Creating thread to keep track of My Investments and Share the information in Public Domain.

This way I will be more responsible learner.

2 Likes

My Current Holding’s are

- Rajratan Gloabl

- RACL Geartech

- Acrysil

- IEX

- Credit access Grameen

- RHIM

- AYM Syntex

- Galaxy Surfactant

- Hester Bio

- Stovekraft

- KIMS

- ShivalikBimetal

- Sasta Sundar

- Gulshan Polyol

- Calcom Vision

- Dynemic Pro

- Gufic Bio

- Gujarat Themis

- Jubliant Ingrevia

- Neuland

- Polychemplast

- Ishan Dye and Chemicals

- Rajshree Polypack

Learning allocation as of my investment phase and Trying to Trim My portfolio.

at Max I would like to have 15-20 Stocks.

11 Likes

Great List! I think that your opinion/tolerance/patience matters the most on this list. It’s like some of the great investors would not like some of your companies, but you have a strong thesis and conviction on that name. So you should read, develop, the idea around each business, that you think of course will be the multi-baggers in the futures. Although you can read the other report, you should build your own story/narration of why this stock will succeed.

Hope it helps

3 Likes

I feel you should allocate more to large and midcaps stocks so to be shock-proof. Having all smallcaps can either yield lot or can ruin.

1 Like

My Key learnings from Market till date

- Look for growth even if you have to pay a higher price.

- If you get Growth at low valuation buy Truck Load.

- When you decide to Buy or Sell just do it, it keeps you disciplined.

- I try to screen stocks based on their Profit and Loss Statement. Topline and margin shall be stable, best if improving.

- Next important thing for me is Capex that too wrt to Import Substitute or Opportunity Size expansion.

- Sometimes I try to play sector Tailwinds with Good Companies. Lancer Containers, Dalmia Bharat, Balrampur and Praj were such picks which gave very good return in short time. Thanks to @hitesh2710 Sir’s Guidance.

- Another Method to identify good stocks is once you find a good company look for investors then check their other holdings and scan their Kundali. I got Lancer Container while checking CheMcrux Investors @prasenjitp04 .

- Another learning to investigate a particular Industry comes from DRHP of IPO Companies . This i learned from @Tar .

- Now days i am reading data on twitter and it really helps.

Valupickr was My Light House to focus in right direction in Ocean of Investing.

It is very important to follow quality people so that you can learn and grow.

Next Steps where i want to focus is allocation. Identifying a good company is one thing but making real money on that company is another.

I will share my rationale about my Pickings in future posts.

8 Likes

Forgot to add 2 more Names:

24. Privi Speciality

25. DFM Foods

4 Likes

Update on the Portfolio

- Exited PolyMechPlast fully

- Exiting RHIM Slowly

- Continued to increase stake in Calcom Vision

- Added Opteimus Infracom

- Continue to track Meera Industries,PolyMechPlast,NatualCapsules,Tinna Rubber,Scandent Imaging,TinnaRubber,

Broad Reason for Recent entry into Calcom,Opteimus(Company Specific reasons are different will post here soon)

Please follow Valuepickr guidelines of starting new portfolio thread and write down rationale of each stock selection. Will delete this comment once you add rationale.

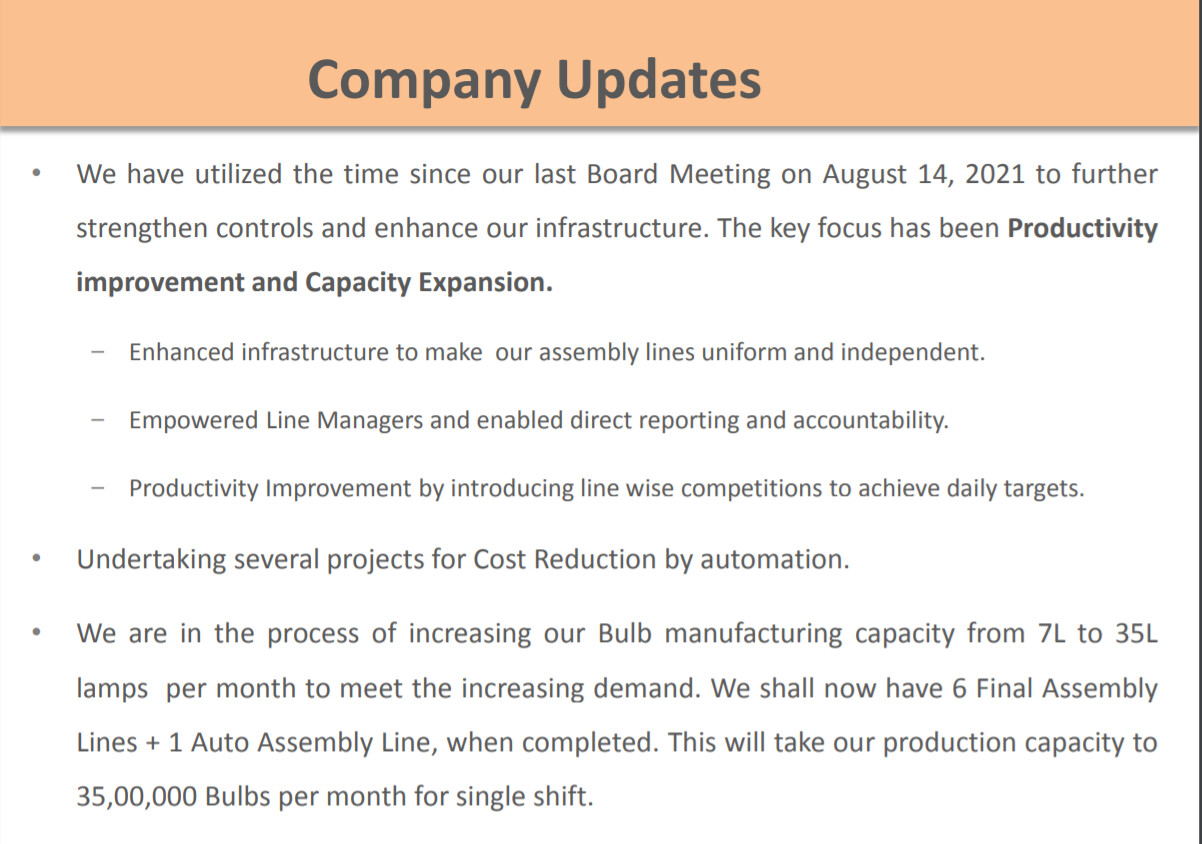

Calcom Vision:

Calcom Vision Ltd is an Original Designer and Manufacturer (ODM) of Televisions CTV Chassis Emergency Lanterns and Electronic Ballast and Luminaries. The company is engaged in the business manufacturing Electronic sub assembly. Their customers include Philips LG and Osram amongst others. The company is having their manufacturing unit at Ghaziabad in Uttar Pradesh.Calcom Vision Ltd was incorporated on May 30 1985 as Calcom Engineering Pvt Ltd. The name of the company was changed to Calcom Vision Ltd on September 21 1989. In the year 1993 the company signed a purchase agreement with Samsung Electronics Company Ltd of South Korea. Also they expanded the installed capacity of B/W Television from 100000 Nos to 250000 Nos.In the year 1994 the company started manufacturing of Hand Mixers on OEM basis for Philips and during the next year they started manufacturing Vacuum Cleaner. During the year 1995-96 the company expanded the capacity of B/W Television from 250000 nos to 310000 nos. In the year 2000 the company launched Power Inverter with one size of 400 VA. Also they introduced 600 VA size during the year 2000-01. During the year 2001-02 they developed and introduced new models of CTV as the demand for the CTV went high.During the year 2002-03 the company’s R&D Department developed many new models of Colour Televisions for European Middle East and CIS Markets. During the year 2005-06 the company’s R&D developed new chassis around Sanyo UOC and Toshiba UOC.During the year 2008-09 the company diversified into Designing and Manufacturing Lighting Electronics items ie. Luminaries and Electronic Control Gear. They developed various products for Osram India Pvt Ltd a subsidiary of Siemens AG and also started supplying the products to that company.

Conclusion: Company Tried their hands everywhere and finally found their Mojo in “LED” Manufacturing.

Basis of Investment:

This One slide was the Motivation behind taking stake

Current Clientele:

They were able to bring in few Chinese Manufacturer as well. I take this as very positive and this suggest about their quality as well as Margin.

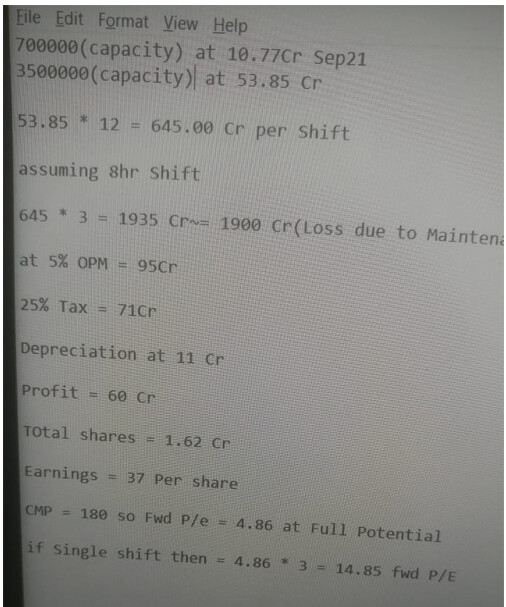

Did Some backend Calculation will wait for story to unfold:

Recent entry of fund houses has further boosted the confidence:

Now Some Anti Points:

- Small Cap so always there is chance of Mismanagement.

- Interest cost seems high and they had one issue is recent past where interest cost got escalated >16% although it got settled now at 11%. Still it’s high will watch this section closely.

- They need to bring in more customers to utilize the capacity and break even faster.

- Execution of strategy over time.

1 Like

Updated Portfolio: Sold My stake in RHIM,PolyMechPlast Fully. Increased stake in CalcomVision, Opteimus.

CreditAccessGrameen:

Best MicroFinance Company in India.

Pro:

- Very Conservative in lending and aggressive in declaring NPAs(60 Days,90 Days Due Period).

- Ticket size is < 50 K, Retail loan to only those individuals who have been with clean history for more than 3-4 years.

- Due to Global Promoters Money is always available to them at good rate.

- Expanding into other states where others are struggling.

- India is still a agrarian Economy and there is very large Opportunity to grow.

- Microfinance Market in india has always witnessed one off event in every 5-6 years( Demonetization, Covid, SKS Micro, Assam). But Credit has withstood with Time and Proven it’s metal.

Cons:

- Market is still not at full potential due to covid but surely improving.

- Madura is still a drag on overall company, waiting for cultural change there.

- Borrower turn bad as happened in Assam.

- Microfinance has to bear the burnt of any national disaster.

1 Like

Opteimus Infracom: Had a long Journey from Phone Trading company to ESDM Company.

Rationale:

- They brought in Wistron India Head to the company last year and immediately ~1400 Cr Joint venture was announced this they are planning to take to sales of 38000 Cr with in 5 years.

- The company at present has capacity to manufacture 3 lakh wearables and hearable devices at present which it plans to more than double to 7 lakh units per month by March.

- Got License under PLI.

- Have capacity to manufacture 1.5L laptop Per Year. Operating around 75% utilization.

- With Wistron on board and Production slowly Moving away from China. Opteimus Electronics(Subsidiary) will become production house for Wistron.

- High Promoter holding(74.93%).

Cons:

- Company was not able to Walk the Talk in Past.

- Debter, Working Capital and Payable days increasing to alarming levels.

- Need to watch the story and PLI how it plays out

3 Likes

Rajratan Global:

Company is well covered on the it’s thread on Value Pickr.

Pro:

- 30% demand from New Vehicles,70% from Replacement Tyre sector.

- ICE,EV,Hydrogen whatever it is All need Tyres .

- Recently Most of the Indian Tyre manufactures have increased capacities.

- ~50% market is with Rajratan, Approved By Almost every Major World Manufacturer.

- With Chinese duty going away chinese Steel is no longer competitive with Indian steel in terms of Cost so indirectly Chinese Tyre manufacturers are coming to Rajratan Thailand.

- 20K MTPA capacity is about to start Production in Thailand,60K MTPA will come online in 1 to 1.5 years.

- New Plant coming up at Chennai will work hand in hand with local OEMs and will Augment the Thailand Plant due to it’s port proximity. All this will help in Margin expansion.

- In recent Presentation they claim of trying additional sectors of aluminum cladding for Optic fibers.

Cons:

- Thailand plant enjoys tax benefit for existing capacity which will be levied from 2024.

- With Demand Increasing Arti Steel, Tata Steel(Read Competitors) may Increase capacity as well. With too much capacity sector may become commoditized and Margins will be compressed.

- Margins are at Peak, After enjoying 2 rapid years of growth company might slow down.

4 Likes

Sold my stake in Neuland labs yesterday, was riding on their innovation led growth which seems not as rosy as was on my mind.

Deployed the Cash to Ishan Dye and Chemicals which had fixed assets of ~30Cr and having a Capex of 100Cr So Major growth can come with backward Integration Margins expanded in current Quarter need to ensure how much of it is sustainable.

Also Purchased More of Shivalik Bimetal in Recent fall.

Sold Off My Calcom after it broke support of 120 waiting for it to go below 100 or Cross ATH to add it back.

2 Likes

Investing Points

- Any Good Company in it’s journey makes a name for itself through Quality and Product(Services). That is why during down time also it is important to remain invested in such companies because it’s just about time when next leg of growth starts with new initiatives. Promoters of such companies also play a big role in this ride.

- While Investing in finance companies one thing where I put most emphasis to check is How good and conservative promoters are. Generally such companies are available at premium compares to peers but it’s worth it. Such companies tend to survive and thrive longer in market.

learned this from Peter Lynch book and Observed in Market e.g Credit Access Grameen.

1 Like

Sold

- Polymechplast(Feb 2022)

- Neuland(Jan 2022)

Entered

- MAS Financial

Portfolio allocation

- Rajratan Global(12%)

- Credit Access(12%)

- Shivalik Bimetal(11%)

- RACL(7%)

- Acrysil(6%)

- Hester Bio(6%)

- Gulshan Polyol(6%)

- IEX(6%)

- KIMS(4%)

- AYM Syntex(3%)

- Jubliant Ingrevia(2%)

- Privi speciality(2%)

- Calcom Vision(2%)

- Rajshree Poly(2%)

- Galaxy Surf(2%)

- Optimus(2%)

- Ishan Dye(2%)

18.Gufic Bio(2%) - Stovekraft(2%)

- MFL(1%)

- Dynemic Product(1%)

- Gujarat Themis(1%)

- MAS (1%)

1 Like

Just one feedback, on lighter note the portfolio name says common man’s portfolio but most stocks are not common…

1 Like

He He.

He He.

Original name was “AAM AAdmi Portfolio” short for “AAP” but VP Moderators asked me to make the name apolitical  .

.

Now coming to stocks it is more about methods of a new bee how he/he starts and matures into a investor after years of learnings mine is somewhere in between.

1 Like