Hi all, Though not an expert in calculation Valutaion however cam across an Auto ancilliary NDR auto while reading the current auto trends- Basic from Screener

NDR Auto Component operates in the auto components industry and manufactures seat frames and trims for four-wheelers and two-wheeler vehicles and other accessories relating to car seats [

It was incorporated and listed in 2019 as a part of Rohit Relan Group. It was listed post demerger of the automobile seating business from Sharda Motor Industries Ltd… Key cutomer and risk factor is Maruti due to over dependence, However benefit of doubt is as its small company so lot of opportunity to grow by creating a good proflie.

Hi Kamal,

Thanks for starting this thread on NDR auto & sharing your valuable thoughts.

I have a small position in this stock at ~ 130cr mcap. I was lucky enough to buy it before the up move started in the auto/ ancillary stocks.

While reading about Motherson sumi demerger & Sharda Motor Industries Ltd, I came to know about this demerged entity. Just sharing few points which made me interested in this.

On an initial screening found promoter holding ~ 74%, low mcap, manageable debt, just 59 lakh outstanding shares, trading at 0.6x Mcap/sales, profit making, dividend paying & the final one was the promoter pedigree / reputation. I hope they will be able to replicate what they did incase of Sharda Motor.

As you righty pointed out, ROE, ROIC and ROCE sounds interesting.

My expectations are big here & will keep evaluating the company performance & average up based on that.

Cheers,

AJ

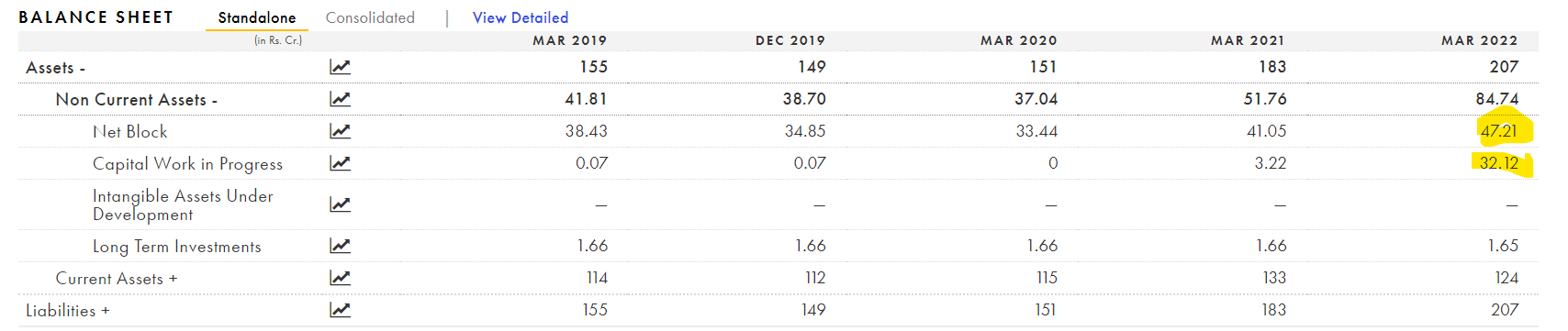

Though I have to still read AR as i said earlier, Its other Income part is from Dividends in its share from Bharat seats and othe assocaite Toyo Sharda… All research on hold due to office work for 2 weeks

Best and Worst both are same for NDR Auto:

Customer Concentration: Maruti and Toyota

As any expansion for Maruti and Few for Toyota, Seat Frame order is coming directly to NDR Auto so revenue visibility is good. New Vehicles are getting added at Maruti or Toyota of Higher cost which need higher Margin seat Frame we can see the same in current quarter.

Now Auto being cyclic sector if Passenger Vehicle Sales go down so will NDR. Any Factory Mishap and Supply stops need to explore contract agreement for such situation.

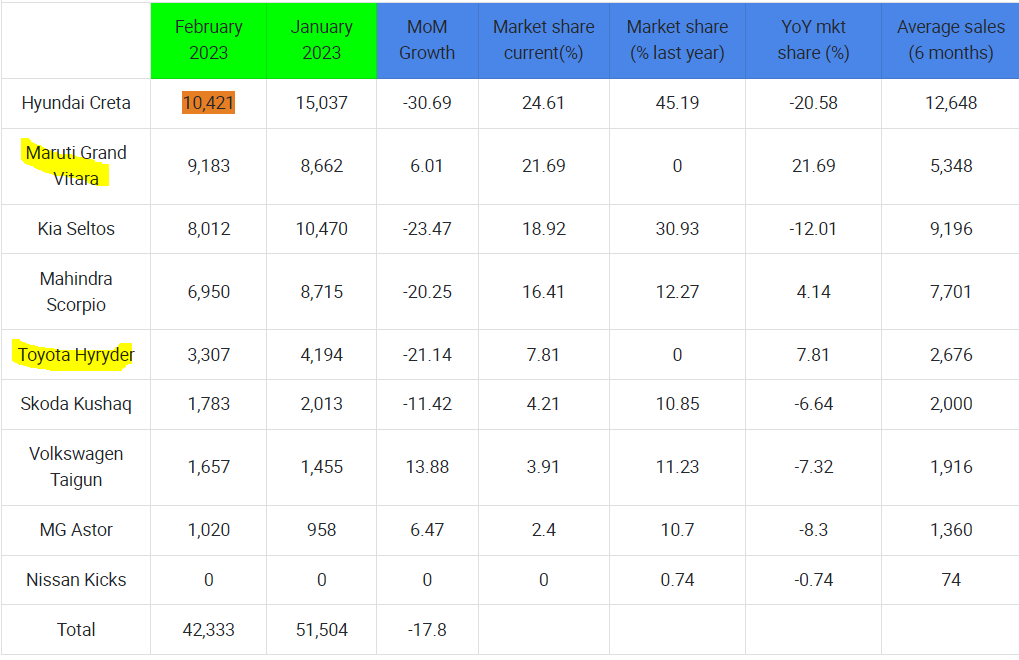

Mahindra and TATA eating Marking share of Maruti but as long as Volumes keep on increasing there is no issue.

Recent Collaboration among Suzuki+Toyota can work well for NDR also.

Does anyone have visibility into NDR’s share of business for the seat frames within Maruti’s overall volumes? And also which models they supply to - SUVs only or all models? Same for Toyota?

Also, any visibility on whether they are developing any new products to increase their value contribution per car?

Lastly, any visibility on their cost efficiency and capital efficiency vs similar competitors?

My hypothesis is that

(a) the market isn’t giving Maruti’s SUV story much credibility yet, as it has missed the bus in the past - however, recent trends are suggesting a reverse l and final strong entry of Maruti into this segment. If NDR is overweighted towards SUVs, then they stand to gain if and when Maruti/Toyota’s SUV biz picks up

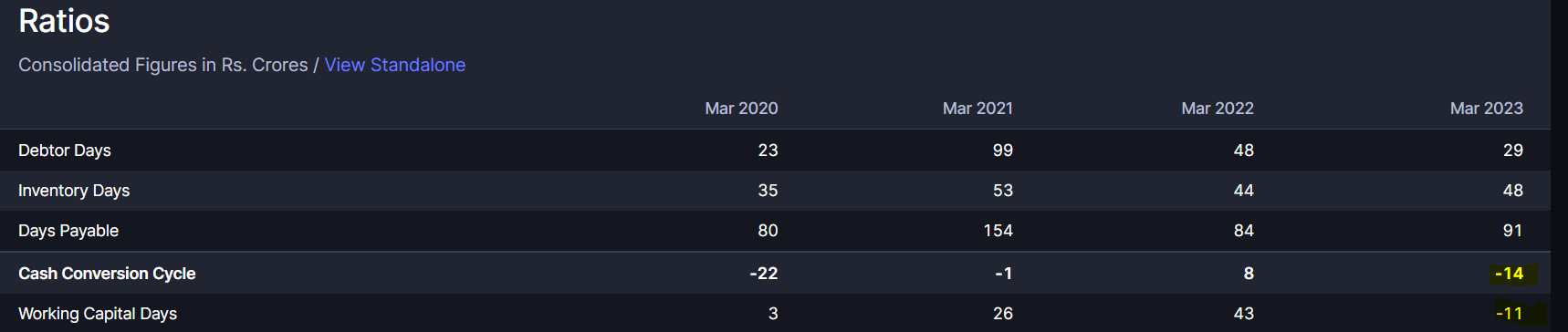

(B) management of working capital tightly is crucial to achieve high turns. They seem on par with peers on this.

I just did a primary reading of the company and talked to a few of my friends in auto industry. I have 2 main observations:

WTD (Pranav Relan) just gives one word answers on concalls without putting any efforts to explain his answers in depth. In companies at this market cap., I have usually seen promoters trying to explain their business to get recognition in capital markets. I might be wrong here, since it just might be his way of communication or maybe if he is trying to protect his business.

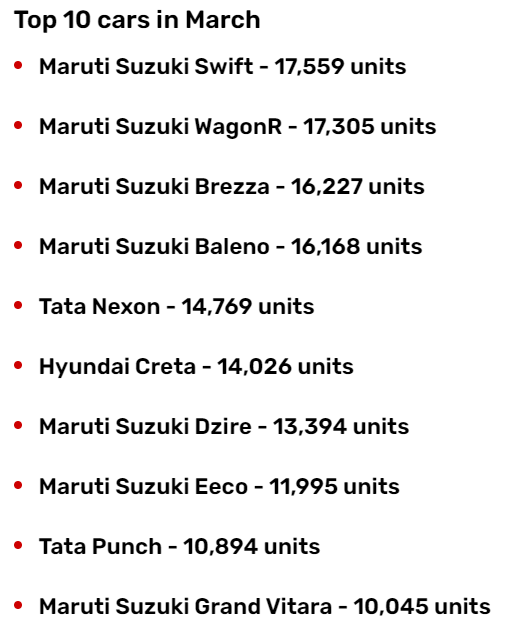

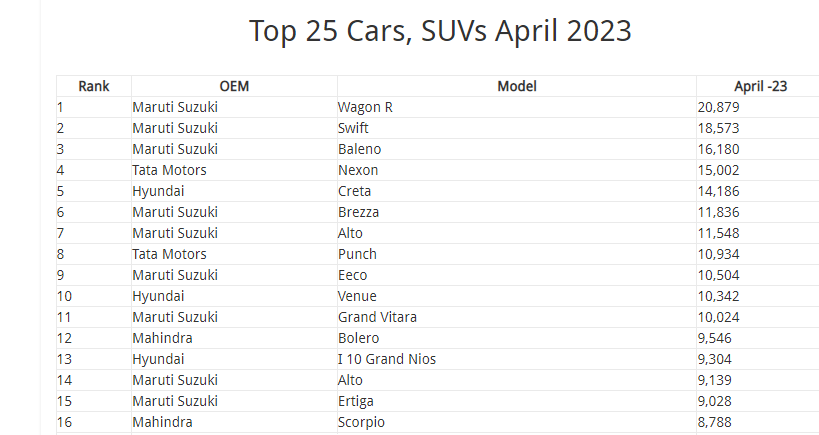

The fungibility issue: The seat frames made for one particular model are not fungible. So revenue is not only dependent on Maruti & Toyota but also the specific model for which they are manufacturing. Apart from a few evergreen models like Wagon-R or Alto every model (which now is doing good) has unpredictability & life cycle and getting a order for new model takes time. This is worrying to me since let’s say new breeza is not a hit, the growth prospect will take a big hit at that instant.

Price has moved 3x from my avg. buying price so far. Never anticipated a quick up move in a short span of 6-8 months. Current Mcap is ~ 390 cr. No change in allocation, Holding with a positive outlook.

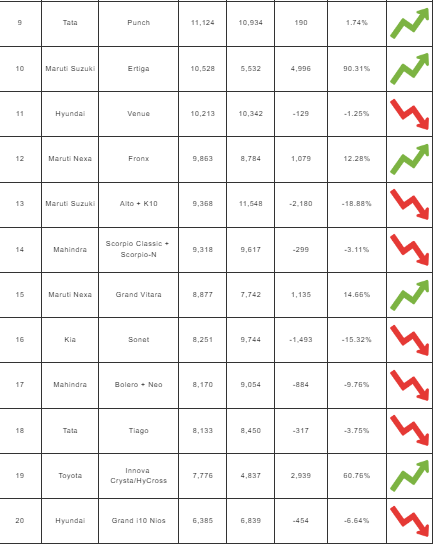

Loss of Hyryder , Alto since they will be discontinued.

Addition of Fronnx from both Maruti and Toyota. whenever launched .

Not Sure about Jimny if this business will come to NDR or not

Superb Results. There might be small production loss in coming quarters as mentioned by Maruti.

Maruti moving more towards mid segment,This works well for NDR from Margin point of view.

visible in current Q

This is to inform you that search & seizure operation by Income Tax Department at the Companys Corporate office and Factories of the Company was conducted by Income Tax Department from May 19 2023 to May 22 2023. As required under Regulation 30 read with Schedule III of SEBILODR Regulations 2015 we will update you on impact and on further developments in near future as and when the situation permits

Is this a concern ? Hows the Relan group in general ?

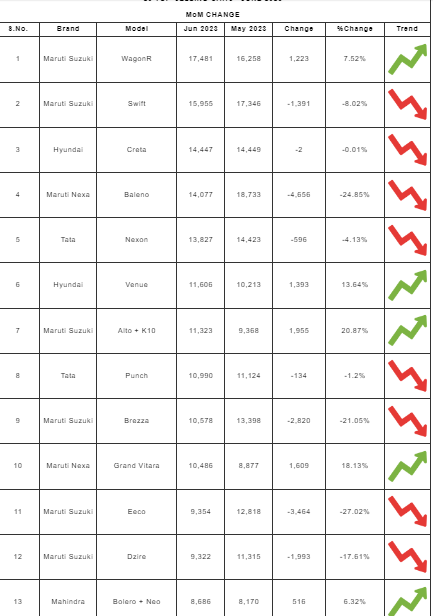

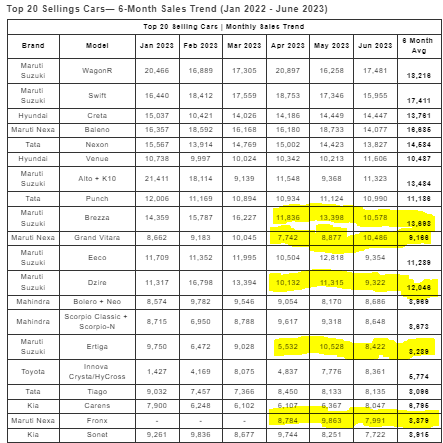

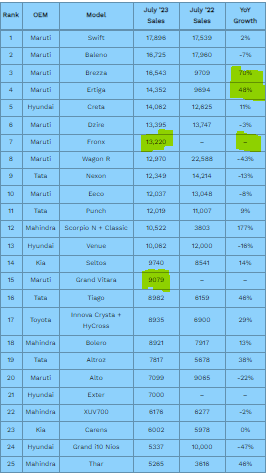

Maruti Rules as usual. Important trend is sales numbers of

High end models. As mentioned in NDR Con Call earlier More sales

of High end Models of Maruti will help in margin expansion of NDR.