Not sure if this true

- Dexolac is sold as baby milk

- It is sold at DMART which is nothing but a kirana store.

Not sure if this true

Have you see any advertising recently for the NAN or CERLAC products recently in any media. I have myself bought NAN only from pharmacies.

I didn’t comment on advertising because it is true. My concerns were only two points ![]()

Not sure about DEXOLAC, i haven’t bought it , I have myself bought NAN only from pharmacies.

I have a pharmacy hence the comment.

Hi

The story of the moat which is weaved around on Infant Powder by a PMS actually originates from a 1992 regulation The Infant Milk Substitutes, Feeding Bottles and Infant Foods Act which got amended in 2003.

Attaching both the files. I have skimmed through these sometime back and disagree on one of the points (I agree that advertisement is not allowed). The point which says that only basis prescription it can sell is incorrect. It’s available online by non pharmacies, even cash and carry stores such as Metro in Bangalore etc.

Aside I feel this regulation is quite good not from a business point of view but from a baby’s health point of view. We have been years ahead in making this law compared to other countries.

Though personally I faced a problem when my kid was born as I had to try out a lactose free milk substitute. As far as I was told no official product existed. There was only black market lactose free powders which the pharmacies arranged. Don’t know if it were true. But I agree I never haggled infact that thought never even came in my mind. It was sold at a steep premium.

Rgds

Deepak

ind2651.pdf (1.3 MB) ind80042.pdf (521.5 KB)

@deevee Love your analysis and thanks for sharing the file. Let me ask you if NESTLE make fairly good quality milk powder (NAN), having more than 90% market share, no advertisements allowed, no new licenses, products for infants hence no one wants to compromise. Then how can any another company compete with NESTLE. Is it not a wide moat.

Hi @JJoy

Thanks.

It is one of the widest moats I have seen rather! People who are having their first child know very well of Nestle but would have never heard of Similac or the lactose free powders (I even forgot the brand name now since its been a few years!). The Nestle brand brings in a comfort level, a feeling of safety and care for new parents. And when folks have kids the second time around they usually would have had a good experience with Nan Pro.

I am speaking as a consumer rather decision maker.

We are perhaps overplaying regulation in this. Lets invert, hypothetically assume companies were allowed to advertise. What would happen to Nan Pro market share?

I feel it will actually increase!

Luckily one of my close friends used to be a senior manager in Nestle Nutrition and when I consulted him few years ago I got extremely good feedback on the processes and ethics of the company.

Rgds

forgot to disclose: i am invested in Nestle for sometime now.

Indeed it is strong moat. Only way to break it would be via doctors. I am aware in US doctors suggest brands based on baby needs and promote certain brands maybe based on their own choice or otherwise. Btw similac from Abbott is a strong growing brand in US. Gerber from Nestle sells equally well, is market leader…and lastly there is enfamil…so back there doctor’s advice rule the show and helps in growth and new customer acquisition…

Disc. Invested in nestle. Skipped Abbott for primary reason they sell similac in India via their unlisted arm.

Can you please mention the source of this information?

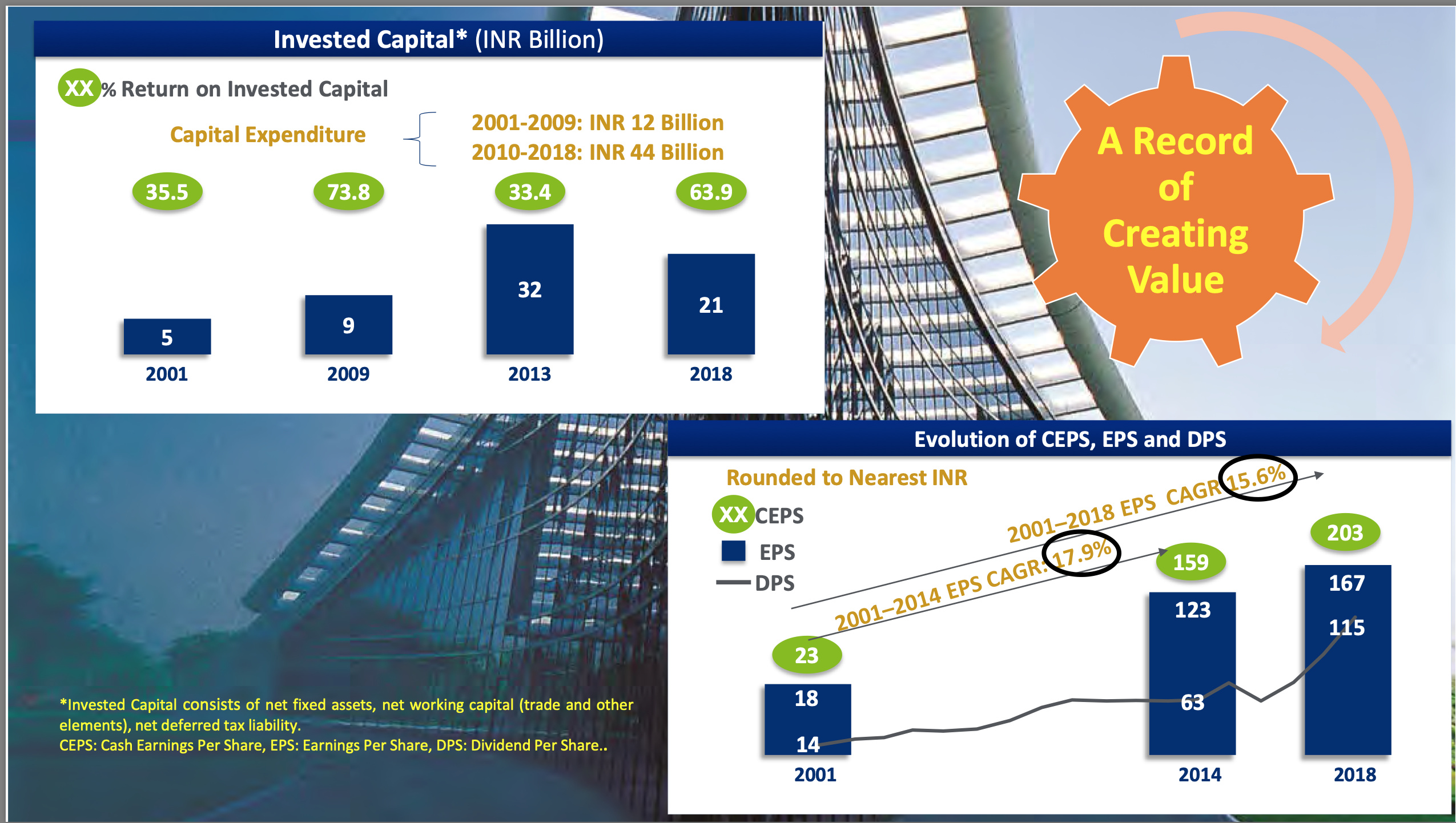

Nestle-India-Annual-Report-2019.pdf (4.0 MB) NESTLE Annual Report Page 9

NESTLE Presentation Page 9

Source:

This series of tweets summarizes the long term growth rates along with the market sentiment over the last 3-decades. A short summary:

1993-2003: Revenue grew @15%

2004-2013: Revenue grew @15%

2014-2019: Revenue grew @4.6%

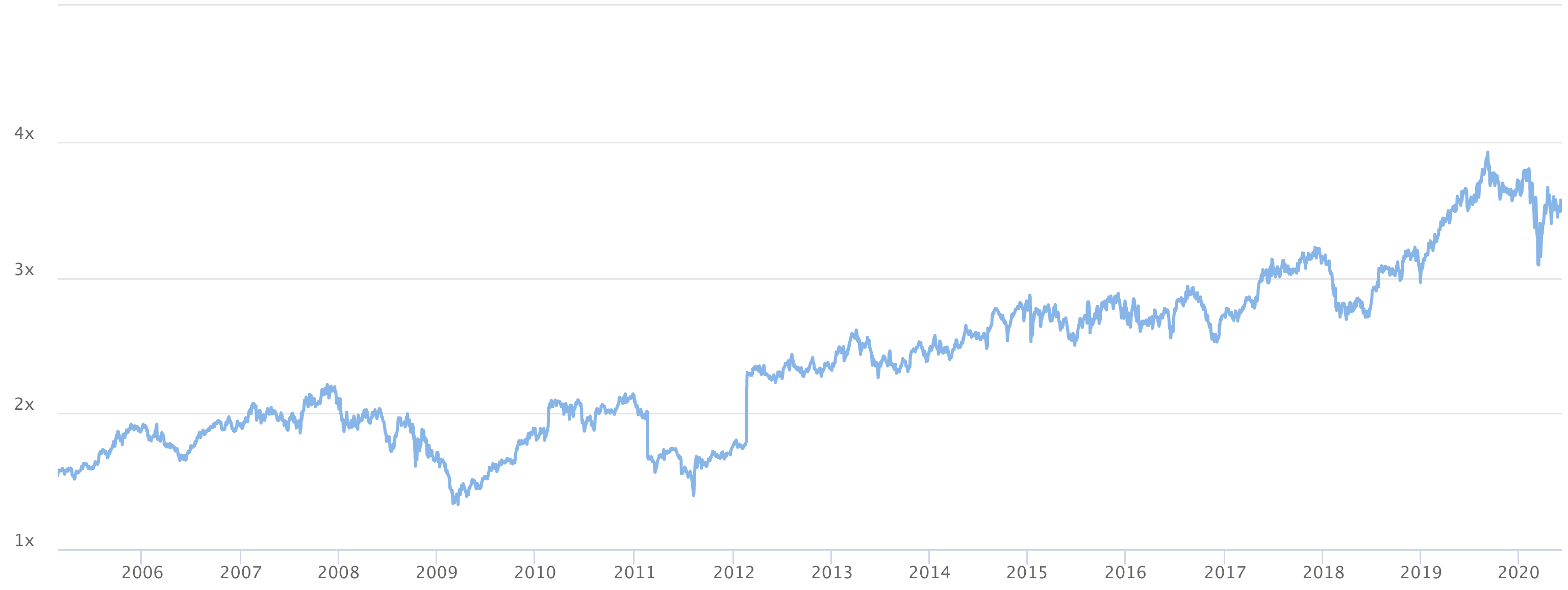

Over the years, the net profit margins have been remarkably stable at close to 12.5%. Margins have gone up only very recently (CY18, CY19) to ~16%, its anybody’s guess how sustainable these margins are. Long term valuations have varied between 2-6 times EV/sales. Only very recently (i.e. from 2016), EV/sales have gone beyond this range and is currently ~12.4x. For context, these are the EV/sales number for NESN (the global Swiss parent of Nestle) [taken from tikr.com] (@TIKR.com - is it okay to share data from the website on this forum?)

It’s not apple to apple comparison as this includes abnormal event viz maggi issue . If you adjust it for abnormality, it has in fact become more aggressive than earlier and shown stellar growth record ( comparing with other mature companies of its age ) and there are very very few of these viz Nestle, asian paints etc . Not even hul comes close to these . These never seem to age

Disc- Invested

Instead of using superlatives, its more important to focus on numbers. Lets account for the maggi fiasco which led to revenues declining to 8175 cr. in CY15. CY19 sales were 12369 cr. (11% growth). Extraordinary right?

These companies have high ROCE due to lower fixed cost and require only a small increase in sales to make profit spurt and hence high operating leverage . Since you like numbers ( I believe quality is not completely revealed in numbers) , in the same period that you pointed out sales , pat has increased from 563 crores to approx 2000 crores I.e just under 4 times roughly . Even if you normalize for maggi , still pat has doubled in 4 years which is not a low achievement for blue chip mature companies like Nestle.

I believe if one expects higher growth rate than this , one musnt look at such large cap mnc .

Moreover past is never a correct predictor of future in markets or many other things as the aggressive expansion that it’s now doing wasn’t earlier and maggi acted as a boost to their mgmt .

Disc- I hold Nestle and this is not supposed to be a recommendation to buy or sell and I am not a sebi registered advisor.

Rate of reinvestment and not ROCE determines future growth, high ROCEs without avenues for reinvestment simply means higher dividend.

As you have pointed out that profits have become 4x on a sales growth of 11% from CY15, you also should account for extraordinarily low profit margins in CY15. Over the last 30 years, Nestle India’s net profit margins (NPM) have averaged at around 12.5%. This is not only true for India, but also for Malaysia (~12%), Pakistan (8-12%), Nigeria (~15%), Sri Lanka (8-12%), and Switzerland (12%). The current NPM are ~16% which is higher than what was in the past.

About your point on operating leverage, it plays a much large role in asset heavy businesses where the gradual topline goes directly to bottomline (eg: auto, metals, etc.). When a company is reporting its highest margins compared to its recorded history, its more likely that operating leverage has already played out. Plus, to gain a better understanding of its future margins, it might be better for us to look at other Nestle subsidiaries (which I have stated above). I guess Nigeria is the only subsidiary where Nestle reports 15%+ NPM.

About past not being a good predictor for the future, I am sure this time its different ![]()

Cheers mate!

This is due to company pursuing aggressive volume strategy as they have reiterated .so past may not offer the right prediction and no one knows future but one must take into account change in stance by company while predicting

Operating leverage is not necessarily only into auto , machine heavy industries etc But wherever variable cost as a percentage of total cost is low . A business that generates sales with a high margin and low variable costs has high operating leverage irrespective of industry type.

Yes but depends on what one compares it with . If it compares it with matured peers like HUL ( which is how I would compare it as it occupies coffee can portion of my portfolio ) then it has greater growth and reinvestment while if one compares it with new multibaggers ( which ideally shouldn’t) , it will always lag (Of course theres a risk return difference too when one compares it with multibaggers )

Cheers

Disc- Invested and my views may be biased

How does higher volume growth translate into higher NPM? I guess you can say higher operating leverage which is probably why NPM is at a historically high number. But if we were to look at this business in 2030, would it be making NPM > 16%? If yes, why?

About Nestle not being a mature company, what are you talking about? They have 90%+ market share in baby food, 60%+ in instant pasta/maggi, 70%+ in condensed milk, etc. How fast are these segments growing? What is the growth rate that you are assuming over the next decade? Over the last 3-decades, they have grown their topline at 12-15% (in-line with growth in nominal GDP). Will this be different in the future, if yes why?