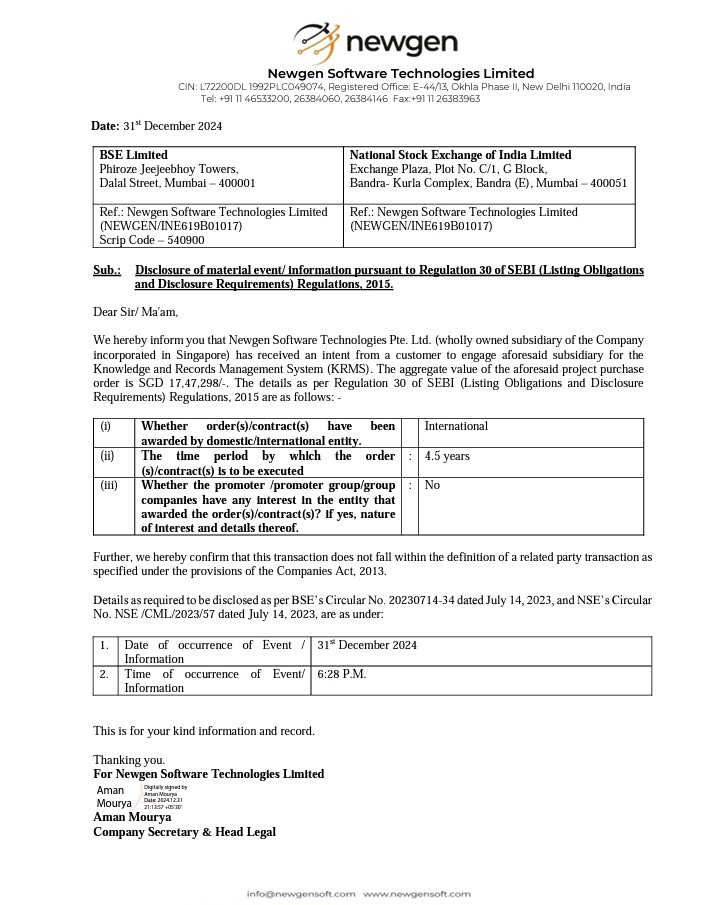

Newgen Software Technologies Pte. Ltd. (wholly owned subsidiary of the Company incorporated in Singapore) has received an intent from a customer to engage aforesaid subsidiary for the Knowledge and Records Management System (KRMS). The aggregate value of the aforesaid project purchase order is SGD 17,47,298/- (Rs.109455289.69).

Time of execution 4.5 years

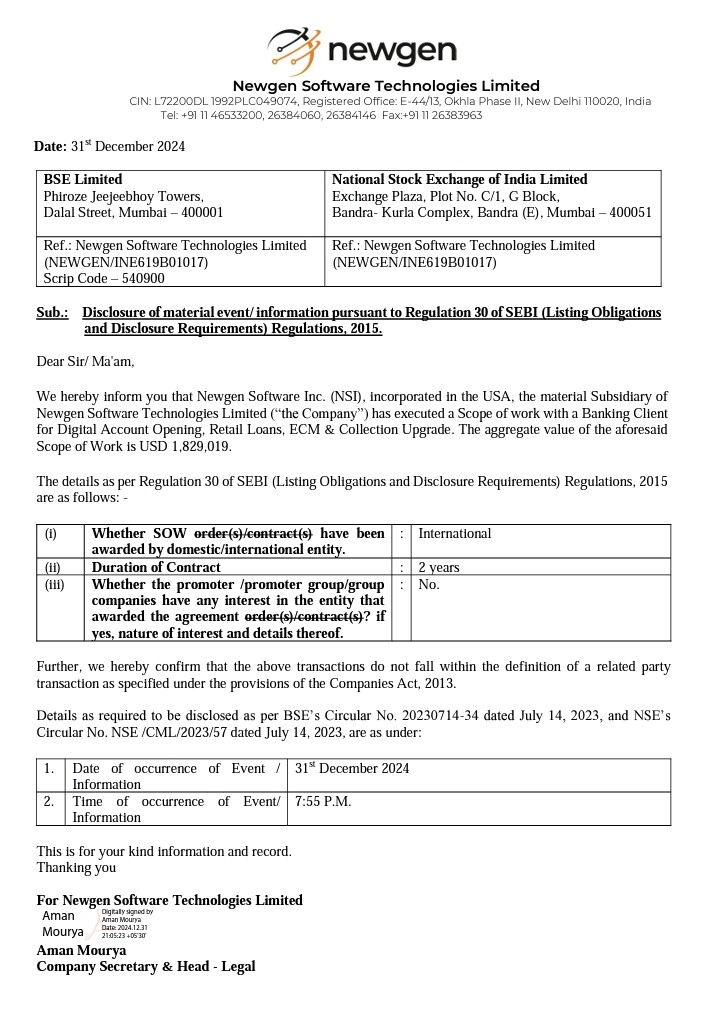

Newgen Software Inc. (NSI), incorporated in the USA, the material Subsidiary of Newgen Software Technologies Limited (“the Company”) has executed a Scope of work with a Banking Client for Digital Account Opening, Retail Loans, ECM & Collection Upgrade. The aggregate value of the aforesaid Scope of Work is USD 1,829,019.

Duration of contact 2 years.

Newgen Software Technologies Limited (“the Company”) has accepted the Award Letter from the customer for the Provision of Credit Automation services. The aggregate value of the aforesaid Award is USD 1,643,256 inclusive taxes.

The time period by which the order (s)/contract(s) is to be executed 5 years

Newgen Software Technologies Limited (“the Company”) has received and accepted the Purchase Order from a customer for the Newgen Remittance system- License cost. The value of the aforesaid purchase order is INR 208,978,000.00/-(inclusive of applicable taxes)

Time period by which order to be executed 1 year

Disc :- invested