Intro: Nazara was started in 1999 by Nitish Mittersain while he was still in college. He doesnt have any meaningful interest in any other business. He is still involved in the business along with the CEO Manish Agarwal who has been with the company since 2015

I have highlighted my commentary in italics. Some of it is just opinion

In order to understand Nazara its essential that one understands the gaming industry and its potential in India. So in this post you ll read about the gaming industry as much as the business verticals of Nazara

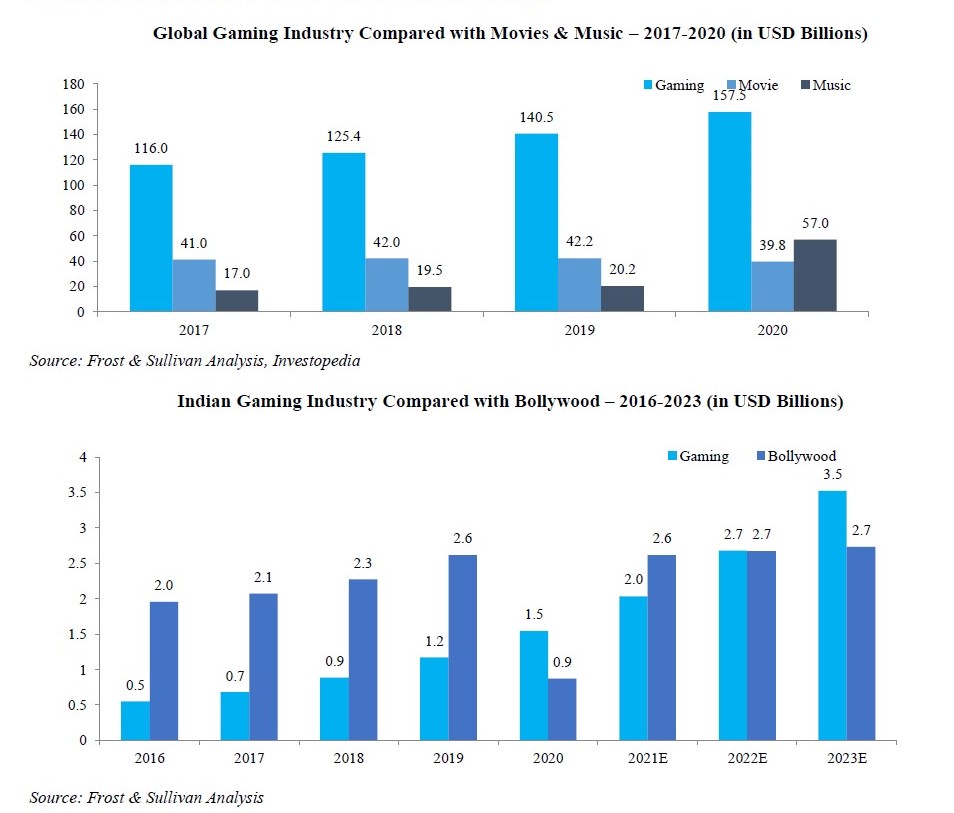

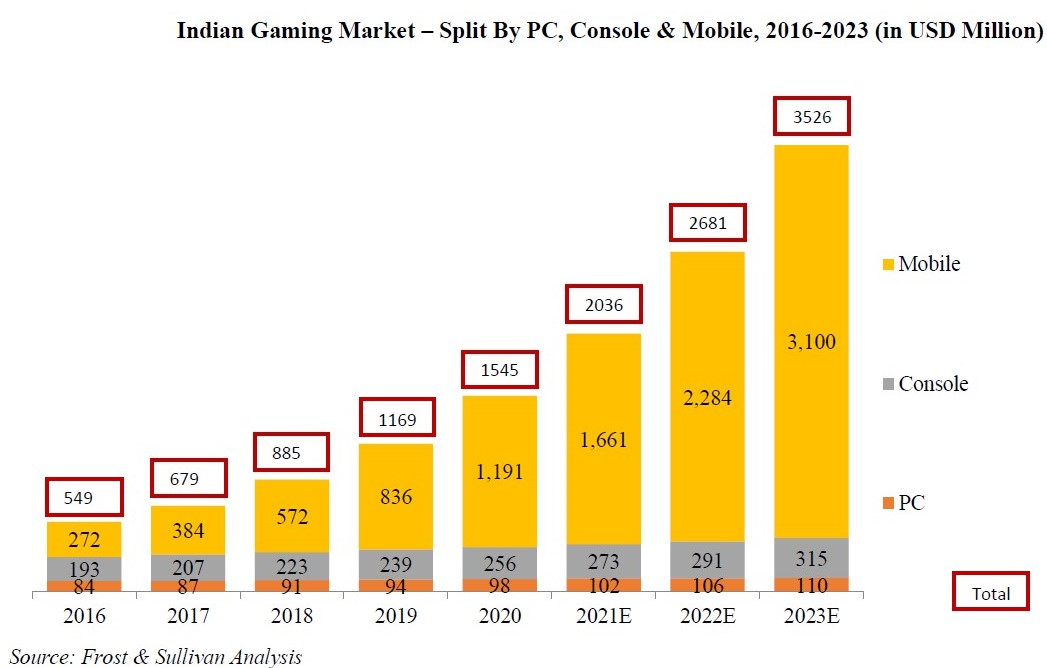

Below chart illustrates the size of the gaming industry

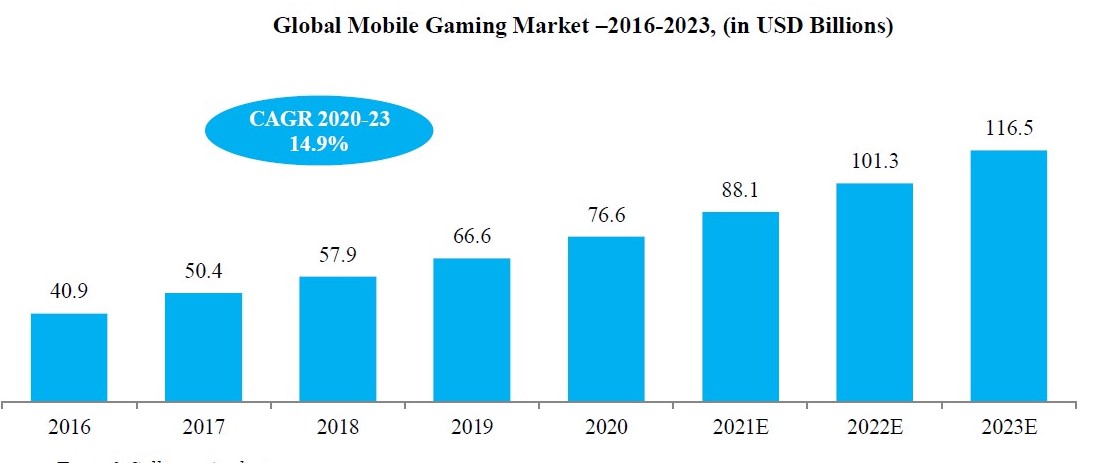

Globally, Mobile gaming is growing faster than console / pc gaming and also forms the largest chunk in terms of revenues. Half of the global population now owns a smartphone, which makes for a massive market of potential mobile gamers; and, unlike PC and console gaming it’s a lot more affordable. It is expected that the number of mobile gamers will continue to grow faster than PC and console gamers as global smartphone penetration increases, and more of those smartphone owners become casual gamers.

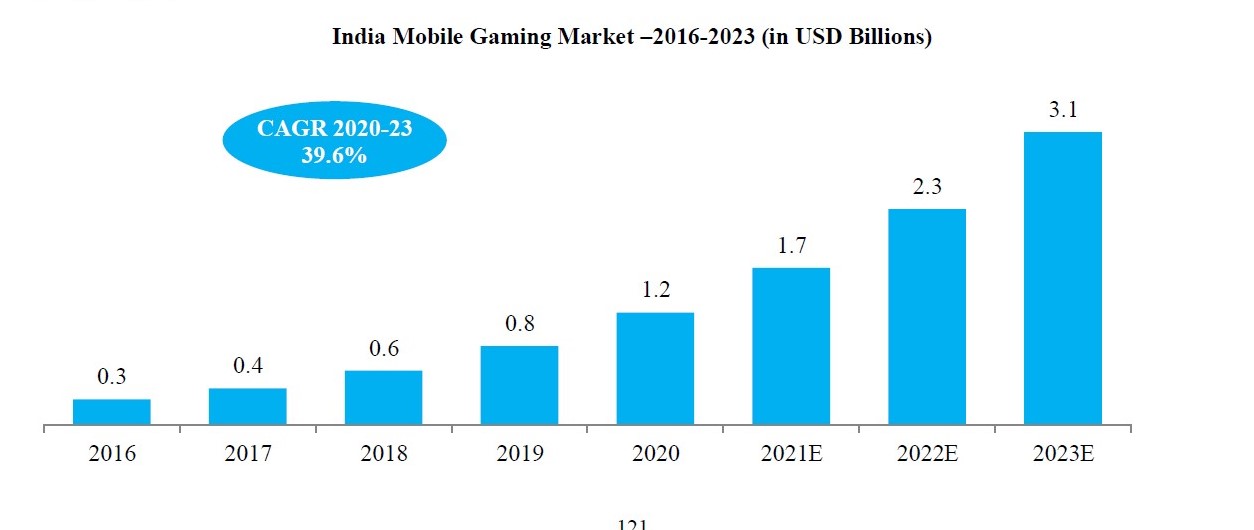

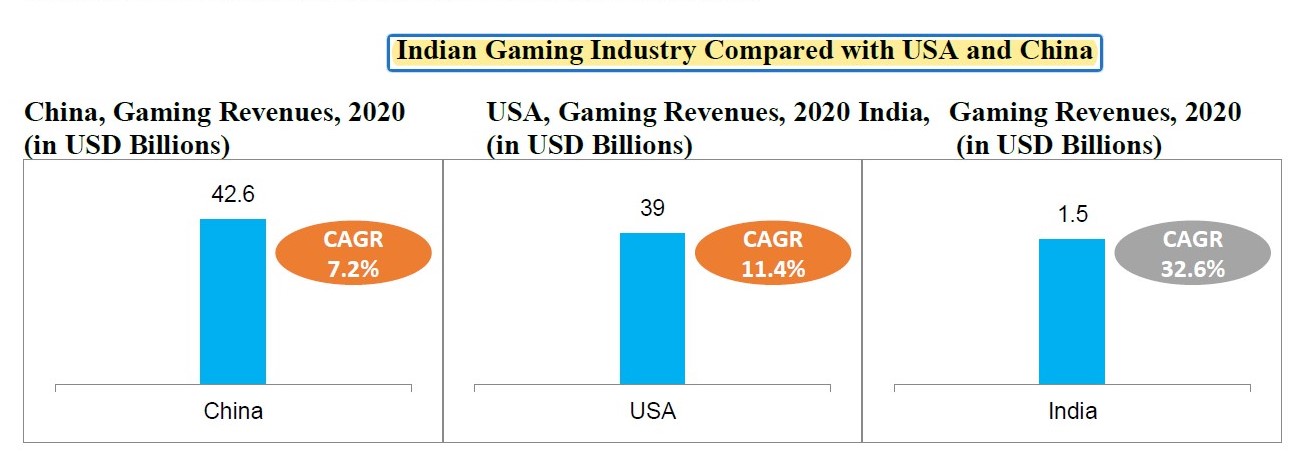

The story isn’t very different at home either. Not only is mobile gaming largest in terms of revnue and the fastest growing segment in idnia as compared to PC and Console gaming. This segment was valued at USD 1.2 billion in 2020 and is expected to reach a value of USD 3.1 billion by 2023, growing at a CAGR of 39.6% during this period as compared to the growth rates in China and the US, which stood at 14.6% and 12.2% respectively

Changing Landscape

-

Increase in numbers of gamers due to cheap data & growing mobile penetration

-

Demographic shift (average age of Indian gamer is 24 years old vs 31 & 32 years in USA and china respectively)

Teenagers playing video games in todays India are likely to continue gaming in their 30s.Gaming is not something most people start at the age of 30

- Increased disposable income along with habit formation(The average annual spend on gaming per individual in India is USD 23, while in USA and China that stands at USD 113 and USD 115 respectively)

A lot of 20 year olds are willing to pay for gaming as they see it as another form of entertainment and are likely to spend more as they older

-

Local games are going mainstream (games like ludo king carrom teen patti have become very popular specially during the lockdown )

-

Social Gaming : Large online Communities are formed around certain popular games. Once a community reaches a critical mass it tends to grow organically (for a game publisher this means new users with minimal Cost of acquisition)

-

Free to play games: Not too long ago most games were played on PC or Console(XBOX,Playstation,etc) Not everyone could afford it.Today you can play for free and that to anywhere anytime on your phone

Whats an In-App Purchasing(IAP) Model? Historically most free mobile Games used to generate revenue via in-game advertisements (ad banner, video ad between 2 levels etc) but this has completely changed in today’s landscape where most free games come with the option to make in-app-purchases. Users can play for free but they have to pay for certain features / items (extra lives, weapons, maps,collectibles, bonus levels etc).These features wont be available to a basic user or if available it ll require a lot of time to procure. In india the mix is still skewed towards advertising model but that’s changing. Globally Some of the most popular games by revenue such as Dota, Fortnite, PubG, are free-to-play.Once a game is launched, incremental costs for content updates are low, meaning incremental revenues from in-app purchases can have a disproportionate effect on the bottomline

Not all gamers are same. There are about 380 million gamers In India. 90% of them do not pay. Even among the ones who pay for in app purchases, most of the revenues come from a small cohort of gamers. The ones willing to pay are unlikely to play 20 different games. They have a tendency to spend long hours playing a select few games. If you are a game publisher who wants to drive revenues through In-App Purchases you want these serious gamers. They can be very loyal. They wanna be part of social gaming community and they dont mind spending. In the Indian context think of what PUBG has been able to establish Pure advertising model works better with casual gamers . Such kind of games don’t live long becausse they are usually very easy and without a little challenge people eventually get bored. However most developers who make such mobile games are aware of it.It still works because its not very expensive making a basic mobile game.

Freemium(free-to-play) games110 mn+ installs across Cricket (WCC1, WCC2, WCC3, Big Bash League, Rivals, Battle of Chepauk), Carrom and TT

WCC is the world’s largest cricket simulation game franchise on mobile.Its also the most downloaded cricked game.( Acquired 52.38% stake in Dec-2017)

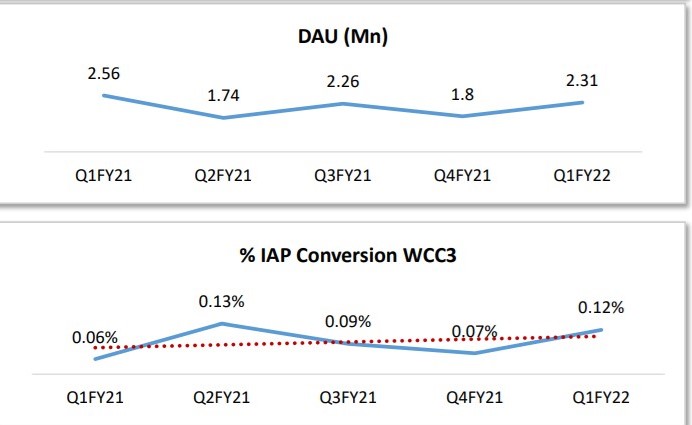

Its played for ~47 minutes / day by ~13.25 Mn monthly active users. (The average time on a casual game is just 15 min)

The Game has a very strong following among those who love virtual sports simulation . It gets over 120,000 downloads every day organically without any marketing spends

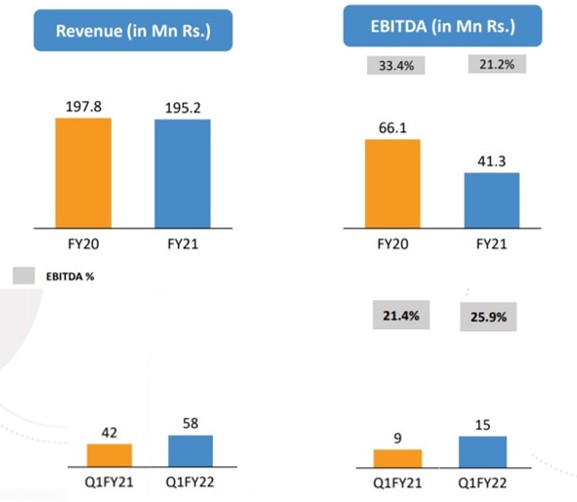

As you can see the Daily average users(DAU) is stable with a few spikes seen during IPL . The growth is going to come from in app purchases in WCC3. Currently the conversion is at 0.12% . They expect this number to reach 1.0% by FY25. (In app revenues grew by 75% YoY in Q1FY22).

As per management Revenues here were flattish for FY21 because they switched to an IAP model from Advertising model and EBIDTA dipped because of content cost for latest game title WCC3

Sports game titles generally have a longer shelf life. The best example of this is a game franchise called FIFA by EA sports. Even though there have been a lot video games on football over the years FIFA is the one with a cult following.Something like that is happening here.

ESPORTS is video gaming at a competitive level. Millions of viewer watch this around the world just like any other sporting event.The prize money in some of these tournament goes into million of dollars. Its so mainstream now that Its already a part of Asian games 2022 and There’s talks about including eSports in the Olympic Games.

Its a billion dollar market growing at 16.15% CAGR and China is the largest esports market in the world. However the eSports market in India is expected to grow faster than china at a CAGR of 25.1% for the next couple of years.

The eSports ecosystem consists of game publishers, gamers, Media & OTT platforms (Twitch, YouTube, etc.), and eSports companies

eSports companies (Nodwin, Jetsynthesys, Gaming Monk, Gamerji, e-war etc) are the ones that host regular events and tournaments where professional players compete for large prize pool. They provide infrastructure , manage online registrations, provide administrative support and contribute to prize pool. Game publishers are their partners in this. Game Publishers are the ones that provide game titles.For game publishers esports is like a marketing tool. More tournaments means more visibility and more fan engagement. Some game publishers have their own Esports unit. Then u have your professional Gamers who are often part of a Team just like in cricket. Some professional gamers are nothing short of celebrities in the gaming world. Streaming live for hours, these gamers get millions of views on YouTube. Then u have media and OTT platforms who showcase these events .(YouTube,Twitch,Facebook gaming,Hotstar etc). Just like in any other sport Media and OTT companies pay for media rights to broadcast/stream. Now as the popularity of eSports grows, more media companies will want a piece of the action and these media rights will keep getting more expensive. Globally there are tournaments that are filling stadiums bigger than our cricket stadiums. Also as viewership of Esports increase in India , more sponsors will want in. All of this is still at a very nascent stage , with a growing number of casual gamers turning professional, increasing sponsorship from brands and a steady increase in the number of tournaments and cash prize pools.

Nodwin Gaming is the Only company in India to have rights over professional eSports tournament IP’s & content IP’s across regional, national and international eSports.Some IPs are 100% owned by Nodwin while others are shared with game publishers.( Acquired 54% stake in Jan-18)

It has a market share of about 70-80%(measured in terms of the total prize pool)

Its a pioneer and it has strong relationships with global gaming publishers and platforms.It has exclusive partnerships with the biggest names in the industry and manages gaming events such as the ESL India Premiership, KO Fight Nights, etc…

Media rights licensing contributed 49% of Nodwin revenue in Q1FY22 and 55% in FY21.Game publishers formed around 30% and Sponsors 15%

*One of the games which really drove esports popularity in India was PUBG which got *banned last year( Anti-China sentiment). The game is back with a new name and its original korean game publisher Krafton. Recently Krafton invested Rs. 164 crore for ~15% Stake in Nodwin. The influx of funds will be used for the development of esports in three regions – South Asia, Middle East and Africa. Currently there are no offline events because of restriction due to covid but whenever its allowed we can expect Nodwin to host the official event.

It also hosts tournaments for WCC(now sport simulation games based on football or basket ball or cricket form a very small part of esports globally. most of it is games like PUBG DOTA CS etc however sports simulation games is gaining traction and in a country like India where cricket is like a religion i see a strong possibility of a cricket simulation game ,playing a key role in introducing a lot of first viewers to esports and once ppl watch it doesnt feel so weird to them and they actually enjoy it. and more viewership means more sponsors, more game publishers and more money)

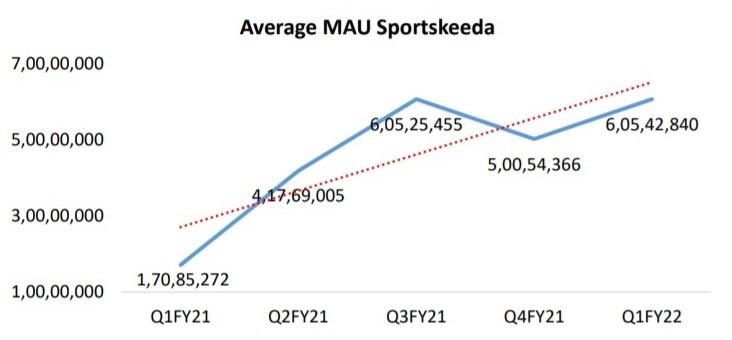

ESPORTS MEDIASportskeeda ia leading sport and eSports news destination website with content across WWE, eSports, cricket, soccer and basketball . (Acquired 63.9% stake in June’19. ) It’s the argest eSports news destination in India.

Content on Sportskeeda is primarily sourced from freelance sports journalists in India and overseas.

Sportskeeda generates revenues by displaying advertisements on its website, which are sourced through leading ad-networks and programmatic-demand-channels. (programmatic revenues means that you have an inventory on your platform, you connect it to the various ad networks which see fitment of their advertisers and the users which you have as a publisher on your platform, and they serve ads)

Q1 FY22: 60.54 million MAUs and 121.44 million visits per month

GAMIFIED EARLY LEARNING tries to bring various elements of game play to the learning landscape to make it more entertaining and engaging. USA is the largest contributor to this market and is expected to reach a size of USD 12.6 billion by 2023, growing at a rate of 47% CAGR. The current size of this market in US alone, is more than 2x of Indias entire gaming industry. The Size of opportunity is huge and its at a very nascent stage globally. So far schools in India have not completely adopted the concept of gamification of education as they feel it takes out the seriousness from education

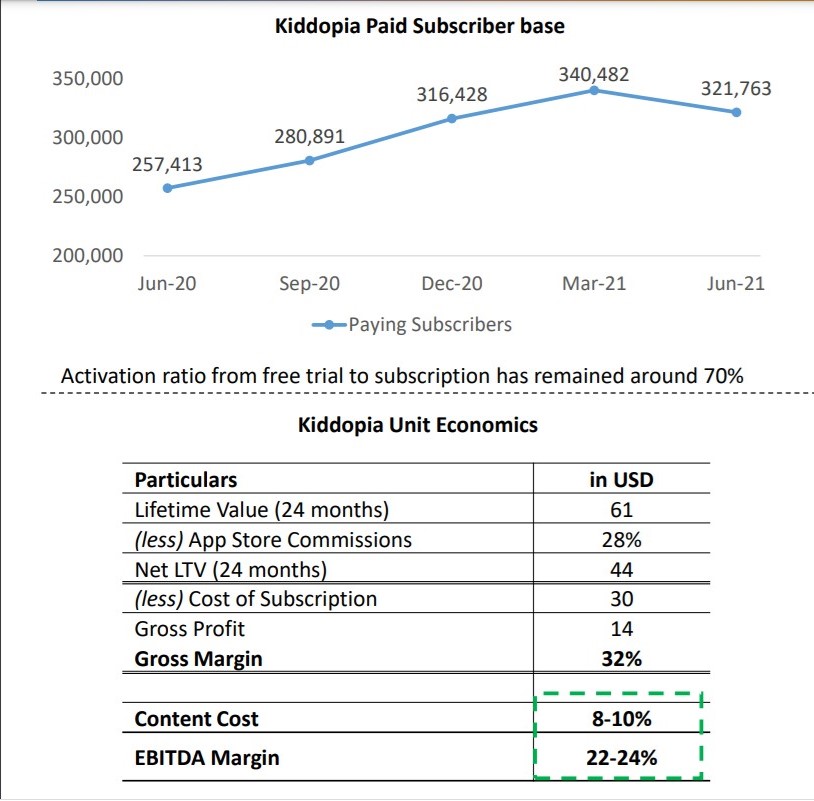

Kiddopia is one of the most popular apps in gamified early learning in USA(Acquired 50.91% Stake in Oct-19) The content for Kiddopia is designed in-house in india while focusing on basic Math, ,Spelling, Colour, Basic Games in alignment with Pre-School and Kindergarten. It caters primarily to children aged between two to 7 years.

There is an initial trial period of seven days, following which one can opt for a monthly or annual subscription plan. Yearly is priced at 59.99 USD. Monthly subscription rates have recently been revised to 7.99 USD from the earlier 6.99 USD per month.so that’s a 15% jump, benefit of which will be seen in the coming months.

It gets 89% revenues from US but its share in US is just 4-5%. Its already active in UK, Australia, Germany, Spain,. Company claims that Right now they are still tinkering in those markets trying to get the find the optimum CAC

Very good trial to activation conversion ratio of 70%. Monthly churn is in a low range between 4% - 7%

When Nazara acquired Kiddopia in 2019 the subscriber base consisted of 115k paying subscribers. That has grown to 320k paying subscribers as of June 2021.This is a 25% increase as compared to June 2020 (257,413). However, compared to March 2021 (340,482) we have seen a 5% decline. That’s due to the impact of Apple’s privacy policy. Apple sometime back launched a new feature because of which now one needs explicit consent to track users on other apps/websites .The result has been that it has reduced the data on the users. User identification for targeted advertising is not possible like it used to be. Kidoppia gets more than 90% users from Ios but this not just a kiddopia problem alone .Their competitors have the same problem. The company believes the majority of this impact has been absorbed.

Although the revenue traction would continue to remain robust one shouldnt expect ebidta margins to go up because they will continue to invest to get higher market share

I would like to see if this growth sustains once preschools re-open .

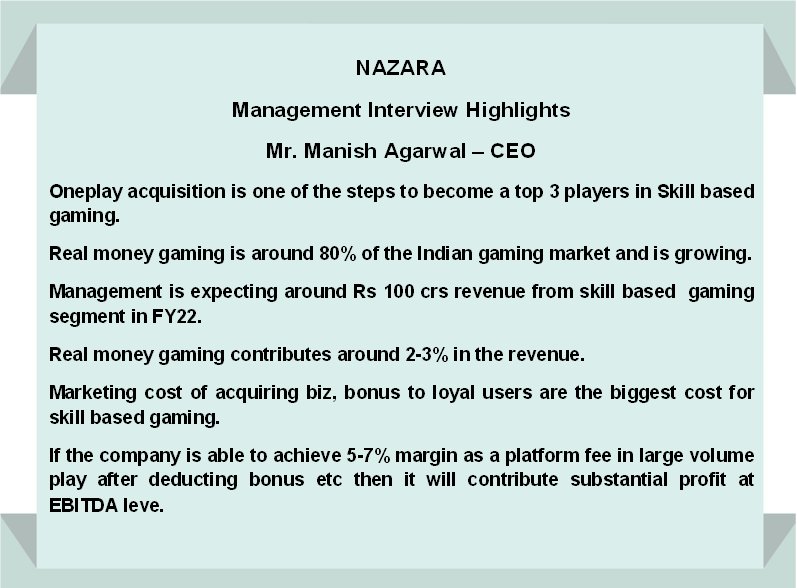

REAL MONEY AND SKILL GAMING are games were players have a chance to win money based on outcomes of skill or chance. Games such as Dream 11,Online Poker, Rummy, ludo, have gained significant traction in the Indian market in the recent years. Real money skill gaming contributes 80% of the mobile gaming market

Between 2018 and 2020, Online Fantasy Sports (OFS) revenue registered a 9.4x growth. While cricket remains the favourite sport, Indians have started following football, kabaddi, basketball, hockey etc . 50% traffic is from Tier 2 and Tier 3 cities

However this category is fraught with statutory risk and there have been instances of multiple states banning all forms of online real money gaming. Gambling is a state subject in India . Real money gaming Is gambling if the outcome is based on chance. More skill, less chance is legal. Now what is skill and what is chance is subjective and that’s where the whole debate is.

Then theres the issue of taxation. Currently GST is paid on platform fees but there is talk of imposing GST on prize money. Govt has formed a committee to resolve these issues but there isn’t much clarity yet

HALAPLAY is a sports fantasy app where users can form their own teams (cricket,football) and bet real money.( Acquired in Mar’19 -64.7% Stake) They charge a 6-7% Platform Fee based on the total gaming transaction of the user.So as the number of users increase, the prize pools get bigger and so does Halaplay revenues. (It also has Qunami which is a trivia game but I don’t have info on it worth sharing)

Now this segment is just 3% of revenues but they do plan to take this up to 8% of revenues. (Now the problem with that is that nazara as a company looks for profitable growth in all their business vertical. at a an ebidta level but this whole real money skill gaming space is seeing a lot of companies getting massive funding from PE funds.and these companies dont care abt profitable growth right now. so how do u compete with them?).

Nazara feels this segment is very large but they want to avoid huge cash burn for user acquisition till theres some clarity on these statutory issues .Its currently loss making. They have indicated that they might do an acquisition here at some stage.

TELCO SUBSCRIPTION Business is Nazara’s legacy business. Its primarily focused on offering a catalogue of Android and HTML5 games to mass mobile internet users and first-time mobile gamers in emerging markets including India, South Asia, Africa and Middle East. They enter into revenue sharing arrangements with telecom operators.

1,000+ games offerings to mobile users in 58 countries through 52 telecom operators (Revenue from this section contributed 97.91% of revenue from operations as of FY2017 from 113 telecom operators situated in 61 countries).

They are typically offered in a bouquet format, through periodic subscriptions or on a downloadable basis. India business took a big hit once Jio came out with bundled offers

This business has been on a decline for the last 4 years. When u have so many free games why will anyone pay for a game which is inferior in content, So I feel these revenues are expected to decline even though management has guided for flattish revenues. Management is still hopeful and trying to revive this segment. Recently they acquired rights to distribute a library of premium Disney and Star Wars games

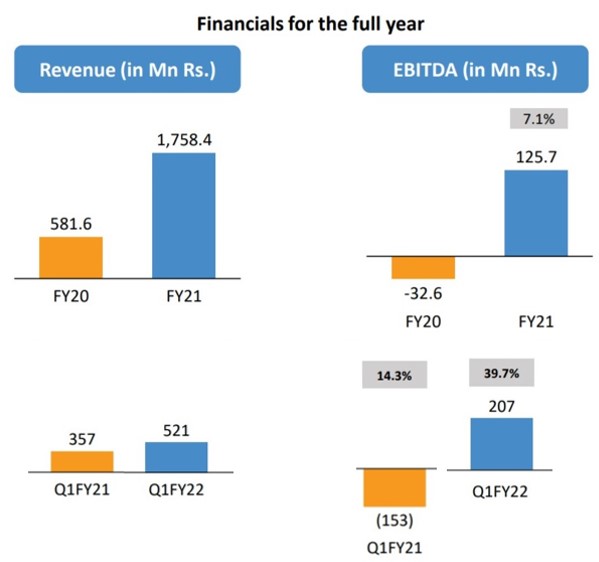

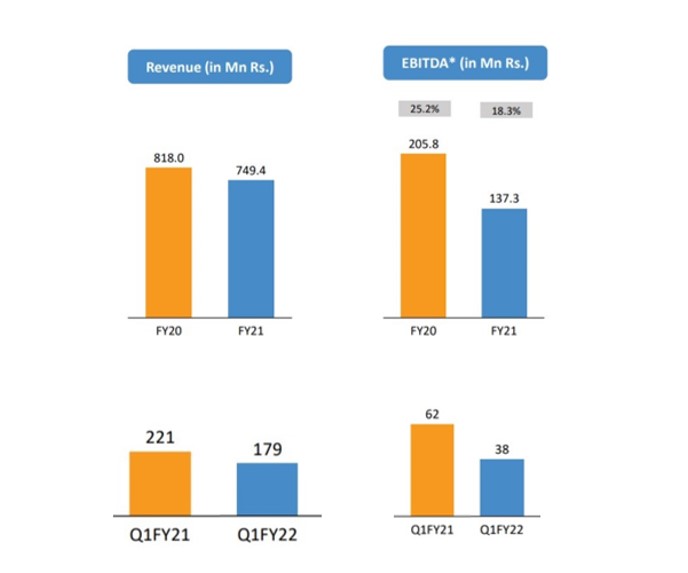

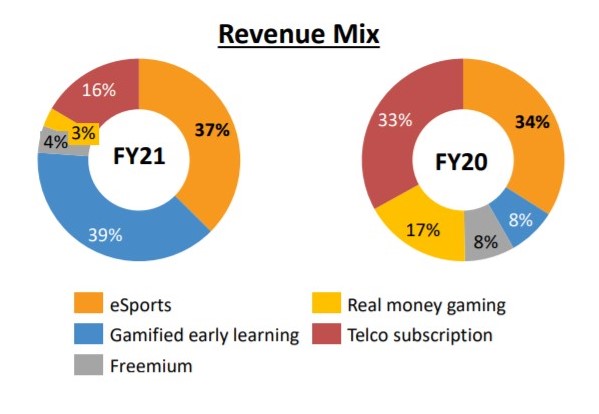

Below is segmental break up from DRHP.Looking at consolidated financials doesnt make sense because of acquisitions

RISKS

- Real money games are subject to regulatory risks

- eSports business revenues gets most of its revenues from a few customers and a few games. If some other game gets banned like PUBG did then it can effect revenues

- CAC may go up for Kiddopia due to Apples privacy update. This is a key monitorable and one will have to see how the company fairs in coming quarters

- Highly competitive industry with low barriers to entry

THE FRIENDS OF NAZARA network and some thoughts . Gaming is not a winner-take-all business. Every game has a shelf life.Its Best to look at games as movies. An investment in Nazara is essentially a bet on the management being able to capture the opportunities that this fast moving industry presents. Thats finding good acquisition targets and then scaling them like they have done so far. Their various segments - world cup cricket, kiddopia,halaplay,nodwin gaming,sportskeeda have all been acquired in the last 2-4 years. Nazara has a majority stake in all of them but the day to day operations are still run by the original founders of these firms.Now typically you might see this as a bad thing but gaming is a very dynamic and fast moving world where you can get disrupted faster than you can think. A game is popular today and tomorrow its gone. So the idea is to spread your risks by diversifying. This is what the company calls FRIENDS OF NAZARA where they acquire a majority controlling stake in companies where the founders are still interested in running the business. (Companies acquired must have already a proven business model). For the founders of these acquired firms they see understand how nazara can help them scale up their business which is something the management has demonstrated. Plus they too realise how risky gaming is and are happy to take a stake in nazara instead.That way even they de-risk their portfolio. And while doing all of this Nazara will avoid cash burn which is how they have operated so far

Now Real money skill gaming is where the money is in the near term but in the long term this kind of growth has a ceiling.This segment is not inclusive. What I mean by that is not everyone wants to do real money gaming. Plus in my opinion its more fun watching someone play a cricket simulation game than watch someone play rummy, teen patti or fantasy sports. As the Indian market matures you will see IAP model dominating and advertising taking a backseat just like it is globally. When game publishers see that money flowing, they will want to promote their own games via esports.OTT platforms will want the media rights due to increased viewership and just like Ipl, these rights will keep getting more expensive. If this actually plays out them it could be huge for Nazara.

If you wanna value NAzara it cant be a multiple of earnings or EBIDTA because they have clearly stated that they will plough back whatever they make into the business while staying EBDITA positive. In my opinion its best to look at Ev/Sales

Disc: 1% of holding (Will keep adding at regular intervals)