Company update regarding electrolyte formulation capacity by HDFC Sec

7 Likes

Ever since started to learn about the scope and potential of fluorine chemistry I had a question in mind about the future of Neogen. Fluorine mostly replaces bromine compounds in agro-chemical and pharmaceutical applications. Especially I tried to dig further deep into the minor and major issues faced (disaster) that happened due to the use of bromine compound in agrochemical space.

Now it seems to be a bit more clear that FLUORINE and BROMINE chemistry mostly do not compete with each other since the bromine compounds (products of NCL) are used during different manufacturing processes (as catalyst or so on so forth).

4 Likes

Fluorine only competes with bromine in few agrochemicals. Mostly Fluorine is replacing chlorine which is much more polluting.

Disc: invested in both fluorine and bromine players.

10 Likes

Fair set of numbers.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/26df3576-06c8-455e-ac34-2693dc2b8530.pdf

Doesn’t it seems overvalued now with trading at close to 100 PE now ?

In the hdfcsec report I could see a lot of highlight on ACC. Below news on Reliance looking for sodium-ion instead of lithium-ion for its giga factory makes me to think. I don’t have electrical background hence confused.

1 Like

watch this video. See what is the difference between Lithium and Sodium batteries

1 Like

Thanks for the useful video on issues related to sourcing of lithium, but I could not see any comparison between Lithium and Sodium batteries.

Explainer on Why lithium is here to stay and both sodium and lithium will coexist in future.

1 Like

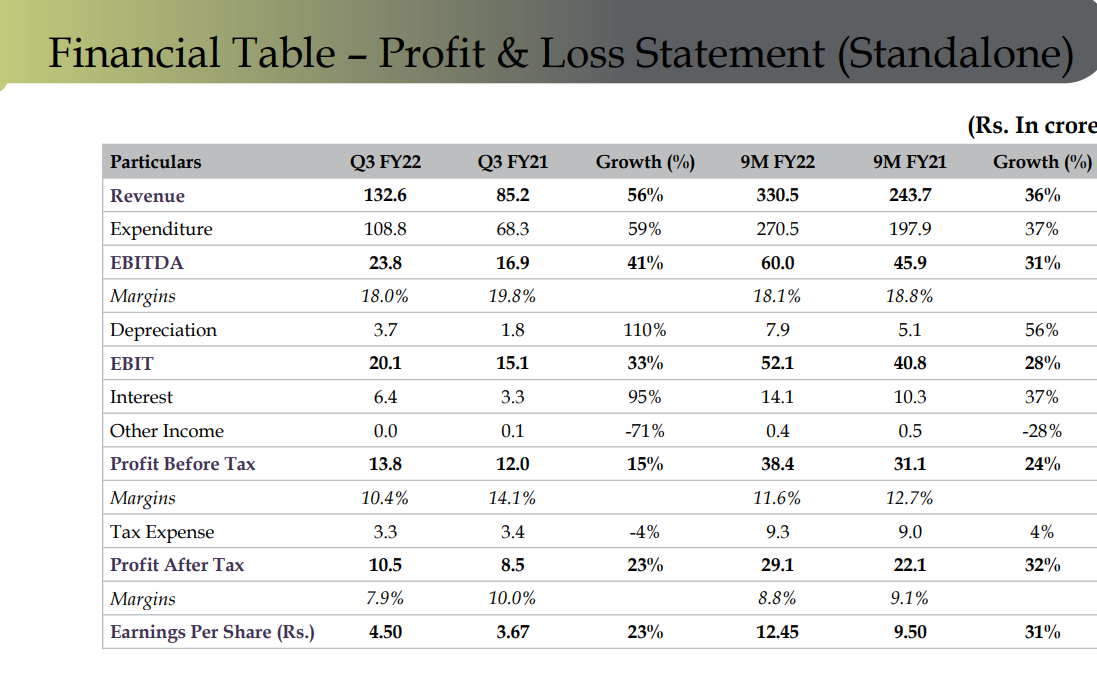

Neogen revenues in Q3 FY22 increased by 56% to Rs. 132.6 crore, as compared to Rs. 85.2 crore in the corresponding quarter last year. The strong performance was driven by higher contribution from the recently commissioned phase I & II expansions at Neogen’s Dahej site. Both demand and realisation stood favourable, led by higher product off-take across key end user industries.

Profit after tax (PAT) stood at Rs. 10.5 crore during the quarter as compared to Rs. 8.5 crore

in Q3 FY21. PAT growth was muted due to higher finance costs and depreciation, in-line with

new capacities added during the year. This will improve once the new plants operate at

optimal utilisation levels.

Raised Rs. 225 crore equity on preferential allotment basis to support our growth initiatives in advanced intermediates, custom synthesis and contract manufacturing, and lithium-ion battery materials space.

The idea is to be future ready and gain first mover advantage in some of these high potential

opportunities, while retaining our balance sheet strength. Post commercialisation of Phase I&II projects, we are now running our Mahape and Vadodara plants at high utilisation levels, while Dahej SEZ plant isramping up. As envisaged, we are now focusing on niche and value-added productsthat require expertise in complex chemistries with multi-stage processes. Our pilot plant initiative of electrolyte manufacturing for lithium-Ion batteries is progressing well and we remain on track to commission that by H1 of FY23. All these initiatives will significantly improve our revenue trajectory over the next few years.

The road ahead appears equally exciting for us, and we remain vigilant of growing opportunities in the chemicals and lithium-ion battery materials for EV (electric vehicles) space. We will continue to use our expertise and capabilities to deliver sustainable and profitable performance.”

8 Likes

Outlook

-

Raised its FY22 revenue guidance to Rs4.5bn-4.75bn, considering its 9M FY22 performance

-

Maintaining its FY24 revenue guidance of Rs7.25bn. It would revise this, after finalising capex, depending on the commissioning.

2 Likes

Initiating coverage report by Nirmal Bang

4 Likes

Couple of Observations

a. The audit fees are increasing heavily over the last few years. Below is the extract from past few years ARs. Will need to see audit fees for FY22 when AR gets published.

Audit fees- 2018- 4 Lakh, 2019- 5Lakh, 2020- 8Lakh, 2021- 22Lakh

b. CFO to PAT conversion from 2011 onwards for standalone entity

| Year | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | Total |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| PAT | 2 | 3 | 4 | 4 | 5 | 5 | 8 | 11 | 21 | 29 | 31 | 45 | 168 |

| CFO | 0 | 0 | 0 | 3 | 9 | 9 | 0 | 12 | -4 | -34 | 83 | 1 | 79 |

c. Approx 60 percent amount is in inventories and trade receivables e.g. for FY22 Trade Receivables-195Cr and Inventories-110Cr

Would like to seek views from fellow members on the above.

6 Likes

Its been a challenge for the company to deliver both very high growth and high cash flows, owing to challenges around inventory build-up… In the year when growth was lower, had delivered significant cash accrual.

Pursuing high growth - They have over achieved on the guidance given on capacity 3 years back. During IPO in 2019, had guided that in FY24, capacity would be Rs. 500 crore. Today, capacity has increased to almost 750 crore and looking to add further. The year in which the growth was minimal, delivered cash-accrual significantly. Not been able to deliver both very high growth and cash flows.

Certain molecules saw an inventory build up owing to lower demand last year. But still the company grew and made up, through other molecules. Inventory likely to get better rationalized once Dahej hits full capacity in FY 24.

1 Like

Notes from the Q4 call

-

FY22 full year revenue at 487 Crore; had given guidance of 450 Cr. Confident of achieving the targeted revenue of Rs. 725-750 crore in FY24

-

Got approval from Board for an estimated capital expenditure of upto Rs. 150 crore, to be deployed in FY23 at Dahej SEZ Plant for:

• Expanding manufacturing capacity of specialty organic chemicals by 60,000 litres – to support new molecules developed in-house and enhancing ability to do multiple chemistries

• Increasing capacity for manufacturing inorganic salts from 1200 MT to 2400 MT in existing Inorganic MPP – this is to cater to demand from new approvals received from international customers for regular lithium-based products recently and expected growth in their demand in domestic market

• Setting up new capacity in existing Inorganic MPP for 400 MTPA for manufacturing Specialty Lithium Salts and additives for Electrolyte

• Overall site development in Dahej -

Brownfield expansions are expected to be completed by June 2023 and will result into incremental revenue potential of Rs. 250-300 crore per annum post commissioning. Expected to reach full utilisation levels by FY25 or FY26.

-

Incremental potential revenues from Inorganic Chemicals (150 Cr) are based on stable lithium prices. Current market prices in Lithium, are 2.5-3 times of what was the world’s highest price in the last - historic peak. Prices likely to start moderating in the CY 2023.

-

Most of the price increase has been passed on to customers. Many other people who are buying from other companies or from China, are suffering, because their suppliers are not in as good a position in securing lithium as Neogen has been. Customers are appreciative that Neogen has bene able to source Lithium for them.

-

In last 3 to 4 months, has added 20 new customers and out of that, 5-6 new customers have also approved Neogen products and have started buying products from Neogen in the international market. Customers based in US, Europe, China, Japan and Korea.

-

Neogen’s Dahej lithium site started in Feb 2020, post which there were travel restrictions due to Covid. Now, customers feeling more comfortable to travel, had several of lithium customers who came to the site, approved and now have started procuring lithium molecules from Neogen.

-

Capex on electrolyte business - For inorganic business - asset turns are usually better and the margins are usually slightly lower. However have to wait and watch as current investments are trial investments. Will have a better idea on margin profile & ROI with 1,000 MT kind of production capacity.

-

CSM business –

a. By FY24, advanced intermediates will contribute 40% and the CSM will contribute up to 20% revenue of that

b. Made 18-20 molecules last year, which were readied for commercialization, they have completed the pilot work and completed R&D.

c. There are multiple segments which the CSM molecules are catering to – agro, pharma, one is in engineering segment and one in food & flavour segment -

Threat from Sodium ion batteries - Sodium ion is mostly used for energy storage applications. Lithium cells are driving EV applications. Most EV manufacturers and batteries will be Lithium based Even if Sodium ion were to happen, wont impact too much

Disc: Invested

6 Likes

What’s view of you guys on valuation as we have seen with other companies where one or two bad quarters and market has severely punished them. At current margin with 750 crore sales, PAT would be 80-85 crore so still trades at 40+ PE (2024 estimates) with taking that much growth into account. I am new to investing haven’t seen many cycles so if any senior can talk about their experience in such cases.

1 Like

Personally feel, given the inflationary trends, either they will significantly exceed revenues or the margins will expand (as inflation tapers). Every company is being conservative in guidance and basing it on “stable” prices. Under the stable price regime, companies also did better margins. One thing has to give.

3 Likes

Found a very interesting co listed in usa which seems to be in very similar space to neogen

Investor presentation: https://quartr-files.s3.eu-north-1.amazonaws.com/conference-calls/099e6-2022-08-04-08-51-32.pdf

This one is at roughly 20 time earnings. Need to see sustainability of growth though, I’m working on it.

5 Likes

We at Solidarity Investment Managers own a position in Neogen Chemicals. Attached PDF contains a detailed note on our views. Sharing our summary thesis below

Summary thesis

Promoters have demonstrated resilience. Their story inspires confidence and trust.

Neogen total addressable market is continuously expanding. Neogen was already strong in Bromine and Lithium based compounds, it commenced Advanced intermediates and CDMO business in 2018 and is now entering Salts and Electrolytes for Li-Ion EV Batteries.

We estimate domestic Electrolyte opportunity could be worth ~15000crs by FY 30 where Neogen is well positioned. Exports of Lithium Salts is an additional opportunity. China controls 95% of global supply at present.

Neogen has executed well growing Operating profits at ~27% CAGR in the last decade.

Promoter credibility, historical track record, and the opportunity to grow earnings at 25%+ CAGR for the next decade make this an attractive business for us.

Valuations are expensive basis near term financials; however, valuations basis short term financials are misleading as they miss longevity of growth.

Our position size has significant buffer for us to buy more on declines, or over time.

-

- List item

Neogen Chemicals – Investment thesis Final.pdf (691.0 KB)

- List item

16 Likes