The stock price reflects double digit growth in the future. If that does not happen, the valuation is not justified. They were pushed back due to Maggi issue. So we should see them catch up sooner or later. But how much growth they can do in the next 10 years will decide the price. They are certainly doing a lot of things but we should see the results only after a few years. Management is not the best but have been forced to work hard after 2016.

I suppose, a stock is a good investment when the setup is inverse of what Nestle offers right now.

Stock of Nestle is, currently, demanding a very high price for a future prospect, which is still speculative;

A good investment is one in which growth is already visible, but the stock price is beaten down due to exodus of liquidity due to global reasons. Or a generally gloomy sentiment. Or simply due to a temporary setback in the company, like the maggi issue.

It can be a good investment if we are certain that the bottom line will keep growing at above 10% cagr with a few abnormal growth from new product lines. It will be speculation if we don’t have any hard data points to back it up.

In a way Nestle is in this kind of situation. The earnings and revenue has been hit due to Maggi issue and Nestle needs time to recover. If we value the company based on past metrics (which includes lost opportunity from 2015), valuation will be depressed.

Nevertheless it does not appear cheap looking at the past and near future unless a product line (like cereals or Nan grow or a new product like cereals) picks up big time or distribution becomes better and economy has better buying power!

I want to draw your attention towards the euphoria that we are in. If it were normal market, Nestle wouldn’t command PE 60 with 7% cagr sales. It is not just Nestle;

Marico 3 year sales growth, is an astonishing 3% and the stock is commanding a PE of 50 !

Emami 3 years sales growth, is 4% … again PE 60

Dabur is even better, 3 yr sales growth is a minor negative… but people are willing to pay a PE of 50

and the Ace of the deck: HuL, 3 years sales growth 4%… commands a massive PE of 60.

This, I feel, is money talking. The fund managers are flush with cash, and good companies are few and far-between. Only when the tides ebbs away, we will see the reality.

A value investor shouldn’t have to pay-up first, and then hope for the stocks fundamentals to catch up. It should be the other way around.

Unless, the sector is totally in ones circle of competence, and one is fully in touch with the sector-beat. Else, it is just not value investing… probably hope-investing or speculation at best.

4 Likes

This company falls under the circle of competence for more people than an oil rig company or insecticide company. So we do have an edge if we try to look at the reality without prejudice.

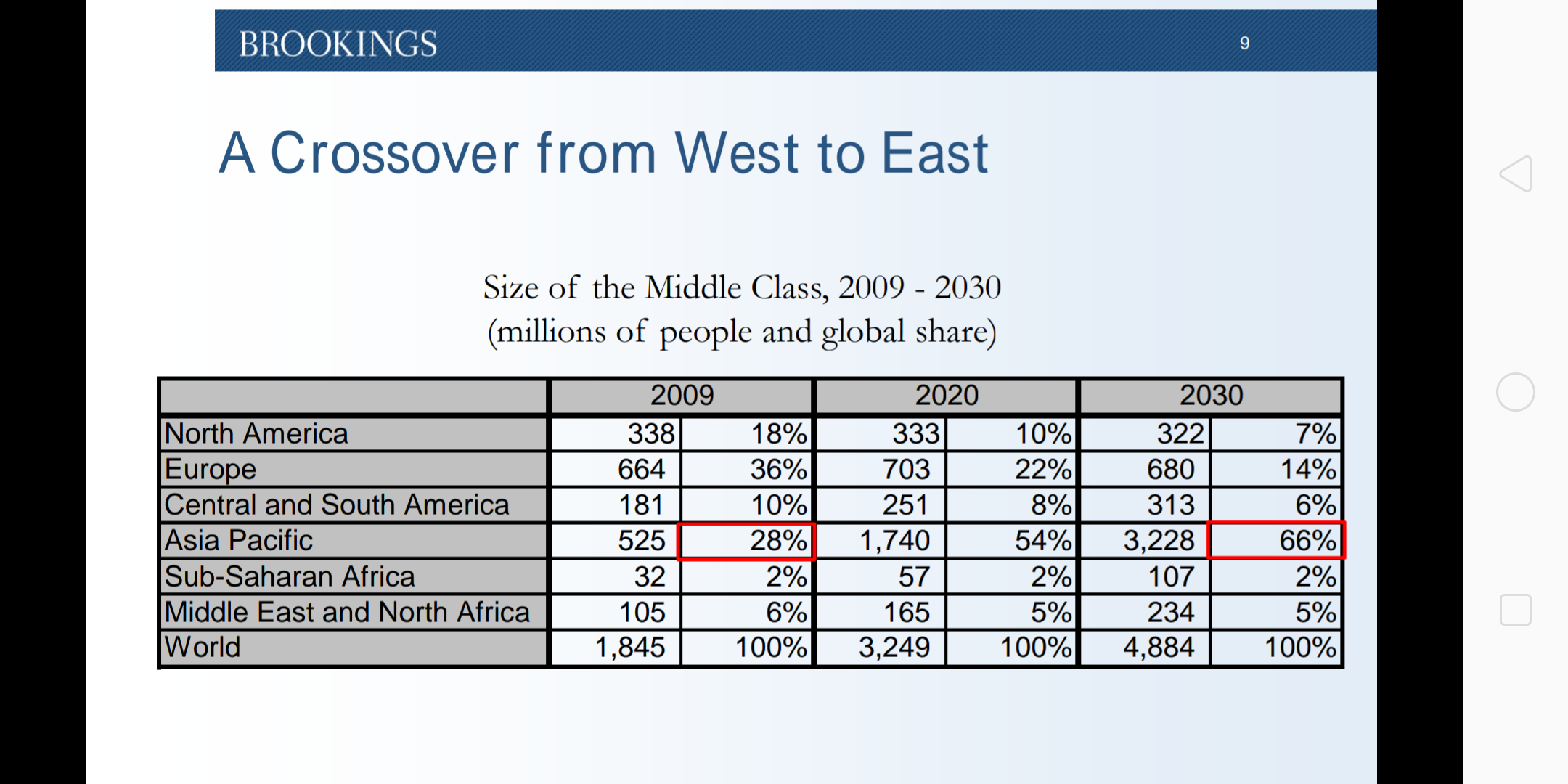

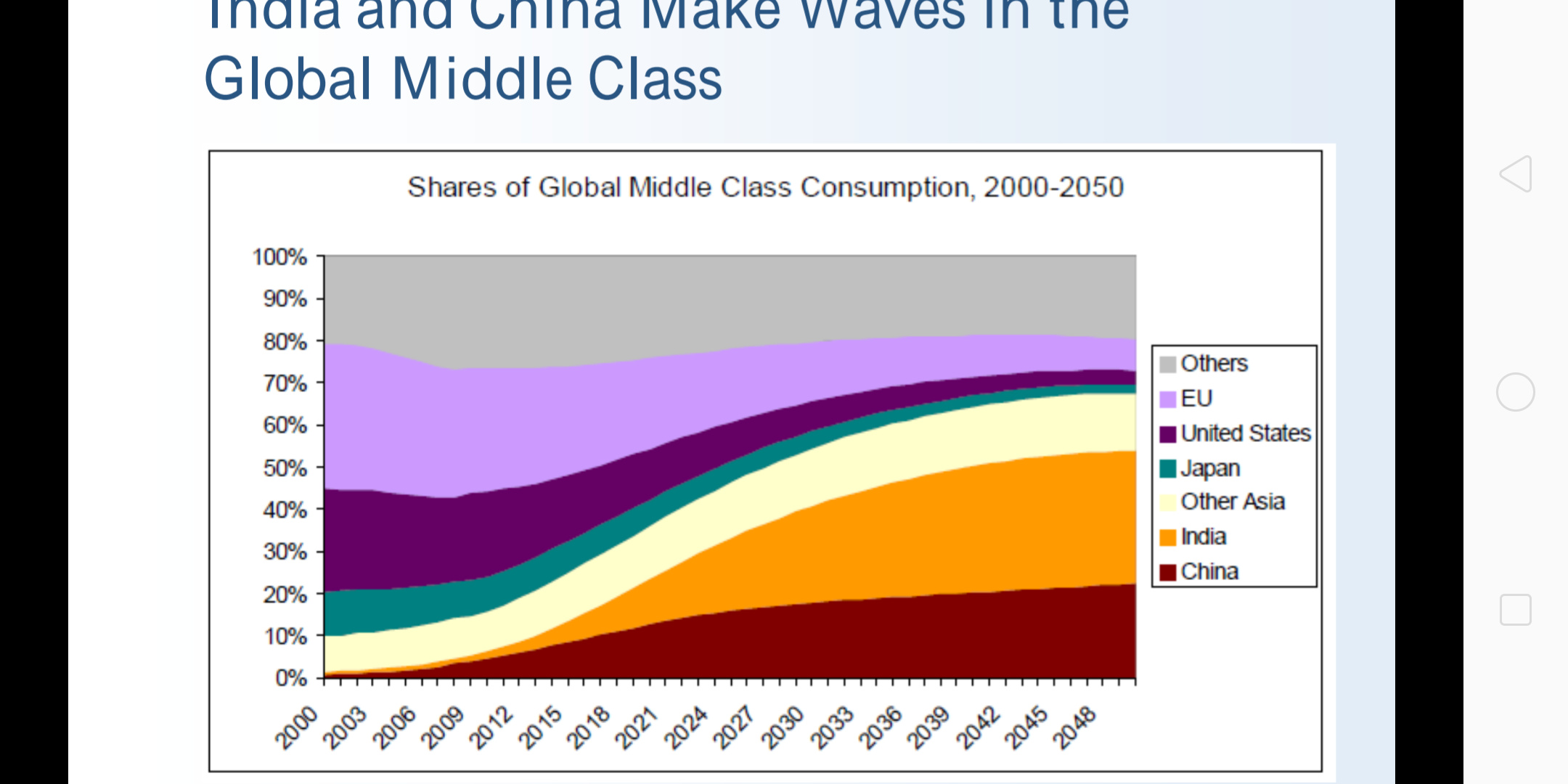

The market size is huge and Nestle occupies a very small footprint now. Indians are unable to afford most of these products although they have an aspiration to buy them. The rise of Indian middle class depends on multiple data points and one can get an idea from proxies. The saturation point is at least close to 10x current revenue.

So once we decide that the company is a good candidate for buying, we need to wait for the right price. It is impossible to buy a company as soon as we decide to buy. We need patience. I remember that Nestle grew at 18% or so between 2008 and 2012. That growth was temporary and it was followed by issues in 2015. During this period , the Indian middle class story has not changed. The population growth has also not changed.

Personally I prefer to wait to buy a good company. I am okay to spend 5 years to buy when I plan to hold it for more than a decade. For a company like Nestle where it is difficult to predict the growth rate in the short term, I prefer to buy at every dip in valuation (sometimes valuation may dip but prices may go up due to faster earnings growth). I usually have 5 to 10 tranches spread across a period of 5 to 10 years.

What is changing at Nestle?

- products like Nan Pro can become affordable for more consumers in the next decade.

- a product like Nan grow (launched after the success of Nan Pro in Indian market) has a longer lifecycle of 4 years compared to a 6 month lifecycle of Nan Pro.

- Cereals has been a fast growing segment if we look at the balance sheet of Kellogg’s india. We can expect the same for Nestle if it clicks.

- Cerelac and Lactogen as well as Ceregrow can take care of the price conscious segment of India. This helps to fill every bucket of affordability.

- Lazy management seems to be realizing the potential. We can see if they are ready to launch good products which have scope to work in India. Take the pink kit Kat as an example. It is a wonderful hit in Asia but we still don’t have it in India. The taste is really good in my opinion ( at least is very different taste) and I am not sure why it is absent here. There are many such products in the parent portfolio that can be Introduced here.

6 Likes

You have raised a very good point. PE ratio is only an approximation which makes sense when comparing similar business, but they have no relevance in absolute sense and claiming a business as expensive just because it trades at a PE of 60 would be wrong. The stock price is the discounted sum of all future cash flows, and so estimating the opportunity size and probability of that being realised is a better approach than trying to guess the right earning multiple.

Can you provide the basis for the saturation point estimate? How did you arrive at a 10x figure?

2 Likes

These data points are very high level. Hence one can add multiple layers of safety margin. Indian middle class (consumers who could afford Nestle products) are only about 3% of total population. The growth of middle class is around 4% cagr in the past and has been accelerated in the recent times. This 40 million middle class is expected to become 400 million at some point of time in the near future (may be 10 to 20 years). That means Nestle gets at the least 10x more consumer base. The importance of a product like Nan Pro ensures that margins will be stable. We have seen Nestle protect 20% margins for a very long time. We need to remember that even at 400 million middle class population, we may not reach saturation. That is why I said at least 10x.

Reference:

Parallel-Sesssion-6-Homi-Kharas.pdf (380.9 KB)

http://siteresources.worldbank.org/EXTABCDE/Resources/7455676-1292528456380/7626791-1303141641402/7878676-1306699356046/Parallel-Sesssion-6-Homi-Kharas.pdf

6 Likes

If increasing Middle Class in India be taken as a theme for investment, then lets see what markets could expand.

- Real Estate: They are likely to make homes in the cities and suburbs. So, real estate will get dearer, but this is not an asset light so not sure about RoE. Paints and Interior businesses (Cera, Kajaria…) are better.

- Home Loans, Banking, AMC, Insurance for the middle class to manage funds.

- Automobiles… Maruti, M&M, Tata Motors, Hero Honda, Baja Auto. A car for each home.

- FMCG too. The eternal consumption story.

- The middle class is a health conscious people. Cannot afford expensive medical bills, hence Cigarettes may not see strong growth like FMCG products. But, spirits are in.

- Pharma: Instead of large entities that depend on exports, which appears to be a fickle business, one could look for Pharma Cos that serve the cities like… Eris Lifesciences. Not so sure about Asset Heavy hospitals showing strong growth.

So, have we covered Roti, Kapda and Makan? I hv little faith in the textile companies.

1 Like

When middle class increases in size, remember that the pie could be shared by many players. For Nestle, risk is less in segments like baby foods where people prefer Nestle over unknown brands.

1 Like

Yes, there may be several ways to play on the expanding middle class opportunity. But we should keep in mind the risks associated with each business, some of these risks prevent them from taking advantage of this opportunity.

Since this thread is about Nestle, I will try to list the risk faced by FMCG.

While progress will lead to rise of middle class, it will also ease availability of finance and costs of starting new business. Therefore the competitive intensity will rise, and the larger pie of revenue will be shared among larger number of market participants. Therefore, while opportunity size is important, it is also necessary that we pick business with sustainable competitive advantages.

Now for an FMCG, competitive advantage has two sources - brands and distribution strength. Setting up a strong distribution network is costly, however as more sales are channeled through e-commerce and retail chains like Dmart, the advantages of having distribution network will weaken. So the only moat that will be left is brands, but I am not sure how much value brand power commands in FMCG. For example, I will not pay a significant premium for Maggi, as opposed to any other (well-advertised) brand. If the moats enjoyed by FMCG companies like Nestle, HUL were to weaken then they may not be right choice at current valuations.

Lastly, we should acknowledge the risk to rise of middle class projection. Future can be surprisingly different from the linear extension of past. Case in point - people expected Japan to overtake US by 2000, and China to overtake US by 2020, but these projections miss the importance of continued reform in order for them to be realised. Alas, necessary reforms are not undertaken if the government has an easy way out, which would be the case in good times.

3 Likes

I also want to draw your attention to the fact that HUL when languishing at 200 RS for almost a decade was still at 50 or more PE…it was never cheap even at 200 RS. Having said that I am not sure about future but people buying hul at 60pe must be betting on ponds, Horlicks and numerous brands which they feel have long way to grow and ethical management to take care of that with no need of loans and arbitrage or dealing with people who may or may not pay back or hugely dependent on interest rates or crude prices or dollar value etc.

Right. The time-tested fmcg companies command a high PE in bear and bull markets alike. I looked up Nestle and HuL.

Nestle is pretty much bear proof, and bull proof too. Its EPS has grown steadily at 10% in the past decade.

It makes even more sense to see why @Uservijay buys Nestle at corrections.

Nestle is cheapest quality FMCG if one has long enough investment horizon.

It’s not the 10% steady growth that interests me. There are times when it had grown at 15 to 20% cagr. In the year 2000 I am sure we would not be sure of Nestle surviving for 2 decades and earning 10x or 15x bottom line. Nestle India makes just 1600 crores today. If we buy it for a little expensive valuation, we may lose opportunity cost for a few years. But if we are certain that Nestle can do 16k crores bottom line, and still have the slow 10% average growth, it will be invaluable. PE is a metric to understand payback period. In business school we have done many experiments to show that NPV is far superior to payback period. But it still makes sense to look at payback period to make sure we keep it within a meaningful period. However if we use payback period to value an asset, things can get ugly and we may miss out on good opportunities.

To understand how valuation can look cheap (or expensive) in retrospect, let’s go back to 2009. Maggi noodles was picking up and was growing at 25% cagr. This segment was only 20% of revenue. We know how this segment grew until 2015. Similarly if new products lines like say cereals pick up, we might end up seeing substantial growth over the years. At least the 2015 issue has helped them to understand risk and diversify/launch new products. Bottom line, one must visualize how good the company is today after all the learnings and also understand the opportunity size. The willingness of the management to use the opportunity size is vital. We can see that only if we wait and watch.

One can buy Nestle if

- we expect few products to really grow double digits and push sales for at least few years

- consistent growth and steady margins

- Large opportunity size of say 10x or 15x.

- Management willingness to bring products from parent portfolio.

- Management getting better when India subsidiary becomes bigger for the parent

- No black swan event that can bring down revenue loss for extended periods.

6 Likes

I wanted to add a few cents about how FMCG brands are created.

A new product needs time to be absorbed. It is habit forming exercise and it takes time. The Maggi brand was launched in 1983 and it made a loss until 1993. Effectively PE is negative if we look at it from shareholder point of view (as payback period). But NPV was expected to be positive and today we know how the cash flow is from Maggi. Between 1993 and 2001, it grew 7 times bottom line and then to become 30% of total profit of Nestle India in 2015. The Maggi brand was actually soup and dehydrated products from Swiss italian inventor. Later when they wanted to launch in India, they asked help from Malaysia and came up with some options. The folks in India refined it and made it spicy to appeal to Indians and Maggi was finally born in 1983. So a product can be successful only if it was adopted to local market. We saw that when cereals was launched in Europe by using Nesquik as a template to counter Kellogg’s. Although General Mills helped Nestle, it was local team at Nestle that used their experience in Nesquik to make a successful cereal product.

The Maggi issue has forced Nestle SA to have a dedicated management in India. Before 2015, for example, Suresh N (MD of Nestle India) was actually serving in Philippines and India was expected to function with mid level management. After the 2015 Maggi issue, a senior management is kept in India and I hope better quality management decisions are made after 2015. Even today the quality of management is sub par at Nestle India as seniority is the ticket to career advancement, just like a public sector or Government job. Imagine a CEO like Varun Berry at Nestle with support from global portfolio!

Nevertheless the Maggi disaster helped Nestle get all the attention and the global management forced the India management to launch 40+ products in a quick 3 year period. Nestle after decades of existence had only 20 odd products until 2015. Maggi hot spots or franchise was setup to use organized dining. Online sales using snap deal and then Amazon was set up. All these efforts will bear fruit only after 5 to 10 years. By then we will know if PE was the best metric to look at Nestle.

6 Likes

ITC is transforming into diversified portfolio with inroads to village platform access. Future consumer trying farm to market in multi channel mode. Organised retailing getting corporatized will increase bargaining power of big format retails. Nestle has created big sustainable brands but with distribution channel getting more concenterated and heightened competition will have its own challenges to keep growing unabadetly. Export market will be key to all and a differentiator.

Neither ITC nor Future consumer will be trusted for baby foods. It takes time and effort to get a mother trust a brand for their baby.

3 Likes

Do you mean, the next leg of growth for Nestle will come mainly from Baby Foods. Does the company envisage becoming a leader in this space?

This is a sensitive product, where brand premiumization has scope. But, how big is this market? And how much success the company has got this far?

Yes. It is the most under penetrated segment. There are other related segments such as Nan grow and Nesplus cereals which are not specific to babies.

The market size is in infancy now. A product like cereal is addictive and people don’t change the brand once they get used to it. Personally I have tried many brands but always stick to honey bunches of oat. It takes time to make people addicted to a product as I had explained in my previous post.

It is the market leader in baby foods with Nan Pro (premium segment) and Cerelac.

The cereal product line is new and is already 2% of sales. It is expected to go to 5% of sales.

2 Likes

Also the ads on baby food is banned, so it is tougher for competitor to build a new brand and replace the existing leader.

3 Likes