An analysis I did sometime back. Pasting it.

FMCG categories

Broad FMCG categories include Cigarette, Food and beverages, home and personal care, alcohol.

It can be categorized as

Nestle

Product Situation Analysis

New Vitamin D milk helps create additional margins to an already high margin product. Having chocolate as a portfolio, Nestle had not done enough to grow them over the years. They have lagged behind Cadburys and had not experimented with variants. However this seems to be changing in the last few years after Maggie was hit hard. Product diversification has been a focus after the maggie issue. Variants of Kitkat and Milybar have emerged.

Nanpro Excella has 30% higher price than Nanpro. Discounts are very rare for these products.

Introduction of breakfast cereal (Nestle NesPlus) has helped Nestle expand to a segment once dominated by Kellogs. We have seen that a developed market like USA has successfully accepted multiple brands in this segment. If we look at the general review of a product like this, it is clear that people compare it to Kellogs and finally buy Nestle for the sake of having a healthy breakfast. Hence the brand has been synonymous for health and nutrition.

Introduction of breakfast cereal (Nestle NesPlus) has helped Nestle expand to a segment once dominated by Kellogs. We have seen that a developed market like USA has successfully accepted multiple brands in this segment. If we look at the general review of a product like this, it is clear that people compare it to Kellogs and finally buy Nestle for the sake of having a healthy breakfast. Hence the brand has been synonymous for health and nutrition.

Nestle has also entered maternity nutrition segment which was new to a market like India. Thanks to GSK pharma and the Horlicks brand, there is enough awareness to stay healthy during maternity. Nestle Baby and Me maternal nutrition supplement has been quite successful.

Nestle Resource Opti is another high margin product that has capability to become a household name like Horlicks.

Premature babies have become common due to various lifestyle diseases that have cropped up in the current century. A product such as Nestle Pre Nan is currently imported and sold in India. With manufacturing in India, the margins must increase when Nestle has enough volumes to start domestic production.

Maggie masala range and the expansion of Maggie noodle ranges has been helping Nestle manage competition. The fortification of the brand ‘Maggie’ is paramount to Nestle and they have done well in the last 3 years.

Competitive Situation Analysis

ITC has been using the maggie debacle effectively. However ITC does not have pricing power as seen in their FMCG overall margins. The restoration of Maggie brand was seen in the last few years. ITC may be able to poach price sensitive consumers. However with Nestle matching price and being aggressive, they have ensured to keep Maggie a domestic brand as always. The sheer variants of Maggie makes it grab more shelf space and sales.

A new segment that Nestle is trying to expand to is the health food business that is dominated by players like Horlicks, Complan, etc. As we could see from GSK’s sales, it is clearly saturated and hence there is scope to crack this segment.

Nestle has presence in cereals market in Europe. However it was launched only in 2018 in India. It has been growing slowly and could be a major revenue source for Nestle. The brand has aggressively expanded the variants and has a very strong portfolio. Kellogs has been enjoying a dominant position for years and this could be changed with 2 to 3 additional players. The capex addition in Goa and Gujarat has been a classic indication of this trend for Nestle.

Economical Situation Analysis

The growth in India’s urban breakfast market seems to be on an uptrend. Kelloggs even reported that India and Korea led the Asia pack. It has been clocking double digit growth for over 5 years.

Technological situational Analysis

Modern production lines and economies of scale is needed for new product lines like cereals. Nestle’s parent has wide experience to achieve this due to their successful business in Europe.

Demographic situation analysis

While most products are focussed for urban dwellers, rural India could start embracing certain products such as baby food and maternity supplements. Children food and drinks could also follow this pattern. The cereal business may take time to penetrate rural India but the growth in urban cities has been very brisk if we look at the growth of Kelloggs.

Social and cultural situation analysis

The shift of consuming quick food such as Maggie and Cereals have been a wide spread trend for several years. This cultural trend is fast penetrating Tier 2 and 3 cities too. The new products such as Cereals could be on a multi decade growth trend, considering the addiction of sugar and lack of time for the modern family.

Political and legal situation analysis

Impact from Government, politics plays very little or no role unless it adds dietary restriction. There are no dramatic changes to accepted food standards in the last several decades. Low sugar and fat is usually the industry trend and Nestle is on the path to reduce them as needed.

Environmental situation analysis

Cereal market:

How big is the market? If Kellogg’s has a large market, it shows that the market is attractive for a new entrant like Nestle.

Kellogg’s has a big chunk of the market. How will Nestle launch new products? Will they attack them with a competing product or can they launch a unique product like they did in Europe? It has been shown that Kellogg’s was not able to counter a unique product very easily. Is there one such product with Nestle Cereals?

Is there a risk of substitutes? Breakfast bars?

No impact from Government. Hence this makes the business run without surprises.

When competing with Kelloggs, How can Nestle get economies of scale?

Gaining market using a large chain like D-Mart may be helpful. Have they done that? For example, Parle has exclusive deal with D-Mart to drive sales using the discount model. Ecommerce entry through Amazon has been initiated.

How will people change from eating traditional breakfast to start consuming cereals? Is there an urban influence to eat breakfast with minimal effort and fuss? Kelloggs in 2017 reported that their growth in Cereals was led by India and Korea.

Supply chain situation analysis

FMCG thrives on a good SCM. Nestle has shown to expand very well within urban areas with their efficient distribution. How they can emulate HUL to enter rural areas need to be closely watched.

SWOT

Strength:

Promoting brands takes a lot of time. Even difficult is to set up distribution. Setting up rural distribution network is an ongoing process. Pricing power is iminent for baby products.

Weakness:

The weakness of Nestle was exposed in 2015 when Maggie was termed to contain lead. The negative publicity was a blow as the product mix of Nestle was very much dependent on Maggie. The branding strategies seems to be poor in terms of naming brands. Nesplus, for example seems to be not a catchy brand name for an important product series. When it was tested with brand recall, it fared very badly. The quality of creating brands has been very well executed by ITC and Nestle may need to take some cues from them.

Opportunities:

Ceregrow, a new product with higher margin was added nationwide in 2017. Nan pro and cerelac are already leading brands owned by Nestle. The young indians like to pay more for products claimed as healthy. Nestle has been using this card for a long time and has utilized it successfully. However with the negative perception of Maggie, Nestle saw a stagnation in sales. This negative perception is temporary as these events vanish from public discussion in a short period of few years. We have seen that in the sales chart and growth rates as shown below.

The aspiration to consume baby products has been increasing in rural india. Over 70% of India’s population is in rural India and they have very limited exposure to FMCG even with the wide distribution. However finding a Nestle UHT milk or Maggie noodles is now possible in most Tier 2 and 3 cities. The apparent perception of Nestle taking a beating is only temporary as we have seen similar stories get buried for other products. Dairy milk is a classic example to illustrate the case.

Looking at market size is very important to understand the future growth. The annual revenue of Nestle India is Rs. 10,000 crores ($1359 million). Parent has a revenue of 8979 crores CHF ($89612 million). This is 1.5% of Nestle SA ‘ revenue. India has 17% of world population and the product mix of Nestle is in small price segments. This clearly shows that the saturation point is very far away. Nestle is one of the best way to play the population game and exploit the growth rate in population and disposable income.

Another way to look at consumption is to look at how it has changed in the past. According to HBR, the consumption became 13X between 1960 and 2012.

HBR - Indian incomes are growing at about the same rate, but from a much smaller starting base. And so what we would expect to see in India, which is still largely a rural country– a rural agrarian country– 70% of the population living on the farm. We would expect to see lifetime consumption increasing for the baby born in 1960 from $14,000 to $184,000, an increase of 13x.

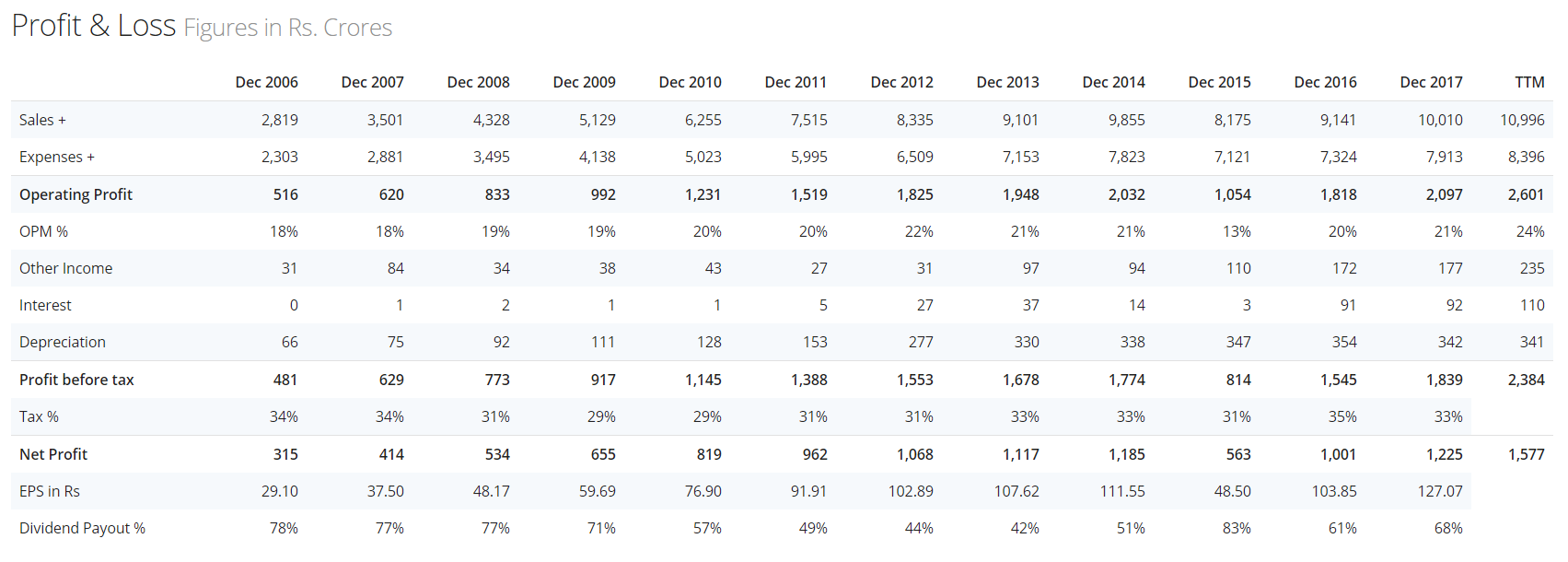

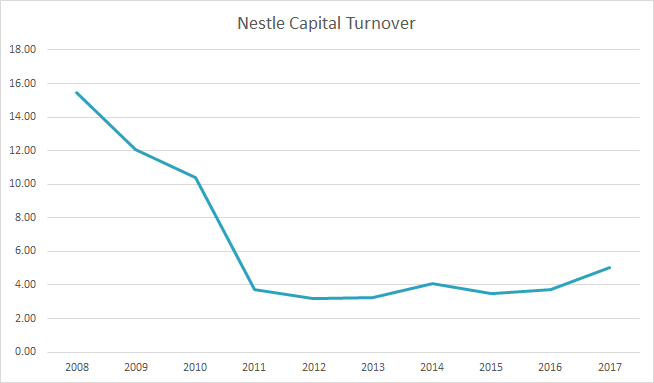

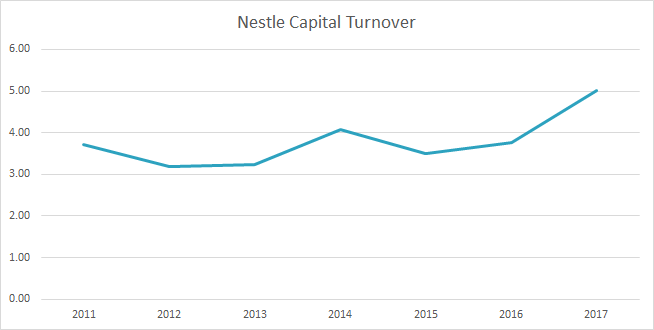

Nestle used to have a Net fixed asset turnover of 5 to 6 in past years. It declined to 2 to 3 in 2012 and has been recovering since. The OPM has been very stable at 20% over a long time. However sales growth has declined and there is a very good macro indication of improvement. The last 24 months of sales data shows recovery and it is possible to see sustained recovery and growth if the new product diversification strategy and brand strengthening exercise takes shape. The initial sales decline happened in 2015 after the issue with Maggie. Sales fell to 8k crores from sustained 9k crores in 2013 and 2014. The sales recovered to 10k Crore in 2017 and has been sustained at this level in 2018.

To understand the opportunity of the cereal products and their opportunity size, we can look at history. Kellogs was a common brand in the EU in 1990s. Nestle was new to this product line and entered in to a JV with General Mills (sold Cheerios in USA). This product line was an important revenue stream for Nestle even today. How they captured the market from Kellogs could be very useful to analyze the opportunity in India. Nestle never launched a predictable product to compete with Kellogs. Each market had a local taste and Nestle was efficient to target that. For example, Nestle never launched Corn flakes in Europe. They also used their strength in other business by launching Nesquik cereal to mirror their Nesquik drink. Kellogs had no such drink and was unable to compete with Nestle.

Threat:

Maggie issue in 2015 was an important event which has changed how the company operates. The product mix is now updated to decentralize brands.

The net fixed asset turns have been improving in the last few years (even though reporting standard changes have made it difficult to compare).

Threat from suppliers : Suppliers don’t have bargaining power. Hence the threat is very minimal due to raw material pricing.

Threat from house brands: High risk for generic products and weak product lines. Example: Cornflakes could be a weak link while a granola caramel crackle could be relatively safer.

Issues analysis

The issue of branding cereal has to be addressed with proper commercials and distribution. Baby food has been a prime revenue generator with higher margins. However the seamless graduation from Nan Pro to Cerelac, and then to Ceregrow has not been executed very well. The use of careful branding would have prevented this issue. We need to see how Nestle could make an infant start moving from Nan Pro to Ceregrow when they age.

References

Nestle:

- Nestle AR - https://www.nestle.in/investors/stockandfinancials/documents/annual_report/nestle-india-annual-report-2017.pdf

- HBR - India growth - https://hbr.org/2012/09/china-and-india-are-an-opportu

- Nestle Cereal growth in EU - https://www.uhu.es/45122/temas/P&SC/BreakfastCerealMarket_ATTACKvsDEFENSE_P&SC.pdf

Disclosure: Adding it to my core portfolio.