The CEO provided some more context about real money gaming.

In the above interview, the CEO shared his vision and also reiterated the company’s strategy

So if you see Nazara’s teleco business which we have been doing for 15 years, it is almost now 13-14% of the overall portfolio and our IPs which we have acquired and grown over last three-four years like kiddopia, Nodwins, Sportskeeda, the World Cricket Championship; they are all growing so. If you look at our strategy, it has been to build all the friends of Nazara as a concept and then continue to build value with those founders at subsidiary levels.

The acquisition spree continues in Nazara - Majority stake in 3 companies so far after listing. Note that Publishme is a company based out of middle east.

One of the key benefits of listing is , it improves credibility of the company as the listed company has to operate under the purview of market regulator like SEBI who plays the role of watchdog. Nazara’s strategy is inorganic growth and the listing certainly helps to expand friends of Nazara at a brisk pace.

The world over is looking towards sharing model wherever possible for optimum utilisation of available resources - Airbnb or cloud providers like AWS, Azure, GCP. Nazara is actually playing a similar game.

- Identify and acquire majority stake in companies which are having more probability of success

- Share the tips/tricks to scale up - I am not sure whether they charge some fee here

- In the future, once it becomes significantly large, it will look for benefits of scaling - it can be at infrastructure level(Common Physical location/IT/Storage etc) or Better contracts with Sponsors(Nodwin) or Packaged Ad revenue(WCC3/Kiddopia etc)

WCC3(Game owned by Subsidiary of Nazara) recently got first in-game integration with Axe-Deodrant(Hindustan Unilever)

Axe understands that a good portion of their target customers(young male) are interested in cricket & gaming in India and WCC3 is specifically catering to that segment with enhanced features. Similar types of in-game integrations can be expected in many mobile games in the future, for the simple reason that mobile is omnipresent & games can get you glued for a longer duration. The brands always look for the marketing channels where they can find customers.

Aside, look at this trend of virtual humans - Meet Rozy Oh who has bagged more than 100 advertisements so far and always remains a 22 years old. Can Nazara make any virtual human( Chota Bheem etc) like this? I don’t know. It is too far to even think on that front.

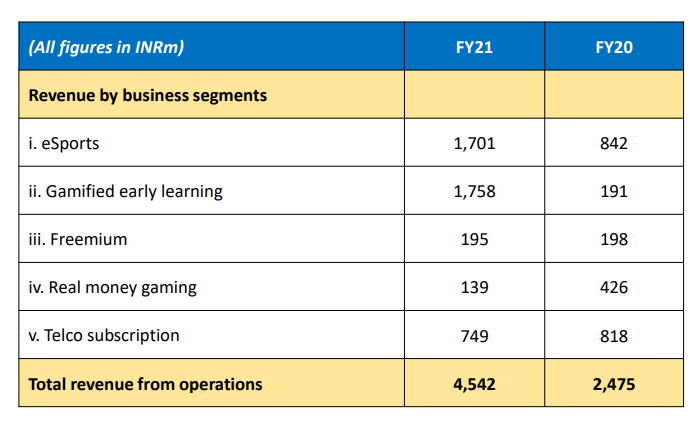

So far, the narrative is going great with the growing acceptance of e-sports(recent addition in Asian games) and introduction to in-game integration with brands(Axe). For the numbers, we need to wait for quarterly results.

Discl - Invested 3% of Portfolio.