Neither happy nor disappointed with results.

Margins of BEC have dragged overall dont know it gonna be regular from here or BEC Margins go back to pre Covid levels.

BEC revenue also decreased…

They never compromised on margins even during tough times.

where did the money go ?

Nation wants to know

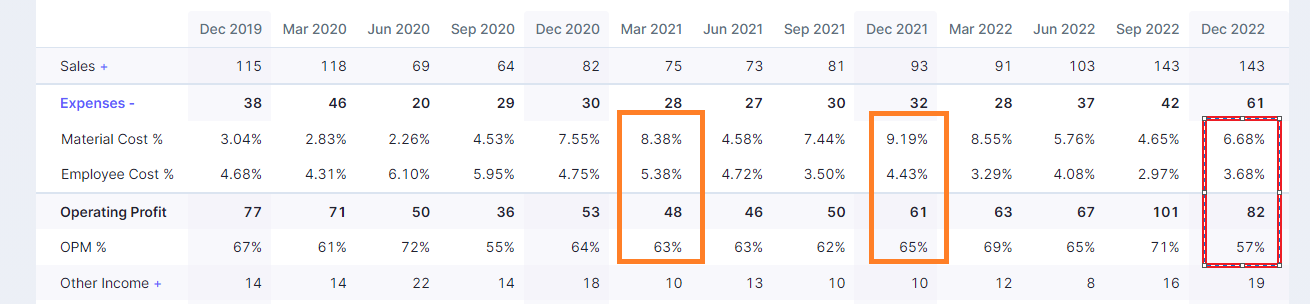

Other expenses 16cr more than last quarter…

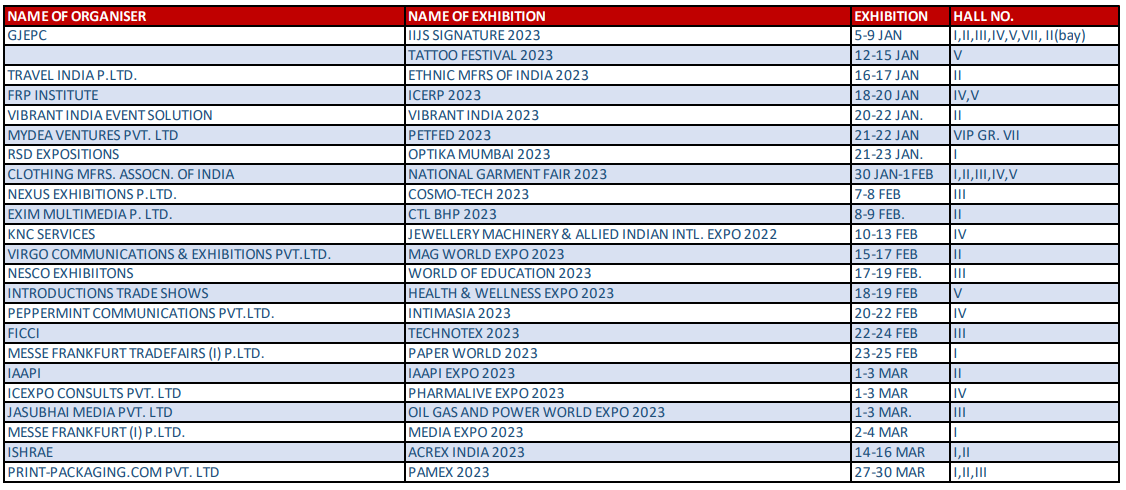

BEC revenue down…Other expenses on higher side…seems they must have done renovation/repair…

As suggested by Krishna, higher other expenses is due to demolishment of one factory shed to build a new exhibition Hall #6. This has resulted in a one-time cost of 15 cr. Adjusted for that, profitability is in-line with last quarter. Its not related to management commission.

And reason for lower exhibition revenues (vs Q2FY23) is a few large-sized exhibitions were held in Q2FY23, vs a number of small to mid size exhibitions in Q3FY23. They are expecting recovery in 4QFY23.

Disclosure: Invested (position size here, no transactions in last-30 days)

Thank you…Where did you get this information?

Nirmal Bang covers Nesco very well, all the shared excerpts are from their report.

Even after decent set of Q3 numbers and expected EBITDA of 400 cr with a net profit of about 300-330 cr in FY24, why the stock trades at 13 P/E and 7 EV/EBITDA (cash = 1000cr which is 25% of mkt cap)? It looks ridiculously undervalued for this kind of stable business.The revenue/profit has not been dependent on economic conditions if one look at the historic financial statements except in FY21 and FY22 covid impact which i assume is not going to repeat. Any idea why so much pessimism in this stock which deserves 16-20 EV/EBITDA ? Is high Promoter holding of 68% and low FII holding of only 2% a reason for lack of price discovery?

Market doesn’t see much growth from here as whole biz is tied to a piece of property. They need to bump-up dividend payout significantly to signal regular solid cashflows.

2-3 thngs happening\abt to happen here :-

1.) Recovery in exhibitn biz vl add to good earnings growth over current base. Generally earnings growth follows multiple re-rating

2.) Single location though a risk, still has ample area to be developed over long run which will provide stable earnings stream. The negligible cost of land on thr balance sheet vl continue to be a source of thr moat esp. in high interest rate environment

3.) The cash balances provide them opportunity to do capex thru internal accruals thus creating a strong earnings stream. Nd they can always buy another land parcel smtime in future and develop, so don’t see any harm in holding up the cash balances for optionalities

The mkts. have given crazy multiples to unstable biz models too in near past and compared to that this stable biz definitely warrants good valuation. So let’s see whn the voting machine market swings to weighing machine in this case.

Disclosure :- Invested.

Inflation = Rental growth takes care of nominal growth of 6-7%. Available land bank (i guess 20-30 acres) and cash will ensure business growth of additional 4-6%. So 10% growth in topline is almost guaranteed unless management becomes very lethargic and bottomline could be 10-15% depending on again management’s effort.

This growth should persist for next 10 yrs and saturation comes after 10 yrs. For 10% EPS growth, 13 PE is too less. But even after 10 yrs, i suppose inflation equivalent growth is sufficient to keep the stock at 16 PE in FY35 as it is a risk-free business. so right now it must trade at 20-25 PE.

If cash is reinvested for new construction, then investors need not worry but if it is in the book like now and cash to equity exceeds 40% (right now 50%) and payout is <25%, then PE will get hammered.

Traffic in this location is another issue which can inhibit growth but i dont think this land will be left unused in a city like Mumbai.

Whatever it is if management share the earnings with minority shareholders, then NESCO is a stock to hold for next decade.

Question should be what would be terminal PE when growth stops. Market has answer. Look at Elnet, IT tech park. Forward PE < 5. Infact EPS is very similar to Nesco

So, if in 10 years EPS becomes 3x and current perception of market is <5 PE, stock if already fairly valued.

Biggest segment of biz is IT park. Now why should be IT park biz command a higher PE than IT companies (on grand scale IT park biz is a function of IT companies biz) which have historically traded at 15PE and have shown about 10% growth and is much higher RoE and capital light biz.

This is a very incorrect comparison, profit growth looks higher in Elnet due to higher other income. Core business has hardly grown, 10-year growth in sales are at 3% and EBITDA at 6%.

And why are you penalizing Nesco for 2 years of pandemic when they were not allowed to operate? Look at FY11-20 growth (and not FY12-22) nos for exhibition business separately, and then do the extrapolation.

Elnet is trading at 5 PE because it does not pay dividend and cash = Equity . Also Elnet is owned by state govt too and hence growth is only 3% due to poor management team. Elnet does not even own that land but leased one. Elnet have no land bank and existing space is fully occupied. Hence no growth but only 3% inflation dependent rental growth which is also mismanaged whereas NESCO has grown at 10% last decade and will continue for another 10 yr.

Instead of considering the likes of HCL Tech and Wipro, if one consider entire IT sector, then historic PE is 20 as Infy, TCS, LTI trades at 23 on avg. Also, they are renting not only to these big companies but many other unlisted companies and foreign companies whose growth or valuation is higher. Anyway, i dont have this point of view to equate IT sector’s growth to NESCO. When IT was growing at 100% YoY between 1995-2000, no renting space was growing at that rate. If IT sector degrow and another new economy sector like renewable energy sector starts growing at abnormal rates, then the space will be rented to them and IT parks will be renamed as Renewable park. Thats why this business is much more stable but with nominal growth than any specific sector.

Nominal growth and higher RoE can be acheived if cash is taken out of the book. Dividend is what matters going forward.

More power to nesco to charge premium .

Also preferred choice for Corporates and employees.

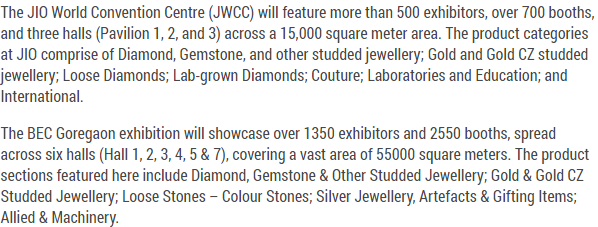

Interesting that hall 6 is out of action. Says its being dismantled? Does anyone have any more details about this?

Hall 4 is where the next phase of the IT park is due to be constructed afaik. So that expansion unlikely to happen anytime soon if they are renting it out to exhibitors.

The management seem to be only capable of executing one project at a time. And sometimes taking a few years holiday between finishing one and starting another. Then they mess around and don’t avail of the huge fsi discount that was on offer in 2020/21 which was a few 100s crs. And so on.

You cant fault them. They are already rich. They seem to be happy with lumpy growth once every 7 years or so. They don’t seem to be too bothered if they reach full developmental potential in 15 years or if it takes 30 years.

There will be one year of growth as bec rev normalises to the pre covid trend. But after that expect about 5 lean years. The underlying rev growth of existing assets is about 5pcpa.

Came up with decent set of numbers. QoQ ~20% eps growth.

Dividend 4.50 per share

https://www.bseindia.com/xml-data/corpfiling/AttachLive/d54e0a54-12d2-491f-ac73-3cc9f06320cf.pdf