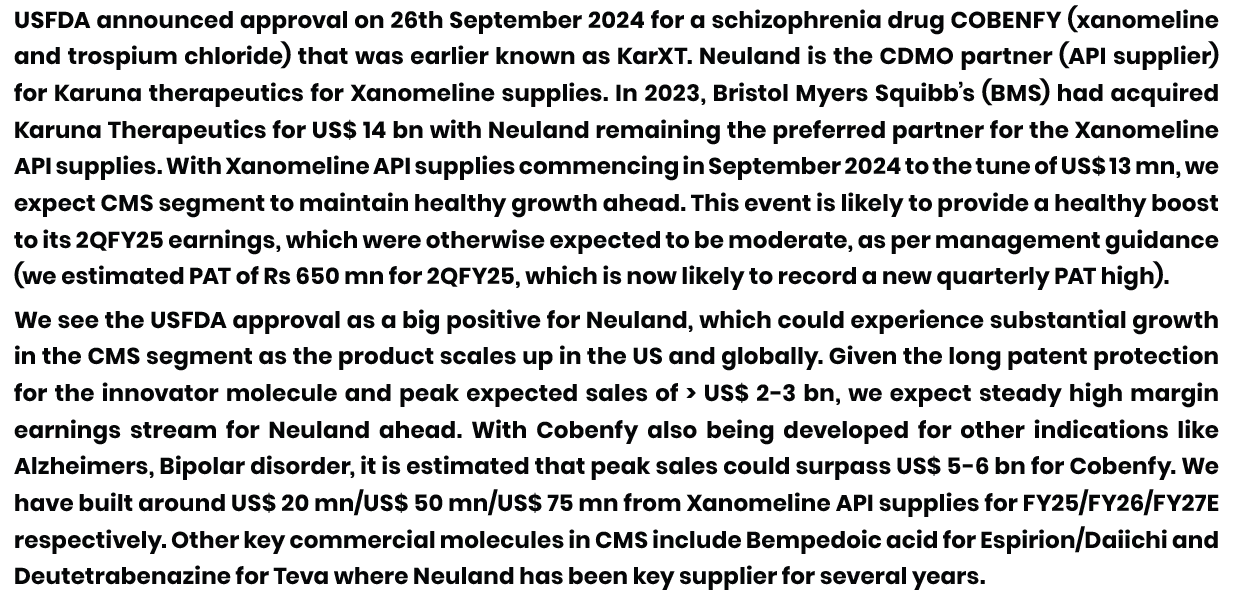

@jeet1990 Neuland is the API supplier for KARXT, who is the formulator.

Are there any other supplier for the API Xanomeline.

As far as I know, which is limited, Neuland is the sole supplier of Xanomeline. I don’t know who the formulator is as those details have not been disclosed. My best guest is BMS will be the formulator or would have had some plan for formulations before they acquired Karuna.

Does anyone know the monthly export figure (December)?

Where can we track the export data of Pharma companies? Is it Volza or is there more accurate and reliable data source other than Volza for Pharma companies?

No correlation between export data and their quarterly results, management has already pointed this and has been case in the past too - the problem is sometimes they also sell to indian pharma cos who use their ingredients and export it further, which is not accounted and even the booking cycles vary

But the 80% export they have mentioned they do, it must be direct exports only right?

Yes the self reported sales to US/EU clients is export data but they don’t release monthly figures or details of exports as it is confidential.

Neuland Announces New Vision and Values Statements

Neuland’s 3QFY25 export shipments declined 5% q/q. Its Bempedoic acid shipments declined q/q from $8M to $6M and its Kar XT shipments went from $10M to $7M.

There is no chemical called KARXT ![]()

What’s the source for the same? Which report/database?

The company doesn’t publish any export data. Any figures you read online are broker’s estimates. Take it with a pinch of salt. If you have questions you may email the company directly and they will tell you the same.

Good news from Neuland.

Track record of management had been to sensibly allocate Capital for CAPEX.

Very insightful information from Saharsh…

We are pleased to announce that we have successfully filed the USDMF for Empagliflozin API. This milestone reinforces our commitment to providing high-quality, regulatory-compliant APIs to global markets.

Results are in line with estimates. Management tone has further strengthened future growth prospect.

“This quarter’s revenues were driven by several important molecules in the commercial CMS and

GDS segments. We expect the recently commercialized molecules to scale even as we are on track

to enhance our manufacturing capacity. There is good traction from our existing customers

reverting for multiple projects as well as fresh interest from a range of new customers.*

We are seeing increased interest in peptides leading to our recent decision to invest in a larger capacity.

Overall, we are confident on the business momentum for the medium as well as long term.”

Neuland results and Concall Updates :

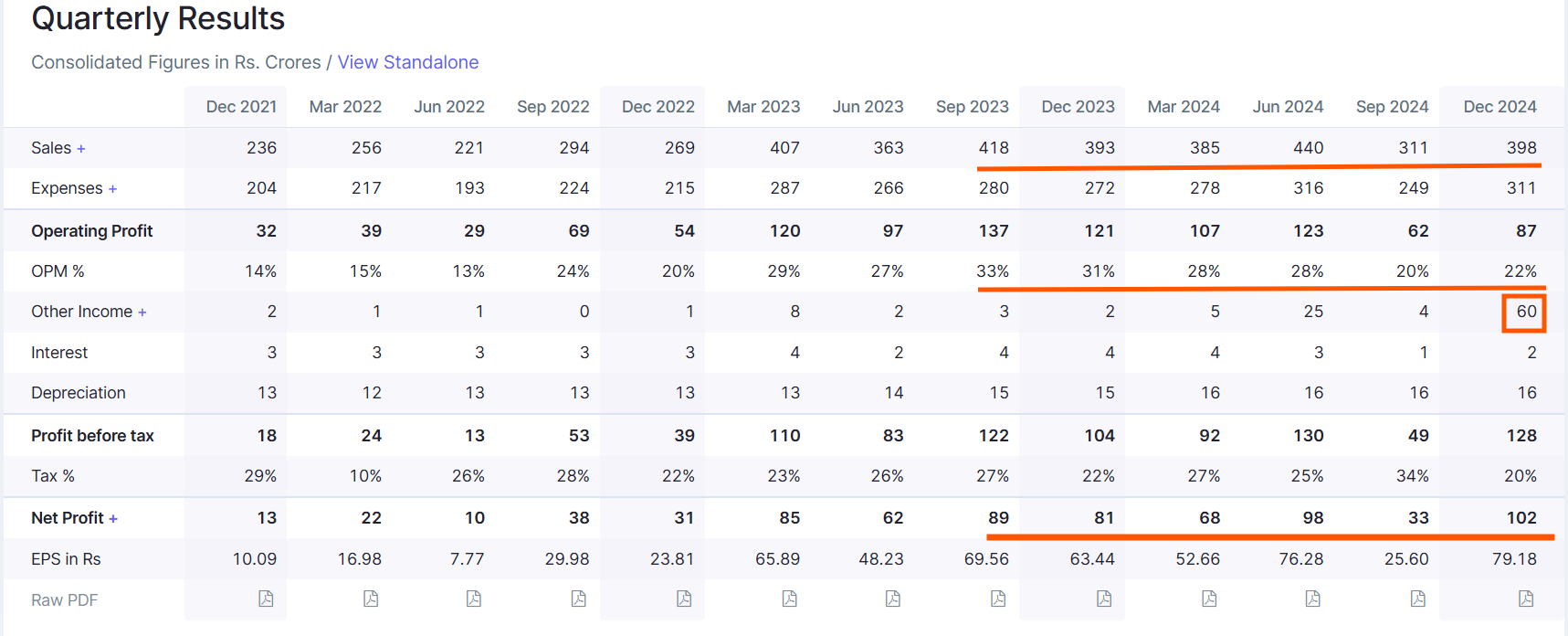

Topline is flat YoY but margins have dropped big time. The PAT has grown due to 60 cr of other income from property sales.

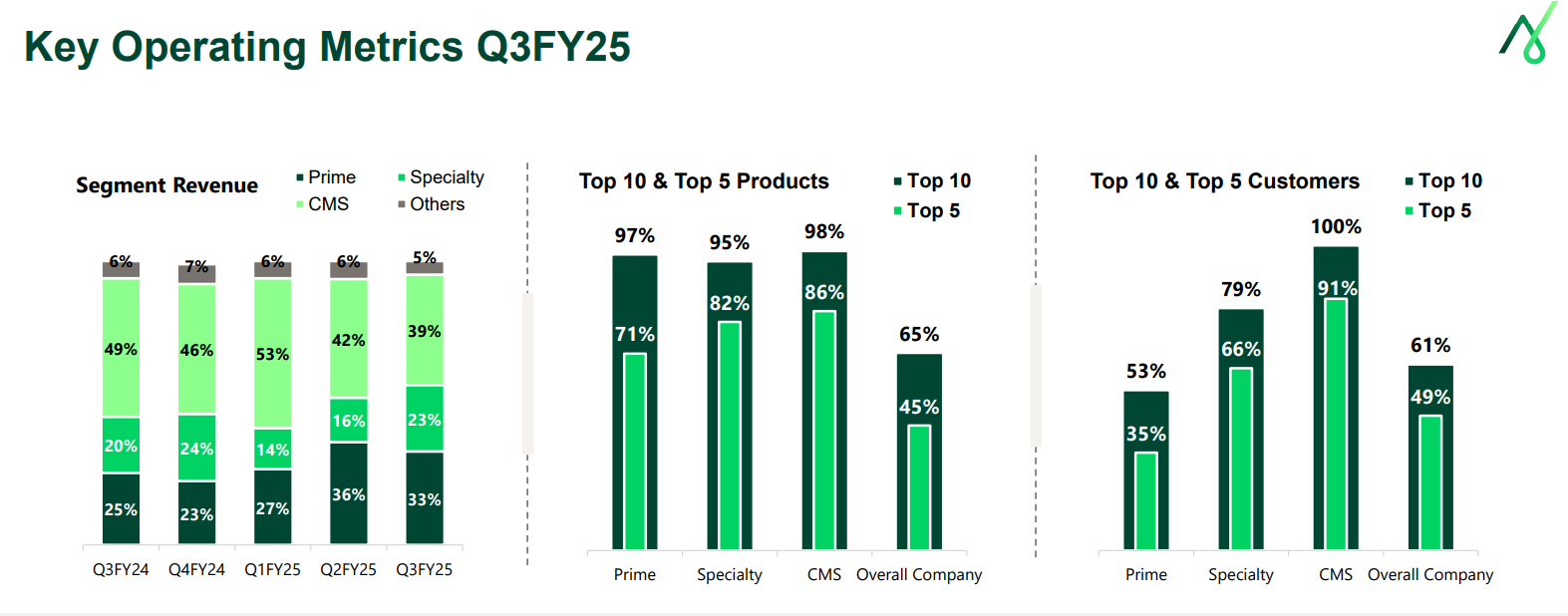

CMS business share to overall revenues has dropped by 10% which is made up by Prime molecules in GDS (Reason for lower margins).

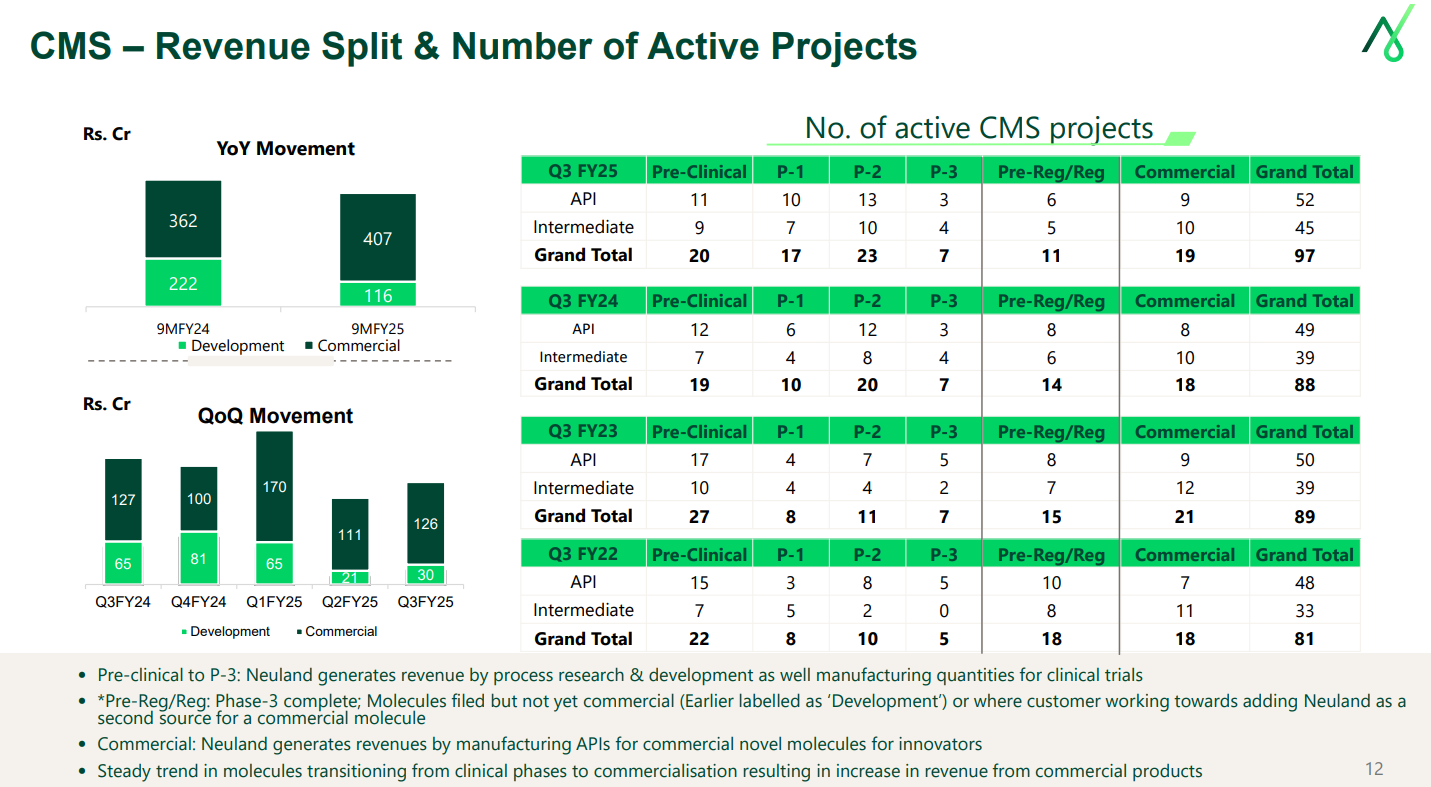

During the 9M YoY, while at a commercial level, the revenues have grown, the development revenues has shown marked drop. (Please note that overall number of projects in commercial and development have not dropped).

CONCALL NOTES

- FY 25 revenues to remain flattish . Growth to come back on FY 26 .

- Most of their customers are small molecule Biotech companies ( They are just called Biotech .They are innovator synthetic small molecule companies ). Neuland doesnt do any biotech stuff .

- New 250 cr capex approved for Peptide facilities which includes enhancing current capacities, New large scale facilities and Increase in R&D capabilities .

- This new peptide facility is to be used for both GDS and CMS facility . There is no anchor client . 2 DMFs for Generic business to be filed : Tirzepatide(GLP-1) and Difelikefalin .

- Other GLP-1 peptides are also being evaluated . Current planned peptide facility should be one of the largest coming out of India.

- In the CMS part of the business , they have only few molecules which are high value . The revenue projections are given based on the dispatch schedules of these molecules (Read: Xanomeline and Trospium Chloride-CARXT for BMS, Bempedoic Acid for espirion/Daichi, Duetetrabenazine for Teva)

- Min 1 if not 2 molecules from preclinical to become commercial in FY26.

- Sharp drop in development revenues due to 1 molecule in previous period with higher trial activity volume dropping from development bucket.

- Most of the client for Neuland is small biotech. Only if big pharma acquires some any of these biotech (As in the case of Karuna being acquired by BMS) do they engage with big pharma. Even if big pharma acquires they dont usually change the API supplier due to registrations and to mitigate the risk.

- Management doesnt foresee any major tariff related risk.

Neuland is the story of value migration from low value Prime API s to high value Specialty and CMS business . They have over the years built a solid foundation and FY 24 seemed to be the inflection point in their growth and the market did recognize the same. The management seemed bullish in their FY26 guidance and in Q4 they have to clock 410 Cr to just close flat.

Disc : Invested . DYDD

I understand it’s very hard to predict the future sales and profits for the company. However, the management has given guidance for 20% growth for the next 4-5 years. I am making my estimates based on this statement.

Sales growth: Let’s take 25% growth YOY. I am optimistic management will overshoot their guidance

NPM: 18%

PE Multiple: 31 (Last 10-year average. It is still on the higher side)

Current Market Cap: 15,250 cr.

FY 25 is assumed a flat year.

| Sales | NP | Market Cap (cr.) | |

|---|---|---|---|

| Mar-25 | 1550 | 300 | 9300 |

| Mar-26 | 1938 | 349 | 10811 |

| Mar-27 | 2422 | 436 | 13514 |

| Mar-28 | 3027 | 545 | 16893 |

| Mar-29 | 3784 | 681 | 21116 |

A lot of the growth has already been discounted in the current price.

Concal Summary : Q3:

We generated a free cash flow in the nine months of Rs. 70.8 crores. We also paid some of our term loan debt of around Rs. 27.2 crores. Consequently, our net debt position stands at a negative Rs. 185.1 crores (i.e Cash of Rs 185 Cr)

As part of our investments, we have invested Rs. 147 crores in capital spends during the nine months and we are committed to balancing growth and profitability by continuously optimizing costs and processes to ensure long-term sustainability. We are progressing as planned towards completing the new production block in Unit III and expect to commence commercial production in FY26, which is also going as per plan.

Conclusion: No Debt , Positive free cash flow of Rs 70.8 Cr after CAPEX of Rs 147 Cr and debt repayment of Rs 27.20 Cr. Net Cash of Rs 185 Cr available in the balance sheet for future CAPEX without raising any additional debt.

While we expect FY25 to be flat, we remain confident that our business will regain momentum from FY26 based on significant order pipeline and customer demand. Overall, we continue to be cautiously optimistic about our future, potential that our business holds.

Conclusion: Momentum to regain from FY 26 on the basis of significant pipeline and customer demand.

Our business is uneven due to the inherent characteristics of the CDMO business, as well as the specialty GDS business, which is focused on small volume products. As a result, evaluating Neuland’s trajectory on an annual basis is perhaps a more accurate measure than comparing quarter-to-quarter results. Again, there may be the odd year also where the trajectory will not be clear due to the specific mix or how products are taking off.

Completion of manufacturing facilities coupled with the scaling up of commercial molecules on the CMS side gives us a great deal of confidence of achieving our stated objectives in FY26 and beyond.

Conclusion: Nature of business is lumpy and trajectory to be monitored on an Annual basis, however new molecules and ongoing CAPEX give predictability of future growth potential.

We continue to see increased interest in customers wanting to partner with Neuland as they look to bring in their innovative medicines to patients.

And I think many ways this can be attributed to three factors.

- Our reputation is continuing to grow as a result of the work we’ve done over the last couple of decades, especially on the CDMO business.

- Our business development teams who are also seeking new relationships are getting increasingly focused on finding the right opportunities that actually fit our long-term strategy. So, being very selective, very decisive in whom we want to work.

- The macroeconomic factors which we all have been talking about also have been favorable to us.

We are therefore enthused by the range of customers expressing their interest in working with us. And that’s what’s kind of giving us excitement about this business.

Conclusion: Decades of hard work done in CDMO is now at inflection point and Company is now able to partner with right kind of customers with tailwind from macroeconomic factors. (Right time right place.)

We are seeing good traction in terms of early-stage projects as well as customers reverting to us with more projects in their pipeline. So, we expect the buoyancy in the CMS business to continue going forward and don’t have any concerns at the moment. On the GDS side of the business, we remain focused on innovating new specialty products while optimizing processes and expanding market share for the key commercial API’s. The specialty API business actually the growth is back on track this time. We are confident that we are on course to meet the overall targets for the GDS segment for the year.

Conclusion: Management is Positive and confident on growth of GDS as well CMS business.

As many of our long-term investors know, Neuland has invested in the peptide space for the last 15 to 17 years. We, in fact, have a team of around 50 peptide chemists who work in our R&D side, and they have delivered multiple projects at lab at small scale. We’ve now reached a juncture where we need to enhance our peptide capacity to scale our business to the next level, even as we have received a lot of interest from customers in our capabilities and as we all know peptides are being considered a new modality for increasing the number of therapies. So, this led to the announcement of the capacity enhancement for which you would have seen the press release and the disclosures.

Conclusion: 17 years of work done in Peptide segment is at inflection point and Company is incurring further CAPEX to utilise this opportunity to full potential.

Neuland flexibility and agility are crucial for effectively responding to the business environment and our growth strategy remains focused on pursuing high value molecules from innovative companies, both on the CMS side and the GDS side. And we are committed to enhancing customer experience, which we believe that distinguishes us as a distinctive API provider. So, our commitment to the future is evidenced by our investments in enhancing our capacities as well as capabilities adhering to our foundational values of customer centricity, agility and operational excellence. Neuland is well positioned to capitalize on long-term opportunities, even as we continue to navigate any short-term challenges that may come our way.

Conclusion: Company has focus and strength in both CMS as well as GDS (Complex) molecules.

Peptide CAPEX: Majority is going into creating a large-scale facility which does not exist today. A small part into the pilot facility and a much smaller part into the R&D facility. With this investment, we will have seamless capabilities from lab to pilot to commercial for peptides. Having said that, the idea is to create facilities which would be usable for both the GDS business as well as the CMS business. There is not one anchor product or one anchor customer for which this investment is being made. We are looking at it as an opportunistic investment to kind of take us into that peptide domain by giving us a larger piece of infrastructure.

Peptide Capacities : Small molecule business, right, where 1,000 KL means something very definitive, in peptides, this whole KL business is a little tricky. So, I am not quite sure if it’s an apples-to-apples comparison. From what we know about the space, and I think based on, you know, all the work we’ve done, we believe it’s a substantial investment and it is a fairly large scale facility and it should provide meaningful volume of peptides. But yes, again, I don’t know much about the infrastructure of WuXi, so it’s difficult for me to compare, but I know it’s a big jump up and it would probably be one of the large peptide facilities at least out of India.

Conclusion: Peptide CAPEX is being done looking into future opportunities in both GDS as well as CMS segment and the CAPEX has not been committed for any specific product or customer and management is positive on further CAPEX in peptide depending on the future opportunities and conditions.

The upcoming Peptide CAPEX is a big jump for the Company and it would probably be one of the large peptide facilities at least in India.

Biologic Vs Small molecule: But you’re right, as in there seems to be some sort of reversal, maybe because costs are more attractive in small molecules. Maybe the formulations are more easier, but again, not the experts to comment further on that. Sorry.

Conclusion : Traction of Big Pharma is inclining towards small molecule segment which is forte for Neuland Labs

New Commercial Molecules : One, at least, maybe two, but we will have to wait and see because again these are still going through trials and filings, etc. But one, we are fairly certain will happen in the next year.

Guidance on Peptide revenue: Sachin, at the moment we would not share anything because I think it’s a very wide range and I think maybe over time we will probably be able to give a better color because again it depends on what molecules scale up over there and therefore there is a very wide range and it might not be very helpful for you guys. But I think maybe in the course of time, we will try to give a little bit of color on that. But for now, maybe we will just hold off.

Big Pharma Vs Biotech business and product mix:

Yes, so I think the Big Pharma Biotech split is something that we don’t have but we’re largely a Biotech company and as we stated also in the past. Usually if we are working with Big Pharma it’s either for a very specialized area like peptides or it’s because Big Pharma has come and acquired our customers We don’t have that mix and we will see if we can provide that maybe at a future date But you can presume that we are largely biotech focused. With regards to a multi project customer and we do have several customers that we do multiple projects with and we don’t have the number for that maybe that is something that we get back to you. But I would say maybe at least 20%-30% of projects are second or third projects with the same customer and its just an intuitive number.

Conclusion : Neuland is getting business mainly from biotech Companies but business from Big Pharma is gradually increasing due to acquisition of Biotech Company by Big Pharma or due to specialised projects like Peptide from Big Pharma. Repeated orders are coming from same customer. Big Pharma relationship and business can be a game changer for Neuland in future.

Customer Stickiness in CMS segment i.e difficult to replace:

Point number one :

What we have observed is that because there is a regulatory filing involved and Neuland is registered as an API manufacturer, there is anyway a certain level of stickiness that is involved with our site. So, it’s not very easy to displace Neuland as an API company even the Big Pharma is not very familiar.

Point number two,

I think even from a Big Pharma perspective I think they just look at things from a risk point of view and as long as they feel comfortable that this company that is currently producing the API is not going to create any significant risk for their API supply, they would tend to continue working with us.

Third point

Ultimately the long-term relationship is dependent on our ability to execute and deliver. And I think that’s where the relationship is built. And I think that’s the journey that Neuland has is kind of going in right now. But I think just given the advanced nature of these programs, even if there is not a lot of familiarity with Big Pharma, we have not seen any kind of reluctance or hesitation to work with a new API supplier, provided the risks are manageable. And I think that’s where Neuland stands out, because our facilities, in terms of our quality management system, in terms of our ESG practices they all are top tier, not just in the country, but even at a global level. And that also creates a certain level of comfort for these large MNCs when they come to evaluate Neuland as an API company.

***Conclusion : It is extremely difficult to replace the API supplier in CMS business which makes stickiness of business for API players like Neuland. ***

***On the other hand , Pharma Companies always look for alternate source of API supplier which have proven track record of risk management, quality management systems, ESG compliance, facilites etc. ***

***Neuland fits in all such criterion with top rank not only in India but also Globally and this creates a comfort level for large MNCs when they evaluate Neuland as API Company. ***

To summarise it on one hand Neuland business model is sticky with its client while on the other hand because of it capabilities it can always be an alternate API supplier for Pharma Companies in CMS segment (at Clinical Trial Levels or Post commercialisation).

GDS VS CMS:

Yes, sure. See, I think Neuland as a company, I think for us, the GDS business is as important for us as the CDMO business. And in many ways, they’re not really competing with each other, right? Because ultimately, there’s a lot of synergies in these businesses and they cater to different customer segments. And because of that, our strategy over the long term is to pursue both the businesses environmentally. However, the way we have nuanced our approach in the GDS business is to try to move a little away from prime and go deeper into specialty. And we believe that going into specialty gives us the ability to command that market share leadership, which sometimes is very difficult to achieve in the prime products where price tends to be the key determining factor. So, I think over a long-term perspective, I don’t want to get into the growth rates and the business mix because again that’s too detailed kind of guidance that we would give but ultimately both businesses our idea is to grow them to their best potential. Even if you take the example of the new peptide facility, it has been designed to cater to both GDS customers and CMS customers. And ultimately, what products, what segment will do more revenue in the peptide facility remains to be seen. So, I think that’s the effort. And but however, I think we will not focus as much on prime just because it’s not really area of our strength to compete on price, but we will focus more and more on specialty products. And eventually, a molecule like peptide will also become a part of the specialty portfolio.

Conclusion: Company will continue to focus equally on GDS as well as CMS segment, however in GDS main focus will be on Complex and specialty API i.e higher margin products. CDMO opportunity is higher in future.

Cost of API in final drug Product:

It’s actually, I think maybe this question was asked in the past and it’s a very difficult question to answer because there is a very wide range of what percentage an API could be in terms of the final drug product pricing. We’ve seen products where it could be as high as 10%-12%. We’ve seen products where it’s like 0.1%. And honestly, I think it’s very difficult to be able to determine even for us what would be appropriate number to take. So, I think maybe it’s a very, I am not quite sure how much we can help you on that front. So, maybe if you can go ahead and ask your next question.

Conclusion: Cost of API varies from 0.1% to 12% and hence no fixed formulae.

IMPACT OF US TARIFF:

I think, we have considered all possibilities, and we have also as part of our enterprise risk management, we kind of look at all kinds of risks including tariff risks, geopolitical risks, etc. I think just looking at all possible scenarios, I think one thing to consider, I think just from a Neuland perspective is that we make APIs, right? We don’t do drug product. And most of the APIs we make are, the alternate sources are either in China or in Europe or in India. There’s not a lot of captive capacity for these APIs in the US. And therefore, it seems very unlikely that tariffs could be affecting our business directly. But having said that, I think also take into consideration that for most of the products we operate on both in the GDS and CMS side, we are typically one of the only suppliers or maybe one of the two suppliers and a supplier risk would actually harm US patients. And that’s also something to be taken into consideration. And yes, so I think for us we will have to figure it out. I think worst case, also understand our business. We, I think almost all our CMS as well as GDS specialty customers consider us to be partners. And if something substantial like a tariff would happen, we would work with the customer to ensure that that tariff cost is absorbed by the customer to ensure that there is a seamless supply of material. I think these are the few responses maybe I can offer

Conclusion: No major impact and management has given a deep insight on this with reason.

Future Outlook:

I mean, I think the outlook we’ve given about growth resuming in FY26 is at an aggregate business level. It is not at a segment level or at a product level. So, what we would like you to just take away from our message is that you can expect Neuland’s business to grow in FY26. It grew well in 24. It was flat in 25. And you can expect the growth to come back in FY26. I think that’s the only message we have given. Beyond that, we will not be able to give any further details to it.

Clarification on Biotech nomenclature:

No, I think maybe the confusion also comes because we call these companies as biotech companies but essentially these are all small molecule companies. They don’t really do any biotechnology work or they don’t do any biologics. The products Neuland makes are all small molecules, so they are synthetic and chemistry based and they are not biology based. It works similarly in the generics business. Our customers, these biotech companies procure the API, they get them formulated at another CDMO, packaged and then sold. But the entire product value chain is only synthetic and there is nothing to do with biology. I think perhaps what can create a confusion sometimes is that because the industry nomenclature calls these small and mid-size US-based companies, they are called as biotech companies. Ironically, although they don’t do biotechnology, they are called biotech companies. But as you know, we are not in the biotech space. And therefore, we are not involved in creation of any biologics. I hope that clarifies. I know it may not be a comprehensive answer, but I hope it helps.

Final Conclusion:

As guided by management FY 25 shall be flat and growth will start from FY 26 onwards. Company seems to be at inflection point and lot of exciting and promising opportunities are awaiting in future.

Business and Management quality is impeccable it is has a proven track record of 3 decades and 2 generation.

Read the concal for 3 -4 times and it was an absolute pleasure reading it and getting insights of the business.

Disclosure : Invested since 2021 and have substantial holding and hence views are biased. Not sold in current correction and my holding period is at least 5 years from here