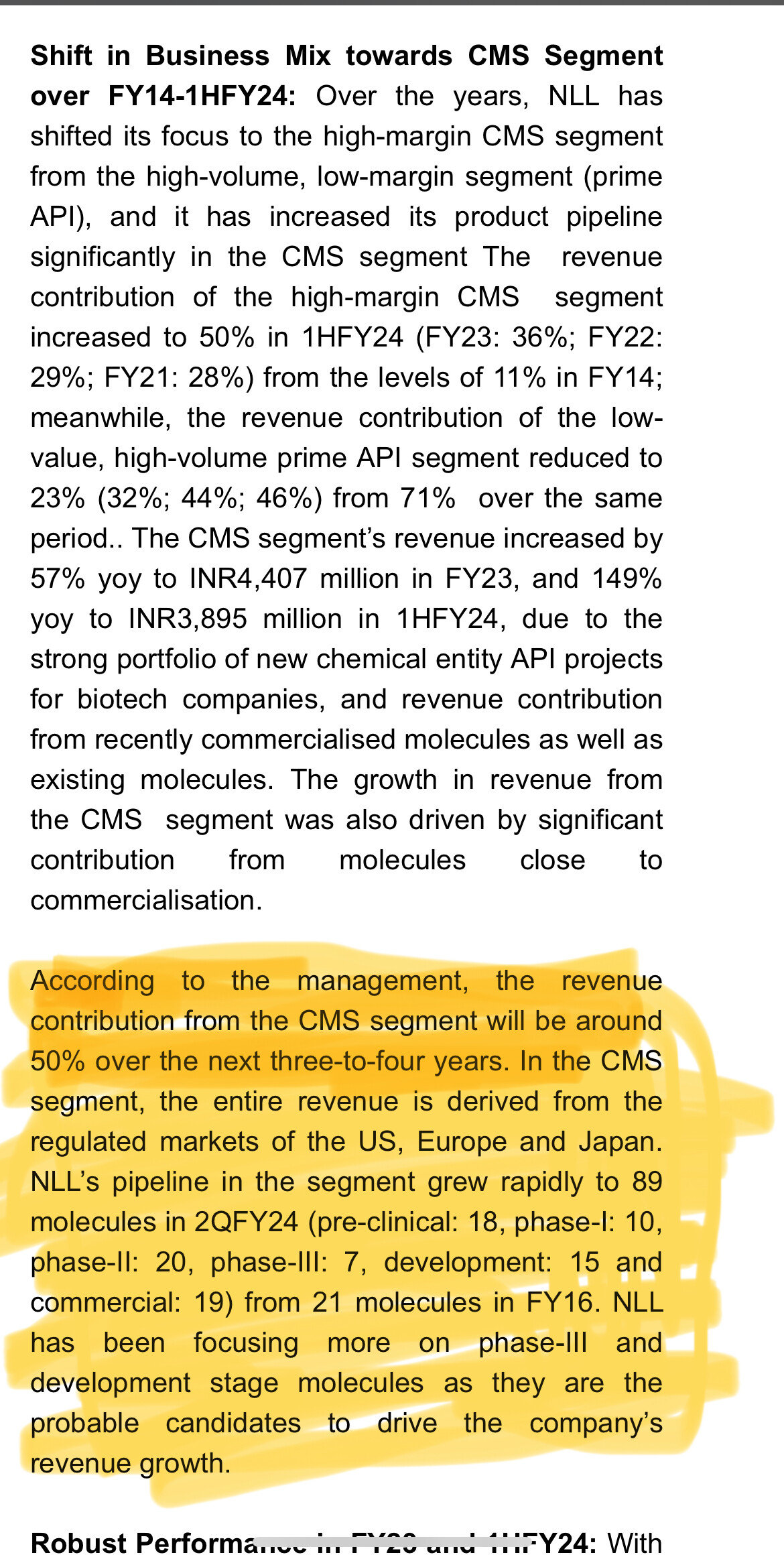

Ratings improved as expected , Rating rationale worth reading to get confirmation of your conviction on the Company.

Investor presentation for Q3 2024

Ratings improved as expected , Rating rationale worth reading to get confirmation of your conviction on the Company.

Investor presentation for Q3 2024

NLL, on the basis of an approval received from Telangana State Industrial Infrastructure Corporation Limited, has entered into a joint agreement with a developer for the construction of an information technology park at the company’s land in Nanakramguda, Hyderabad in FY21. This investment property carries a book value of INR189.1 million; the management reiterated that it expects a much higher fair value (i.e. 4x-6x of the current book value) to accrue to NLL once the construction is completed. This asset sale amount can be then used for the guided capital expenditure

the above info is from credit rating report

Is KarXT the molecule near commercialisation management was alluding to in last 2 voncalls?

Maangement had never referred specifically to KArxt molecule in any of its concal.

Thx. I never said that, they did… they have been saying couple of molecules are near commercialisation…just trying to understand if KarXT is treated as already commercialised or not… may be that’s the question for concall now

What was the most important key learning from the con call today?

Guided for moderate growth in FY25 with acceleration in FY26 and FY27. Overall 20-25% growth over the next 4-5 years.

Neuland Labs

Q3 FY 24 concall highlights -

Sales - 394 vs 270 cr, up 46 pc

EBITDA - 122 vs 55 cr, up 124 pc

PAT - 80 vs 30 cr, up 165 pc

Segment wise sales break up -

Prime APIs - 25 pc

Speciality APIs - 20 pc

CDMO - 49 pc

Others - 6 pc

Segment wise contribution from top 5 products -

Prime APIs - 80 pc

Speciality APIs - 67 pc

CDMO - 91 pc

For 9M FY24, Breakup of CDMO sales -

Development - 221 vs 96 cr YoY

Manufacturing - 362 vs 165 cr YoY

No of molecules in various phases of development / manufacturing ( APIs + Intermediates ) -

Phase 1 - 19

Phase 2 - 20

Phase 3 - 7

Pre Commercial - 14

Commercial - 18

Company is Net Debt free

Capex for 9M FY 24 @ 68 cr

Expect a 20 pc kind of CAGR for the company over next 4-5 yrs ( although the journey won’t be linear )

FY 25 may be a moderate growth year. Expect growth to pick up post FY 25 as more molecules (as expected) go commercial

When a biotech customer of their’s gets acquired by a Pharma major ( as was the case with the acquisition of Karuna Therapeutics by BMS ), it opens up several new business opportunities for the company

Since Neuland works with a lot of small Biotech partners, a prolonged funding winter for these Biotech companies may be a risk wrt new business for Neuland

Current capacity utilisation of Unit-3 is 57 pc. Company has still bought land adjacent to Unit-3 for further expansion

Company has 03 generic molecules in its pipeline. Will file DMF for one of them in this calendar yr, in the next CY for the other two. All these are lucrative molecules

Company has 02 peptide molecules in their CDMO pipeline which are nearing commercialisation. However, company is not the primary supplier for these molecules

Company owns a commercial property which should end up being liquidated in next FY. Expecting an exceptional income of aprox 100 cr from that property

Capex lined up for next 2-3 yrs @ 100 to 120 cr/yr - in that range

Disc : its a major portfolio holding for me, biased, not SEBI registered

Key Takeaways from Q3FY24 Concall -

a) Sucheth Remarks: We are investing in people and infrastructure to deliver on our long term plans. Company is doing expansion by adding new manufacturing facility. Employee cost increased compared to last couple of years.

b) Saharsh Remarks: Business is seeing increasing interest from customers with exciting pipelines ahead and as the quality of business grows, company is gaining better visibility of future and planning accordingly.

c) Generated FCF of 129 Cr in 9 months have utilized partly 39 Cr to reduce debt and CAPEX investment of 68 Cr for enhancement of capabilities. Working capital cycle has reduced from 137 days to 118 days in 9MFY24.

d) There is Product and customer stickiness; Top 5 Products in CMS contributes 91% and Top 5 customer contributes 95% to revenue. Company has majorly 5 customers in CMS business|

e) Company have done CAPEX of INR 68 Cr in 9MFY24.

f) CMS - We see strong interest from customer, led by increasing interest from customers with large pipelines which further solidify’s Neuland position in CDMO market.|

g) Unit 3 operating leverage continues to play but as a matter of fact Unit 3 was operating at lower utilization levels for 4 year period before it picks up.

h) We expect FY25 to be a moderate year of growth with some normalization of margins due to higher operating expense due to ongoing investments but effective FY26 we have better visibility of growth and aspire to grow 20% CAGR for next 5 years.

i) The new capacity coming up will be the scale up of existing molecules and new ones yet to be commercialized from the capacity we are creating for FY25.

j) In the past based on our experience whenever small biotech company got acquired by large big pharma, this opened new doors of opportunities to expand our business with new company.

k) There are multiple factors which comes into play to make sure big pharma sticks to old CDMO partner is a) How complex the molecule is? If the complexity is high, customer stickiness will be high and b) if you are closer to NDA and you have validated the process at your side and your site is registered to the NDA there are less chances of changes while if molecule is going thru Phase I or II then the risk of losing partner is high.

l) On the biotech funding on the molecules which are driving growth for us in the CMS sector are all coming from companies which don’t require funding and are cash-rich. But we can see impact in molecules which are in Phase I or II but that’s also temporary.

m) Supplier or CDMO partner switch is not easy and depends on the complexity of molecules and may take minimum 2 years to change the API partner and can go upto 5 years based on regulatory approvals.

n) Current EBITDA margin is very favorable and won’t be sustainable. Note: Based on Management comments it appears 23-27% is the fair range of margin for Neuland given the product mix.

o) Regarding Peptides we have 3 molecules in GDS of which 1 we are expecting to file DMF and the other 2 in FY26. Also, in Management expectation GDS molecules also has very high potential compared to CMS molecules.

Very good summary! Just to add, while giving growth guidance, management has not considered peptides opportunity so that’s an upside as and when it materialises. Overall, Neuland as a CDMO & API asset should do very well and re-rate further. Quality of business is much higher.

This is to inform you that the Company’s management will be participating in the following group analyst/ investor meetings:

Date Meeting Organized by Location

March 7, 2024 ICICI Securities Limited Hyderabad

Pursuant to Regulation 30 of SEBI Listing Regulations, we wish to inform you that Mr. Ashutosh Kumar Sinha has been appointed as Chief Quality Officer w.e.f. March 6, 2024.

Mr. Sinha holds M.Sc. in Pharmaceutical Chemistry from Institute of Chemists, Kolkata and is an MBA in Total Quality Management (TQM), from Sikkim Manipal University. He brings over 28 years of experience in the Quality function, working across organizations such as

Ranbaxy Labs Ltd, Glenmark Pharma Lab, Dr Reddys Lab and Symbiotec Pharmalab. Prior to joining us he was associated with Syngene International Ltd. as Associate

Vice President & Quality Head (Small molecule & Client dedicated centre).

His area of expertise, within the pharmaceutical Quality, include functions such as Corporate Quality Assurance, Plant Quality Assurance, Development Quality Assurance

(API & Formulation), among others.

q3 results analysis

neuland q3 fy24 .pdf (2.1 MB)

can any one provide with his linkedin id please,

Price has sharply corrected over the last couple of weeks. Any news flow?

It looks like slight reversion to mean.

These small corrections in prices are healthy in the long run.

Personal opinion

Completely agree that a correction is needed given how its run-up. But i was asking since a 10% drop indicates some news flow typically