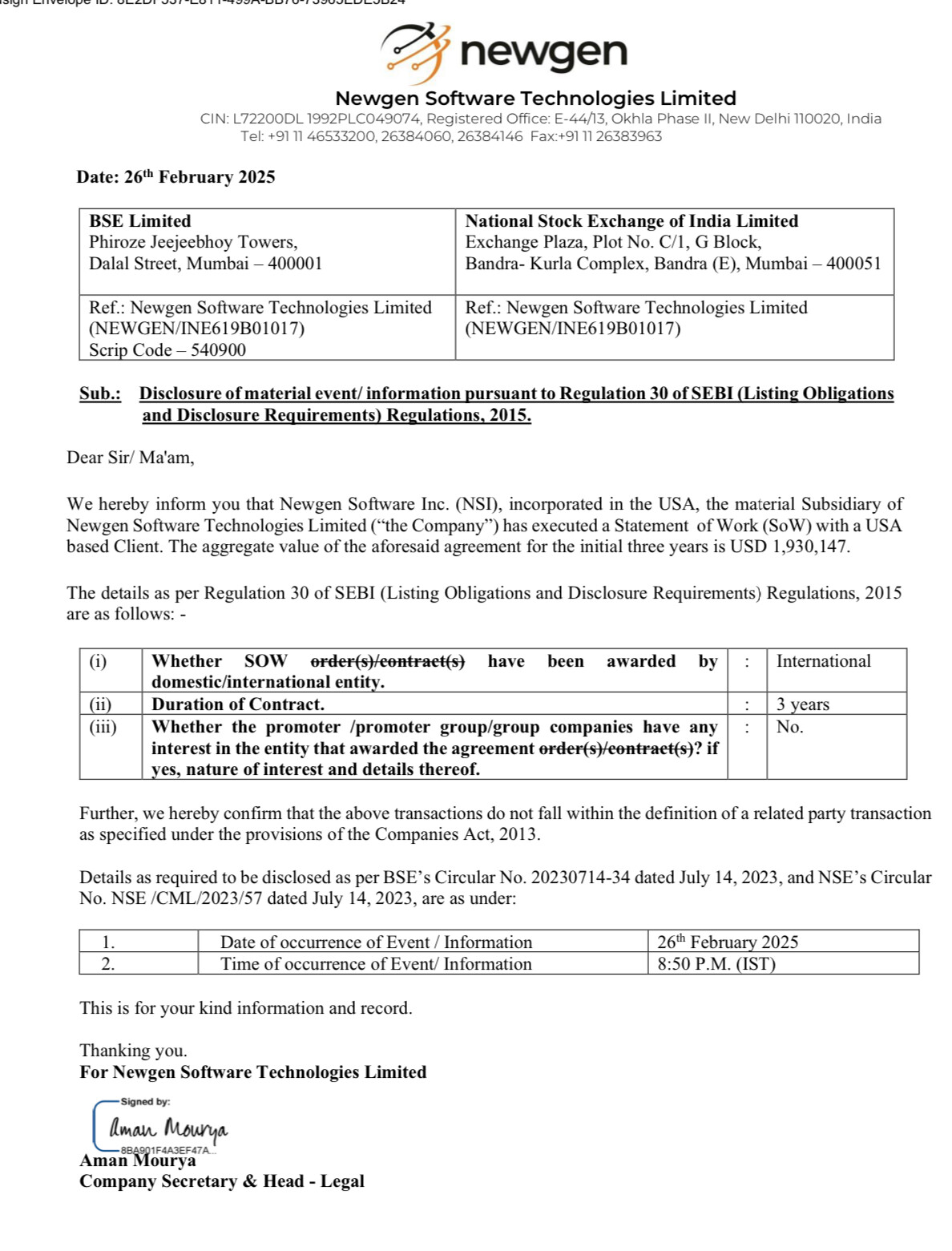

Newgen has executed a Statement of Work (SoW) with a USA

based Client. The aggregate value of the aforesaid agreement for the initial three years is USD 1,930,147.

Duration of Contract. 3 years

4 Likes

The aggregate value of the aforesaid Award is USD 1,285,074 inclusive taxes.

The time period by which the order (s)/contract(s) is to be executed : 5 Years

2 Likes

The result of IT companies like Wipro, Infy, Tata elxsi , E2E is not so good in this Q4 Fy25, Q4 FY25 result would be crucial for Newgen. The result will clear whether the slow execution of orders in last quarter is still there or it has accelerated!!

2 Likes

Q4 result is scheduled on May 02,2025 as per exchange disclose. After so many years, results is coming on Friday. Earlier, they used to declare on Tuesday.

2 Likes

Expectation on Q4 result:

Net revenue from operations: 450 cr

Profit before tax: 148 cr

4 Likes

Newgen Management on GenAI

Question : GenAI has been one of the big tech disruptors. Is there a case, where this could cannibalize Newgen’s revenues on the content management or the BPA end?

Answer: I think this is a question for service companies not for product companies. Technology is our enabler to sell. GenAI has actually reinvented all the use cases across industry for the kind of things which we sell. In fact, using AI for content ingestion is one of the most hot cases right now in the market, by which the last quarter out of around six deals we got in US 3-4 are just around the AI capabilities of our product which is typically a combination of ML and AI. We are leading this right now. I can say with confidence that we have the one of the most content management and low code AI led products in the market with our Marvin, Luimn and Hyper. Most of the cases we have won in last two quarters, AI has played a very important part of that. The content management and GenAI complement each other. So far people used to retrieve content, now they can discover more value out of that content. That’s why GenAI works on that content either through RAG or vector embedding or many other technologies like that. There’s a renewed interest in the enterprise content management space globally right now, both on the ingestion and the management & knowledge management side of that. We got 2 orders in Singapore government, which are to do with kind of things we are talking about. We got one of the largest orders from the primary regulator in India which is AI led content management and similarly we got 3-4 orders in US from insurance companies which are around document ingestion which is AI. So, this is what we are excited about not threatened about.

Disc: Invested. I am not SEBI registered Advisor/Analyst. My view may be positively biased. I am not suggesting any investment action. The information provided above is for education purpose only.

3 Likes

Pretty close

Profit before tax is 141cr

Any indication/inferrence Wht can they do FY26 & 27 ?

D- Not invested, Studying again

As per concall, they will resume their growth like Fy22-24 from Q3 of this financial year. They are taking some implementation time of some orders till then.

It is like they were getting 97-98 marks till Q2 FY25. Now, they got 91-92 marks. As per their commentry, they will again back to 97-98 marks by end this financial year.

Reason: 1. Increase in size per order which has increased implementation time which has affected their associated revenue growth. Still they have grown 20 percent in annual basis.

2. Tax bracket has increased which has affected PAT.

Disclosure: Invested at very low levels. Already multibagger for me. No plan to exit in immediate future. I would remain invested till it is growing around 20 percent or more annually.

9 Likes

Today: Q1FY26 result day. Q1 has been thin quarter historically. Their income is always lowest in this quarter among all four quarter of financial year. It is also very hard to predict their topline and bottom line in this quarter due to low base of this quarter. I will be waiting to see update on status of their execution on recent orders in management concall in evening. That will give idea about its future trajectory in this financial year.

10 Likes

Concall update:

The management concall gave a hints of increased degree of issues which we had seen after Q4 concall.

Although they’re still looking for growth, they don’t give guidance but this time they do not sounds like maintaining 20 percent growth on annual basis. I may be wrong but there was certainly difference in their confidence for timeline of recovery. Offcourse Newgen management has been always honest. Looking on its high PE, there is no scope of less than 20 percent of annual growth. PE derating can be saved only if Newgen attain 20 percent growth or more on annual basis. This quarter was too flat after in longway back sometime in 2021.

3 Likes

Yupp. Tend to agree. Also, on large deals, in Q2, they have not secured anything yet. I think this year will be sort of muted. There is also an upfront cost of sales, new product scaling etc.

2 Likes

overall weak Quarter, smaller deal size win, no order cancellation seen, headwinds observed by management, no specific number in guidance was mentioned as mentioned in previous quarter.

overall weak concall

2 Likes

Hi @Hemant_Kumar2 I tried to understand the usecase they are trying to solve but unable to find any documents related to it.Do you have any reference to the sources where they have specifically called out the usecases they have solved using the platforms they have.

New order inflow was muted in last couple of quarters for Newgen. Hence, the growth slowed down and stock corrected significantly.

However, Newgen has recently reported very robust flow of new orders across geographies. This should help in bounce back of revenue growth. This also indicates that slowdown was temporary and Newgen’s IT products have good potential.

Disc: Invested. I am not SEBI registered Advisor/Analyst. My view may be positively biased. I am not suggesting any investment action. The information provided above is for education purpose only.

7 Likes

Newgen Q2 2026 Conference Call Highlights:

Revenue, 400.8 cr. Growth of 11%, YoY.

Subscription revenue Growth of 20% YoY.

EBDITDA 102.4 Cr. Growth of 23.4% ( adjusted for other income)

Net Profit of 82 cr, Growth of 20.4% YoY.

Margin 25.5% compared to 23%, YoY.

15 New logos were added. Multiple large deals in Europe, Ghana, US and India.

Focusing on expanding in India and Middle East.

EMEA and PAC growth at 22%.

EMEA at 3% AND India at 7%.

R&D spend at 9% of revenue.

Sales and Marketing 21% of revenue.

Net cash at 90 cr for 6 months.

Large deal momentum:

Delay in large deals in India and EMEA, but strong wins in mature markets.

Q2 have significant wins in mature market, which are subscription based and don’t contribute immediately to revenue.

Overall, momentum is strong with matured markets outpacing India and Middle East in large deals.

Orders from Q1 and Q2 have yet to be fully realized in terms of non-license revenue.

Large public sector momentum in India/Middle East is saturating, so focus has shifted to NBFC and private banks.

Note: NBFC are in sweet spot, may invest more in technology.

AI:

Levering AI, significant investment in AI, to increase Productivity, employee engagement, Decision making, policy.

AI central to new products; Management project 20-30% productivity improvement over 2-3 years.

Employee headcount down by ~100 YOY.

AI seen as both opportunity and disruption risk; continued investment essential.

AI is driving new use cases and expanding product scopes. Company stays ahead by investing and adapting quickly.

Order book:

20% annual growth is better than previous year. Conversion of order book to revenue should improve over the next 2 quarters.

System Integrator (SI) Channel:

It took time to develop, but now delivering results, especially in major markets.

Direct sales remain primary. SI is expected to grow slowly and is not break even yet.

What is System Integrator, You ask?

Combines various hardware, software, and networking components from different vendors into a single, cohesive, and functional system. They bridge gaps between different technologies to create unified IT infrastructures, implement new software, automate workflows, and ensure all parts of a system work together seamlessly. TCS, Infosys and Wipro like companies.

Disclosure: Invested.

3 Likes

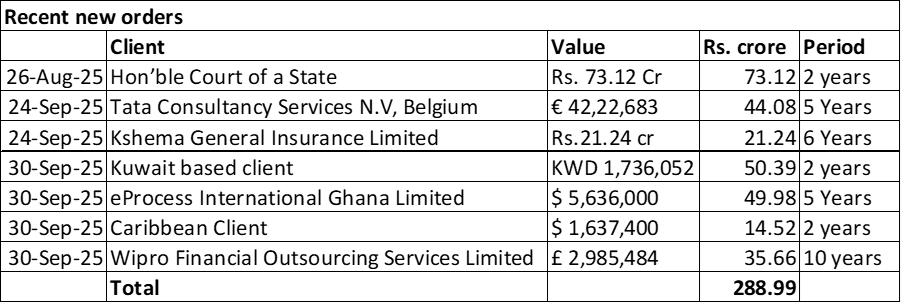

Kuwait based company order of KWD 1736052 (aprox 50cr ) has been revoked by the customer on 5th dec,2025.

Any reason to worry ?? Is newgen loosing customer due AI or competition??

Or just a regular business dilemma ?

Any idea anyone?

This may be due to esop and rsu