Execution is impacted in Monsoons typically. H1 has had a double whammy for a lot of EPCs - elections, then Monsoons.

1 Like

As I cautioned exactly 1 year ago market is correcting valuation premium which purely happened because of excessive euphoria and liquidity coming into infra stocks. NCC has delivered negative return since then despite all the great stories posted about the company’s prospect.

This should server as another reminder to investors about inevitability of mean reversion. In bull market every price move has its own rationale and narrative but instead of being swept up in those one should always be mindful of valuations.

Just to clarify there is nothing wrong with the company and when the stock multiples comes below its historical averages I’d be among the first to start feeling positive about the stock.

What is the historical avg of PE multiple for NCC (& Infra stocks)? Is it around 16?

Yes that’s correct. I think around 190-200 stock should start getting into value zone.

It’s almost there now - around 210.

I do have a question though. The historical PE multiple may have been 16. But given the focus that current govt has been and would be giving on infrastructure development & with the fact that NCC works “closely” with many governments (center & state), shouldn’t they get a better multiple?

Granted, their net margins are just at 4% (but that’s the case with the sector) & there seems to a lull in project executions in this fiscal, which NCC says is due to elections etc. But if things pick up after this, shouldn’t they get a better valuations? I compared NCC with KEC. The business numbers of KEC is much lower than that of NCC but KEC trades at much higher valuations. And inspite of cut in revenue guidance for current fiscal, they have retained the order inflow guidance as they are sitting with 9-10K worth orders in L1, which they expect to be awarded in March.

Just curious to understand everyone’s views on valuations front.

1 Like

Working with government is actually a big negative and this is the main reason NCC gets lower multiple as government customers tend to be the worst ones what with payment delays, execution bottlenecks etc. The price action that NCC saw in last 2 years was far out of the stock character and there clearly was some extreme discounting of all positives (including the ones you mentioned above) that investors were factoring in about the company.

Comparing with KEC is pointless as this is another highly overrated and overvalued stock for the reasons totally unknown to me.

In my experience every bull market has its phases and favorites and as far as I’m concerned liquidity that we saw in PSU and infra stocks in their heydays will take much longer to come back. We might see money moving to new sectors now.

So even if fundamentally there is nothing wrong with infra companies, their stock prices will for sometime now totally depend on earning growth and NOT on any narrative driven rerating.

S Naren of ICICI PRUMF has made some news off late with his warning on valuations & safety margins. He advises investment in debt, REITs, and preferably large caps and to be very very careful about small & mid caps.

Two days ago, his firm has bought additional 5 lakh shares of NCC. I feel the current sell off in NCC is unnecessary pessimism.

1 Like

NCC gets LoA for a project worth ₹1,480.34 crore from Bihar Medical Services & Infrastructure Corp

https://x.com/CNBCTV18Live/status/1903431851873882504

2 Likes

Two new orders worth ~11000 Crores from BSNL (Bharatnet project)

1 Like

NCC has received a total of around 20000 crores worth orders just in the month of March. Announced additional 5773 crores worth of orders today in addition to the three orders already received (10800, 2100, 1400 crores respectively)

3ffb4def-2860-41f5-b449-207d7b6964c2(1).pdf (764.7 KB)

4 Likes

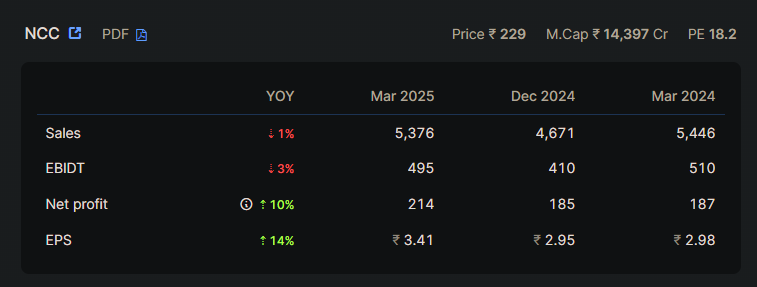

Looks like collection problem still persists…lower revenue (inspite of a big order book) and higher interest outgo (as additional working capital is needed in place of reduced collections)

On the positive side, they are already giving FY26 guidance, which reflects confidence in business (if 10% topline growth is good or decent or okish - that am not sure)

2 Likes

Very good order book. But revenue down both YoY & QoQ. Perhaps due to longer duration monsoon this year all over India?

Even before Monsoon their revenue growth is nill. This whole year they recorded negative revenue growth

Yes, collections from Jal Jeevan projects were an issue. It was the case for other companies like KEC as well.

Let’s see how H2 turns out

Hi is it common for the companies to withdraw guidance - the NCC Management has withdrawn any guidance for FY26 - what are the members expecting for the next 2 quarters ?