This is where the tri-party agreement between GMDC,GUJARAT FLUORCHEMICALS & NAVIN FLUORINE will matter.

5 Likes

3 Likes

(Broker’s Call: Navin Fluorine (Buy) - The Hindu BusinessLine)

Disc: Invested

Navin Fluorine Concall Q3-FY23

-

For Q3 revenue surpassed 500cr and EBITDA margins improved significantly due to ramp up and commercial production

-

Depreciation increased due to commercialisation of plants which impacted the PBT of company

-

MPP and dedicated plant for agrochem intermediates started in the quarter and co started supplies of commercial products post successful commissioning and qualification

-

Successfully completed plant audits by 4 MNC customers;

-

New plant in Dahej achieved close to designed capacity as operational efficiency in December; the new project in Surat will start commercial production in Q2-FY24

-

CDMO represented remarkable performance with YoY growth of 73%; cGMP-3 expansion is on track; CDMO is further ready for expansion and plan is currently under preparation

-

Honeywell HFO molecule has a wide range of applications; this is an independent molecule that has got multiple applications. Co is working on the molecule independently and this molecule is currently at very early stage and it will grow significantly and co will gain market share from other HFC

-

Currently commissioned first line of MPP with molecule and in Q4 there will be 2 more molecules going live; dedicated plants is commercialised 1 month prior to the target, from Jan reached at full capacity utilisation for the dedicated plant

-

CDMO will remain lumpy on a QoQ basis and one should look at it on a YoY basis. In CY2022 there was relatively soft demand; in CY23 there will be strong demand; Q4 will be better than Q3-FY23.

-

In HFO and agrochem dedicated plant company achieved close to full capacity; and will be the same at full capacity in Q4

-

Co started working on the debottlenecking of dedicated plants as well; it will be done in next 2 qtrs and will increase the capacity by 20% and then will speak with customer for extra capacity if needed co will do more capex which will take 1 year and will double the capacity

-

Trying to reduce the dependency on the generic pharma companies

-

Pricing for CY23 will be similar to pricing decided with Honeywell in CY2022 but company is seeing some softening the price of RM now

-

Out of the 4 customer for plant audits 1 is existing customer and 3 are new customers; 2 out of it are from performance material side.

-

In H2-CY23 company might see some softening in demand due to recession and macro events and some inventory buildup in agrochem in Brazil due to draught last year; but mid term trajectory is strong

-

Current run rate of Q3 EBITDA is sustainable in future on an annualised basis; as newer projects start getting commercialised the margins would further increase. Overall margins will increase at consol level to 30% from 25% currently as new projects’ portion in total revenue will increase further.

-

By FY24 mgt hope to take 3 big new projects to the board; out of these 3 projects one will be HF another will be CDMO i.e, cGMP 4 and one will be in speciality with 200 cr+ capex for each project.

-

Currently segment mix is 60% agro; 20% pharma and 20% industrial; performance material is very small. This will move to 1/3rd to agro and ⅓rd to performance material and remaining ⅓ from pharma and industrials.

-

On CDMO for CY23 company will be able to achieve $10-12 mn qtrly run rate but it will be lumpy on qtrly basis but will be achieved annualised basis

-

cGMP-4 will be significantly larger investment than cGMP-3.

Disc: same as before. Old holding. No buys or sells in last 30 days.

12 Likes

e0e9f235-8c68-4d46-8016-b36338cf2fd3 (1).pdf (1.3 MB)

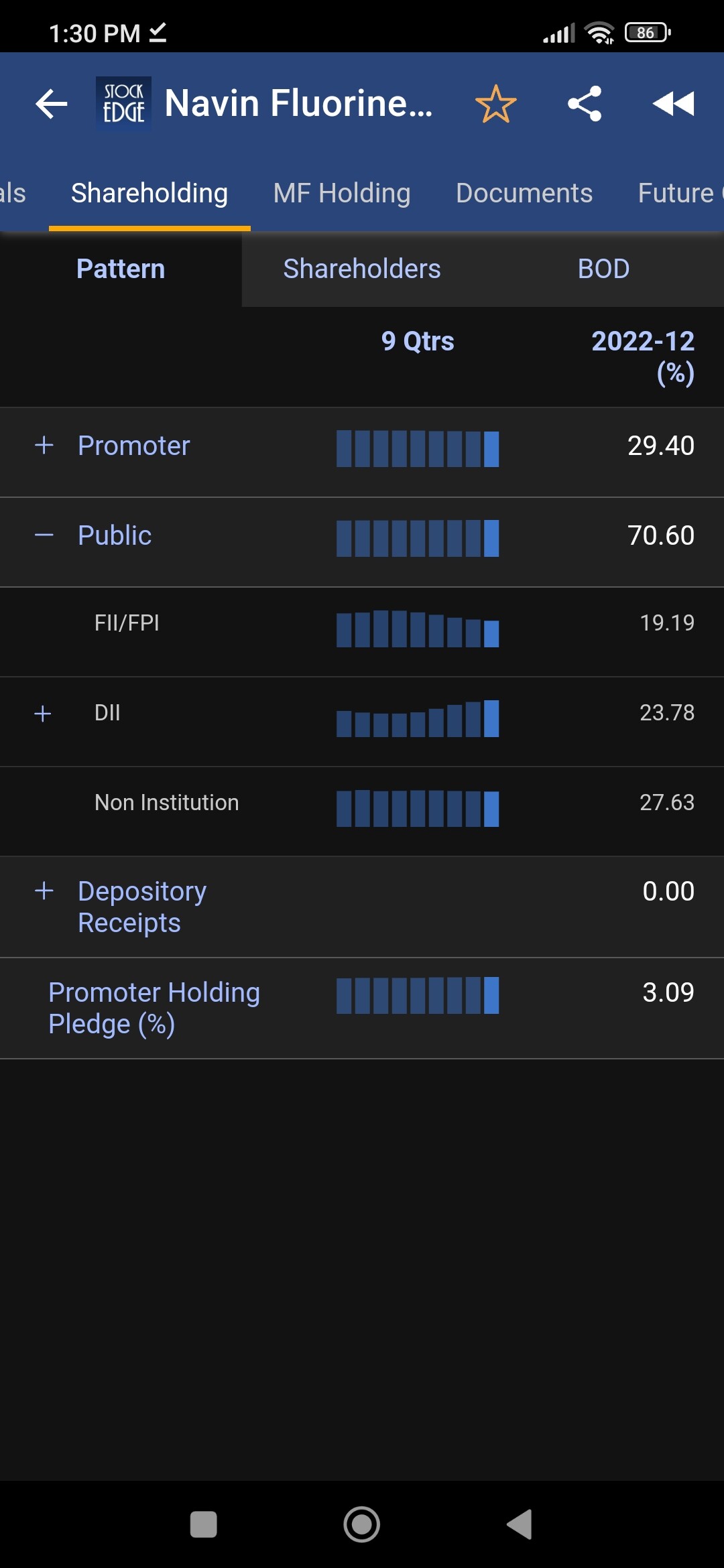

Now the promoter holding has gone down to almost 28.

So is this a precursor before a stock split or bonus?

I know that this will not increase promoter sharholding but atleast will increase value since last split from 10 to 2 , brought down prices from 3000 to 600 and niw it is again to 4000.

First time Thesis fully reflected in Numbers

I Attended the call live, seems there will be another 1000+ crore capex over the next 2 years

NAVIN CONCALL NOTES (SOIC)

-FY23: Revenues first time crossed 2000 crores and EBITDA crossed 550 crores. EBITDA has more than doubled YOY. EBITDA Margins at 28.9%.

-R32 capex will be commissioned as per schedule. Q2FY24, sales will start. Adding one more new molecule in MPP.

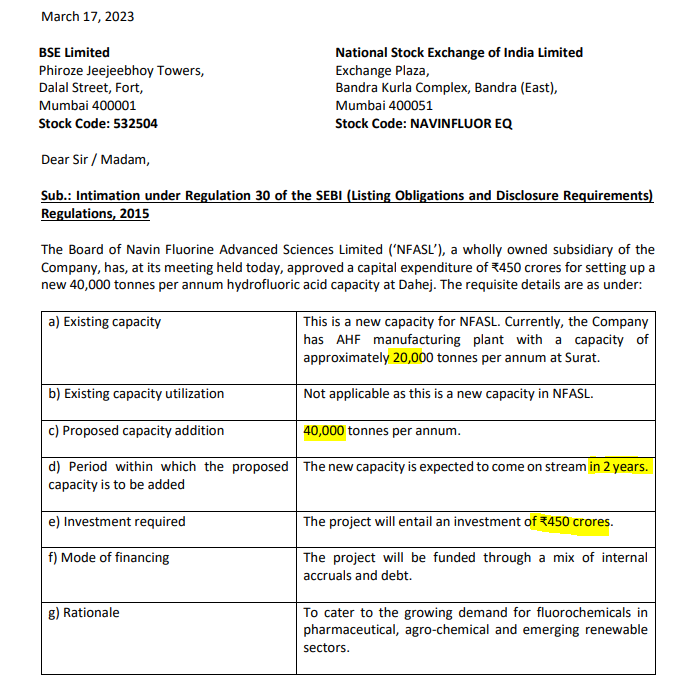

-Navin Advanced Life sciences:- 40,000 MTPA HF being set up for more than 400 crores.

-2 more new projects will be given to the board for approval. CGMP4 & one new project in Speciality Chemicals.

-Not seeing any impact on pricing of agrochemicals, as most of our business is contracted. As we are working with innovators on patented molecules. Have seen some impact, for the rest of the year- Will see some impact on one molecule. Maximum impact was felt in Q4FY23. Have developed other molecules which has ensured no slowdown is seen.

-Took a decision to reduce the chemical business for Generic pharma.

-Working on debottlenecking the Honeywell contract, and will increase capacity by 20%. Working on new molecules identified by Honeywell.

-Getting very good traction with our key accounts in CDMO. Getting opportunities outside of Fluorination. Have added one new customer. CGMP4 will be significantly larger than cGMP 1,2 or 3.

-Other expenses have gone up due to 2 one off charges: consultancy charge (5crore) & another one time 10crore charge.

-Outlook FY24: No change in Guidance as we haven’t been impacted by any over inventorisation in agro. Q1- Sequentially you will see some drop, because the HPP plant in DAHEJ was shut for a month. 1 more line of HF was shut in Surat.

-R32: there is a lot of interest to buy R32 on a long term Basis. Demand will increase as it will be used as HFC & HFO blend. Pricing for R32 will remain strong.

-Not many companies are adding capacity in R32. Demand is strong and only a few players are adding capacity. For quite a few years there will be demand for R32 as a HFC blend and HFO blend. No one can add capacities for R32 post December.

-In Q4- achieved optimal capacity fairly quickly. There is still capacity headroom available in the Quarters to come. Will get close to the full capacity utilization. Debottlenecking will come into play next FY. For HPP- Honeywell contract.

-Annualized margins will keep improving. We can’t comment on a QOQ basis.

-On ref gasses and Inorganic Revenue was flat.

-Extremely confident of growth in CDMO in FY24 and coming years.

-Maximum impact of Esop charges will be seen in the first 2 years, and in the third and fourth year. It will end up going down.

-In MPP: produced 3 molecules and supplied. In total there are 5 such molecules (4 agro, 1 pharma). Identified one more new molecule for a new customer.

-Working capital: will bring it down over a period of time.

Disc: No reco to buy or sell.

[/quote]

15 Likes

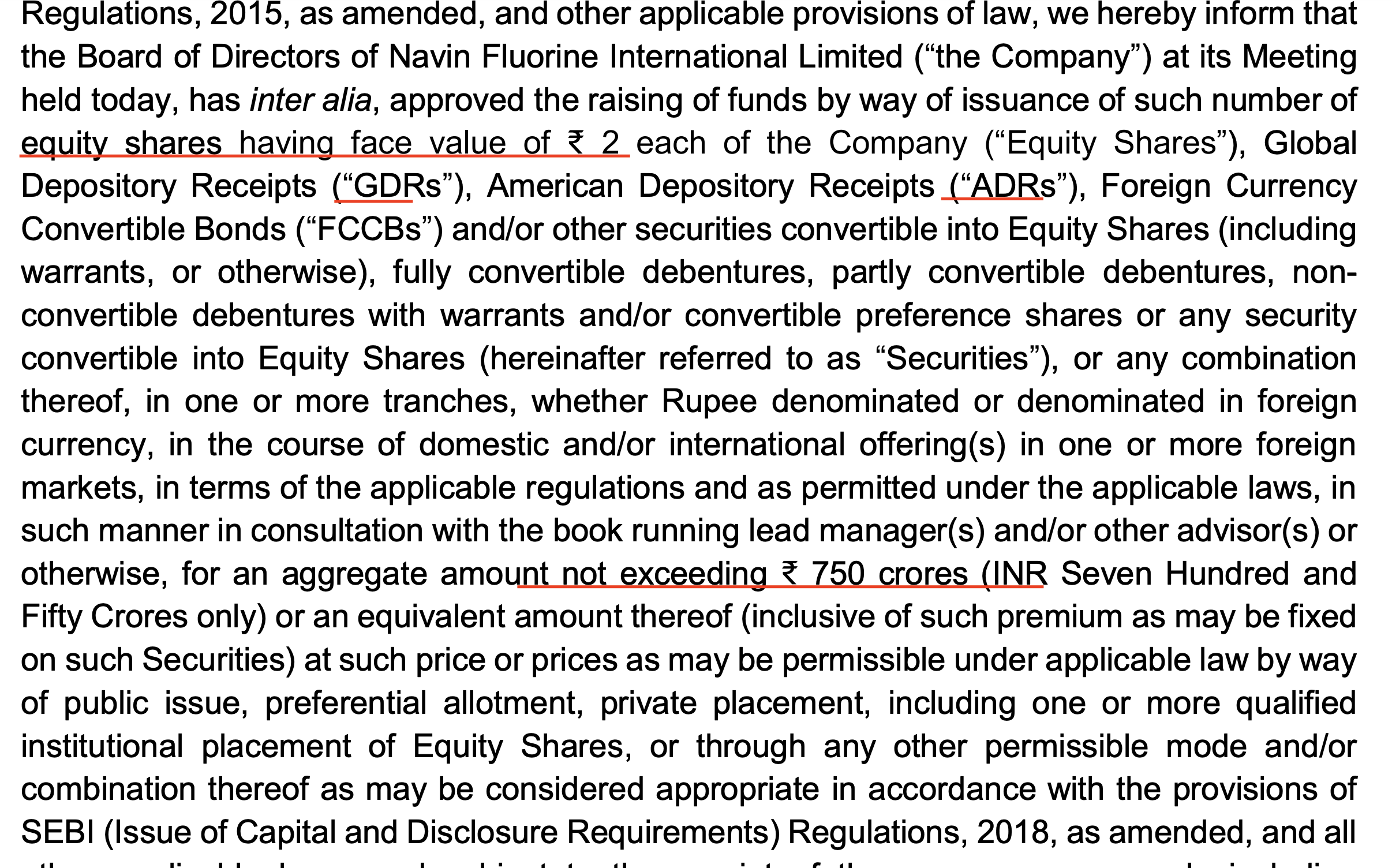

Navin is raising 750 cr by issuing shares.

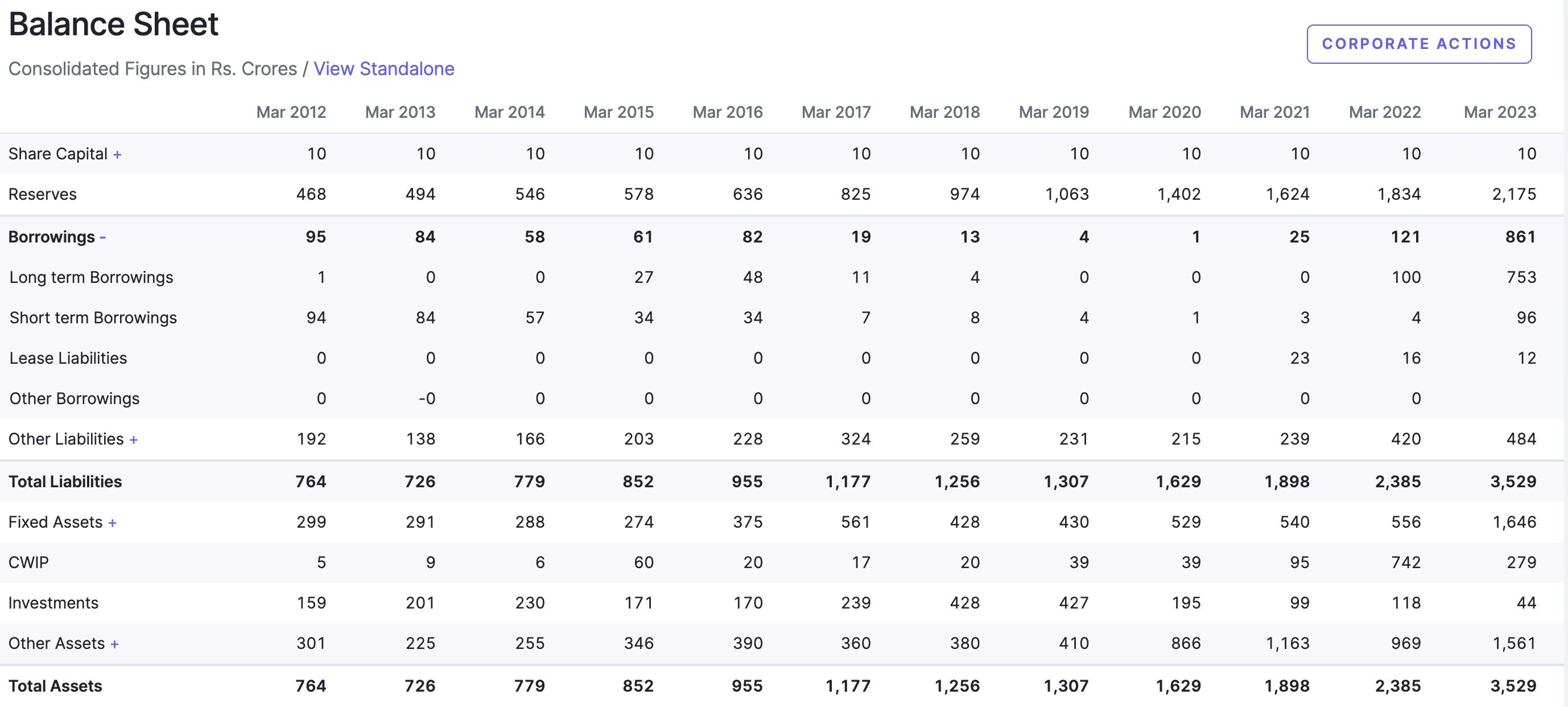

They have not diluted their equity in last 10 years (may be more but screener shows only 10 years). Despite record profitability in FY23 and huge ongoing capacity expansion, they are feeling a need to raise money through equity.

May be they want to reduce their borrowing which has shoot up in FY23. Or may be they are seeing huge opportunities and getting ready to address for them … time will tell.

6 Likes

Is this the reason for todays fall ? Stock 13% down.

3 Likes

Probably. And the session opened just 30 minutes ago, price may come back some by end of the session, or may fall more.

Investors of this forum, who follow businesses, do not react to tweets or other posts of social networking sites, unless the information has an impact on the business. And news like this is not uncommon, and will be notified to the exchanges by the company.

Have a trading position, SL got hit.

5 Likes

3 Likes

I was going through the Q2 concall and it really gave very negative impressions to me. The CFO and CEO kept saying one standard phrase “we cannot give forward looking guidance, we do not know how it will pan out, we do not know how much would be the demand from customers”.

One can understand that the business is such that you cannot earn regular fixed revenue contracts but being the KMP running the show, you must be having fair idea of what can be the trajectory, the expected pick-up or consolidation in business!

They looked very defensive and appeared to be in no mood to make the interaction fruitful. Infact they did not talk about numbers at all! All they said was, at best, generic vague statements!

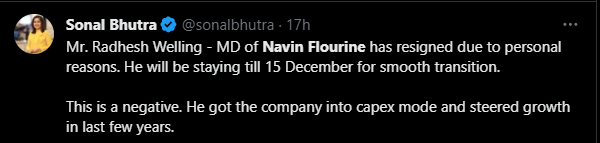

Radhesh Welling has resigned, Promoter holding is at 28%, No guidance/ affirmation from Management in the concall and a clear expression of not meeting the FY24 revenue guidance!! I know chemical space is in trouble at the moment, but the Management can soothe some nerves on the concalls, which was not the case here!

I would be really happy if someone from the forum can also share their views on the concall. Maybe I took some of the comments, the other way!! (Who knows)

Disclosure: Invested around current price. No buy/ sell recommendation.

2 Likes

Navin Fluorine Q1 FY25 Analysis: Key takeaways!!

Navin Fluorine International Limited demonstrated resilience in Q1 FY25, achieving 7% year-on-year revenue growth despite challenging market conditions. The company’s performance was supported by stable operations in its High-Performance Products (HPP) segment and strong sales from new R32 capacity. However, the Specialty Chemicals segment faced headwinds due to inventory rationalization by global agrochemical majors.

Strategic Initiatives:

- Capacity Expansions: NFIL is progressing with several expansion projects, including a Rs. 540 crore agro-specialty project set to commence commercial production by September 2024.

- R&D Focus: The company has established a new R&D center in Surat to strengthen its product pipeline and develop new capabilities.

- CDMO Growth: NFIL is focusing on increasing the share of late-stage and commercial molecules in its Contract Development and Manufacturing Organization (CDMO) business.

- Diversification: The company is exploring opportunities in performance advanced materials, including co-development with global majors for sectors like semiconductors.

Trends and Themes:

- Shift towards India as a manufacturing hub due to the China+1 strategy

- Increasing focus on sustainable and environmentally friendly refrigerants

- Growing demand for fluorine-based agrochemicals and pharmaceuticals

Industry Tailwinds:

- Increasing adoption of new-generation refrigerants (HFOs)

- Rising demand for crop protection chemicals in emerging markets

- Growing pharmaceutical industry and increased outsourcing of drug manufacturing

Industry Headwinds:

- Inventory destocking by global agrochemical majors

- Pricing pressure from Chinese competitors in certain segments

- Volatility in raw material prices

Analyst Concerns and Management Response:

Concern: Decline in Specialty Chemicals revenue

Response: Management expects demand recovery in the second half of FY25 and is focusing on strengthening the product pipeline and developing new molecules.

Concern: Competitive pressure from Chinese manufacturers

Response: NFIL is focusing on long-term supply contracts with innovator companies and continuously working on improving efficiency and developing new routes of synthesis.

Competitive Landscape:

NFIL maintains a strong position in the fluorochemicals market, particularly in India. The company faces competition from Chinese manufacturers in certain segments but differentiates itself through long-term partnerships with global innovators and a focus on high-value specialty chemicals.

Guidance and Outlook:

Specific numerical guidance was not provided, management expects:

- Improvement in the second half of FY25

- CDMO business to reach $100 million revenue by FY27

- Peak revenue from the Rs. 540 crore agro-specialty project by FY27

Capital Allocation Strategy:

NFIL is focusing on:

- Organic growth through capacity expansions

- Investments in R&D and new capabilities

- Maintaining a strong balance sheet with a net debt to equity ratio of 0.38x

Opportunities & Risks:

Opportunities:

- Growing demand for new-generation refrigerants

- Expansion in CDMO business, particularly in late-stage molecules

- Potential in performance advanced materials for emerging sectors

Risks:

- Continued slowdown in agrochemical demand

- Pricing pressure from Chinese competitors

- Regulatory changes affecting fluorochemicals

Regulatory Environment:

The company is navigating various regulations, including:

- Phasedown of high-GWP refrigerants

- Increasing focus on environmental sustainability in chemical manufacturing

- Regulatory support for domestic manufacturing through initiatives like PLI schemes

Customer Sentiment:

- Agrochemical customers are cautious, leading to inventory rationalization

- Pharmaceutical customers showing increased interest in outsourcing to India

- Growing demand for R32 refrigerant from domestic and export markets

Top 3 Takeaways:

- NFIL demonstrates resilience with 7% YoY revenue growth despite market challenges

- Strategic focus on capacity expansions and R&D to drive long-term growth

- CDMO business expected to reach $100 million revenue by FY27, supported by increasing share of late-stage molecules

3 Likes

Thoughts on NFIL and the Specialty Chemicals Sector?

The Specialty Chemicals segment is navigating a challenging landscape:

-

Agrochemical Destocking: While destocking seems to have eased, Chinese competition remains a significant concern, especially with their increased capacity and integration, threatening margins.

-

Global Innovator Strategy: Many global innovators are focusing on greater front-end integration and building more resilient value propositions to protect against competition from generic Chinese companies. NFIL is prioritizing staying in the supply chain of these innovators, even if it results in short-term EBITDA margin sacrifices, to ensure long-term profitability and relationships.

-

Management Outlook: Despite ongoing competition from China, the Specialty Chemicals division aims to ramp up production to gain operational leverage. The agro-specialty plant (Capex ₹5.4bn) is expected to be commissioned by October 2024, with a firm order covering 50% of its capacity. While pricing for the dedicated customer is fixed in the first year, non-dedicated volumes remain subject to price fluctuations.

What are your thoughts on NFIL’s strategy and the impact of Chinese competition on the Specialty Chemicals sector? How do you see the near-term margin pressures playing out?

3 Likes

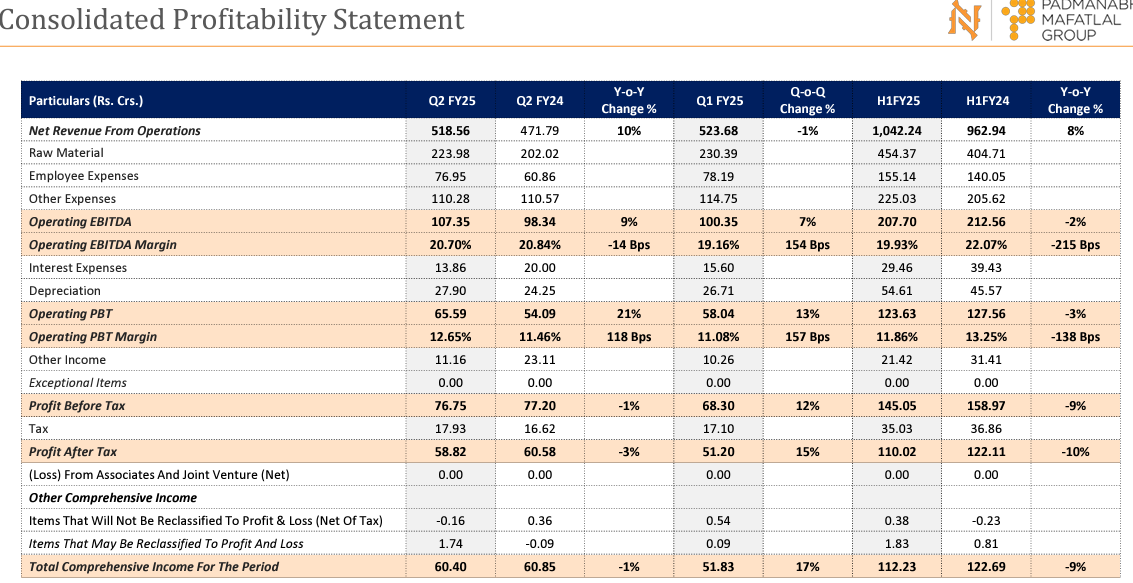

Overall, fair set of topline growth in Q2 FY25, driven by the HPP and CDMO segments. While consolidated profit after tax slightly declined, (lower other income, higher depreciation, tax) the company maintains a positive outlook, backed by a strong order book, ongoing capacity expansion projects, and a strategic focus on key growth drivers.

Posting the summary note from the investor presentation here.

Navin Fluorine International Limited Q2 FY25 Performance Summary

Topline:

- Consolidated revenue from operations for Q2 FY25 was Rs. 518.56 crores, a 10% increase year-over-year (Y-o-Y).

- The Specialty CDMO segment saw a 10% Y-o-Y sales increase, reaching Rs. 518.6 crores.

- The HPP business vertical experienced a 23% Y-o-Y revenue growth, driven by increased R32 sales and better R22 realizations.

- Specialty Chemicals revenue decreased by 15% Y-o-Y due to cautious global demand and competitive pressure.

- The CDMO business vertical saw a 41% Y-o-Y revenue increase, driven by strategic actions including supplying a quantity for process performance qualification for a late-stage study for an EU major customer.5

Bottomline:

- Consolidated profit after tax for Q2 FY25 was Rs. 58.82 crores, representing a 3% decrease Y-o-Y.

- Operating EBITDA for Q2 FY25 was Rs. 107.35 crores, reflecting a 9% increase Y-o-Y.

- Operating EBITDA margin for Q2 FY25 was 20.70%, a decrease of 14 basis points (bps) Y-o-Y.

Other Trends:

- Strong order visibility for the Specialty Chemicals segment is expected for Q3 and Q4 FY25, extending into FY26, supported by the Surat and Dahej assets.

- The CDMO segment holds a strong order book position for H2 FY25.

- Navin Fluorine is making significant investments in capacity expansion projects

- AHF capex for Rs. 450 crore is on track for commissioning by the end of FY25 or early FY26.

- Additional R32 capacity with a capex of Rs. 84 crore is progressing as planned and should be operational by February 2025.

- cGMP4 capex of Rs. 288 crore is underway, with Phase 1 (Rs. 160 crore) expected to be commissioned by the end of Q3 FY26.

- The company maintains a consistent dividend performance history, with a focus on ESG targets.

- Navin Fluorine’s core business strategy emphasizes a high-demand product basket, strong customer partnerships, and being a dependable fluorochemical company.

- The company is focused on driving operational excellence, financial robustness, disciplined execution, revenue stream diversification, partnership strengthening, and the creation of scalable platforms.

Competitive edge stems from factors such as:

- A strong brand reputation, state-of-the-art facilities, and a focus on building scale.

- Backward integration, deep expertise in fluorine chemistry, and a comprehensive approach as an integrated fluorine provider.

- Credible certifications, a competent team, and a commitment to safety and sustainable practices.

- Proximity to logistical options and a long history of expertise in handling complex fluorine chemistries.

Disclaimer: Invested and Biased. Less than 3% of PF. No transactions in the last 30 days. Post purely for study purposes. Consult your advisor before any transactions.

3 Likes

Some interesting questions and management answers providing insights from the Navin Fluorine International Limited (NFIL) Q2 & H1 FY25 Earnings Call:

Specialty Chemicals - Improved Visibility

- Vive Rajani from Morgan Stanley asked what gave management confidence in the improved visibility for the second half of the year for the specialty chemicals business, given past deferrals.

- Nitin Kulkarni, MD, NFIL responded that they had entered into supply agreements with customers for many of their specialty molecules for both Q3 and Q4 of FY25 and the calendar year 2025. These agreements were based on the company’s existing capacity and were firm orders, not assumptions.

- Anish Ganatra, CFO NFIL, added that the visibility extended not only to Surat assets but also to the MPP and the dedicated agrochemical plant.

- Key Insight: NFIL has secured firm multi-year orders for its specialty chemicals business, providing greater revenue visibility and certainty compared to past quarters.

CDMO Business Trajectory

- Vive Rajani also asked for a sense of the expected trajectory for the CDMO business in the second half of FY25 and going into FY26, given the traction with European and US clients and the two new molecules.

- Mr. Ganatra responded that they anticipated at least flat growth in Q3 compared to the same period last year, but a very strong Q4, and even stronger growth going forward.

- Key Insight: While specific numbers were not provided, the management expressed strong optimism about the CDMO business growth, driven by large commercial molecules and continued customer acquisition efforts.

CDMO Capacity Concerns and Product Mix

- Sanjay Jen from ICICI Securities raised concerns about CDMO capacity to meet all the orders, given the multiple projects in the pipeline. He also asked if the company was de-emphasizing early-stage molecules.

- Mr. Ganatra clarified that they had planned the GMP4 project to meet the required capacity needs. He also explained that the company is not de-emphasizing early-stage molecules, but rather balancing the mix as commercial molecules start to take a larger share of the pie. The pie itself is growing, and the proportion of revenue from commercial molecules is expected to reach 60%.

- Key Insight: NFIL’s capacity expansion plans align with its order book and strategic focus on commercial molecules, which offer larger volumes and lower risk profiles. The company continues to engage with early-stage opportunities while prioritizing later-stage and commercial molecules.

Specialty Chemicals Domestic Revenue Growth

- Sanjay Jen also questioned the sharp improvement in domestic specialty chemical revenue, assuming NFIL was shifting its focus away from domestic pharma.

- Mr. Ganatra explained that the domestic revenue increase was partly opportunistic due to the current market scenario, and partly due to supplies to local customers on behalf of large global players. The core message remains a strong order book for both Surat and Dahej assets in Q3 and Q4, indicating continued focus on export-oriented specialty chemicals.

- Key Insight: While domestic revenue showed growth, NFIL’s primary focus for specialty chemicals remains on exports, with a strong order book for the second half of the year, driven by both new and older product portfolio recovery.

HPP Business Growth Drivers

- Sanjay Jen asked if it was fair to assume that growth in the high-performance product (HPP) business would be driven solely by pricing until new R22 capacity came online.

- Mr. Kulkarni clarified that growth would be driven by both pricing and volume growth, as they are adding R32 capacity expected to be completed in Q4 FY25.

- Key Insight: NFIL expects continued growth in its HPP business through a combination of pricing and volume increases. The upcoming R32 capacity expansion will further contribute to volume growth.

European CDMO Agreement Clarification

- Ankul Pal from Access Capital sought clarity on the order book visibility, specifically whether it was driven by new products for global innovators or a recovery in demand for older products.

- Mr. Ganatra explained that the visibility stemmed from new molecules introduced in the last 18 months, alongside some recovery in demand for older products.

- Key Insight: NFIL’s order book strength for specialty chemicals comes from both recent product launches and a rebound in demand for existing products, indicating a healthy mix of innovation and market recovery.

Margin Improvement Drivers

- Ankul Pal further inquired about the drivers for achieving the targeted 25% margin, asking whether it would be primarily due to product mix shift or pricing.

- Mr. Ganatra said it would be a combination of factors, highlighting their focus on getting there sustainably.

- Key Insight: NFIL aims to achieve its 25% margin target through a combination of strategic initiatives, including product mix optimization, operational efficiencies, and pricing, while ensuring sustainable growth and profitability.

Management tone shows confidence in company’s growth trajectory across all business segments. Notably, the focus on securing multi-year orders, expanding capacities, and driving innovation positions NFIL favorably for long-term success.

Disclaimer: Invested and Biased. Less than 3% of PF. No transactions in the last 30 days. Post purely for study purposes. Consult your advisor before any investment decisions.

6 Likes