Q2 Investor presentation: https://www.bseindia.com/xml-data/corpfiling/AttachLive/a92a059f-4763-4e3b-bd8f-cb1d47cd760c.pdf

The slide below was interesting:

Q2 Investor presentation: https://www.bseindia.com/xml-data/corpfiling/AttachLive/a92a059f-4763-4e3b-bd8f-cb1d47cd760c.pdf

The slide below was interesting:

I think they are reporting it since Oct 2020 Investor updates, good to see they will be largely sticking to the Q4 FY22 completion time line.

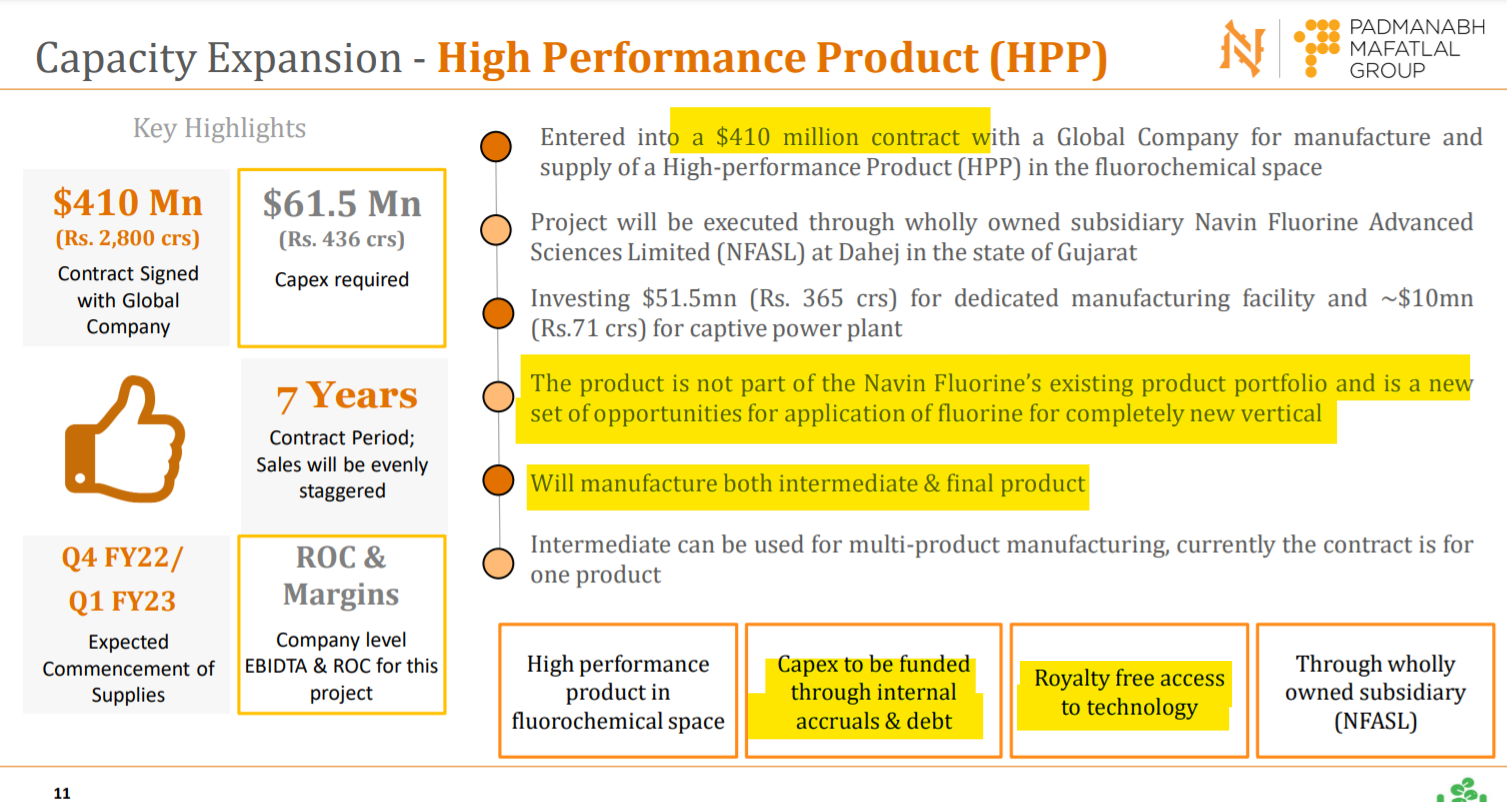

Another Long Term Contract

In Line with my thoughts in the July Post, there are several growth triggers at play here:

In the next 4 quarters we will see the addition of 500crores+ to the netblock. 195crores in MPP+365 crores for HPP and 70 crores in the power plant.

cGMP 3 will be up for debottlenecking in the next 6months and post that there is a real possibility of the addition of cGMP 4 given the quarterly run rate is becoming stable and project flow is increasing.(Management hinted in the call)

Likely Capex announcement for newer applications like Electric Vehicles, Semiconductor,5G, etc in the next 24 months.

High Probability of those 5 molecules for which MPP is being set up to move into Dedicated plants in the next 2-3 years.

Further development of the HPP segment and opportunities in the intermediate space.

Likely CAPEX announcement which will be relatively large in size in new age ref gas.

Another long term agreement. I do think this is at a superior juncture when compared to Pi Industries, which is currently going through the struggle of establishing the Pharma vertical. Navin is already there in Pharma Crams, Pharma intermediates for generic, Agro intermediates and other fine chemicals including the HPP.

Disc: continue to remain invested in line with our thesis.

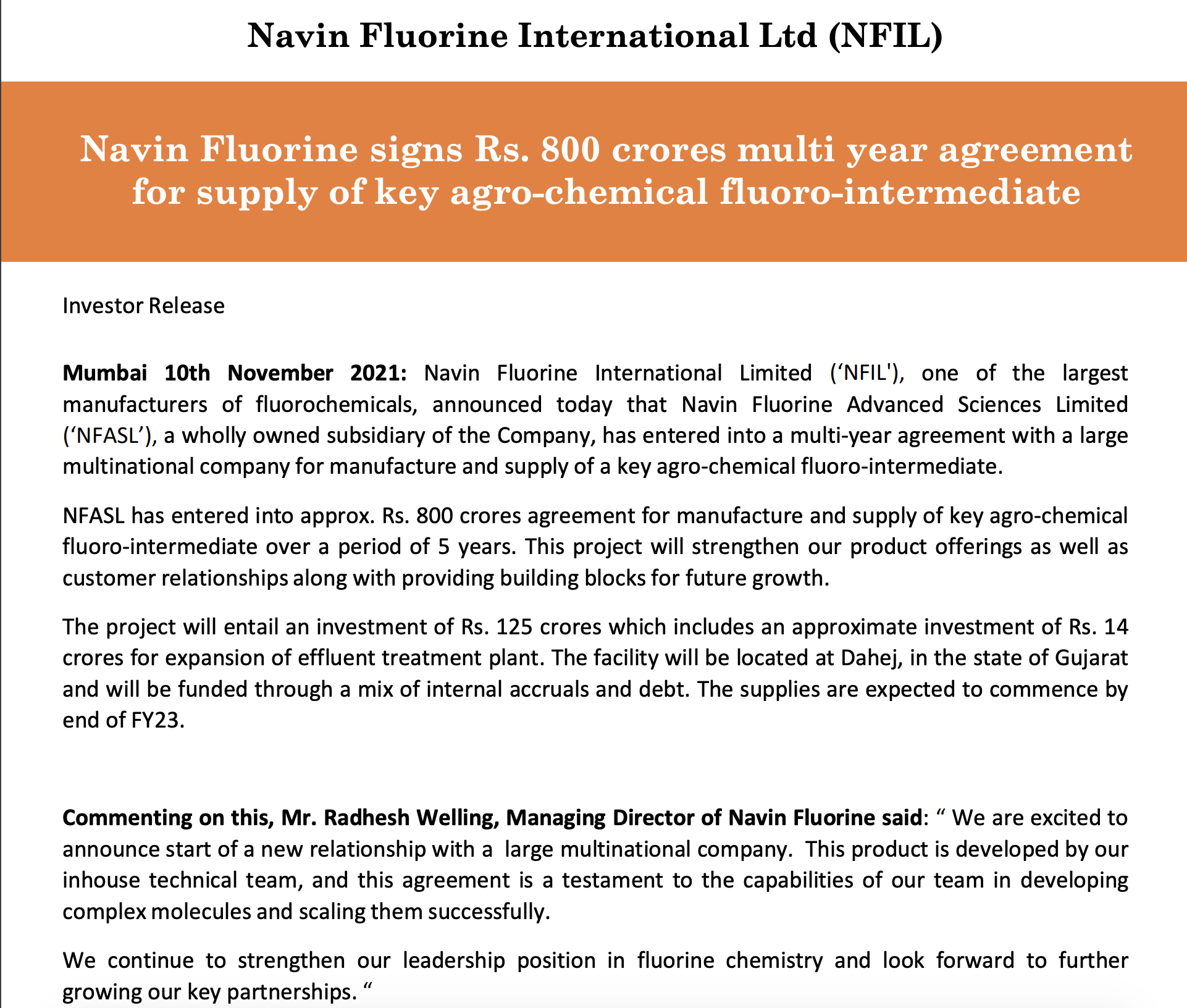

Business udpate call:- Regarding the contract

Navin Fluorine International (NFIL)-Key Takeaways of the Business Update Call-11th November,2021

#NFASL has entered into ~Rs. 8 bn agreement for manufacture and supply of a key agro-chemical fluoro-intermediate over a period of 5 years.

#The project will entail an investment of Rs. 1.25 bn which includes an approximate investment of Rs. 140 mn for expansion of effluent treatment plant. The facility will be located at Dahej, in the state of Gujarat and will be funded through a mix of internal accruals and debt. The supplies are expected to commence by end of FY23.

#The facility will be based out of Dahej and will share certain common infrastructure with the HPP and MPP plants.

#Product development and scale up has been developed in-house-R&D/T&D teams. NFIL does not supply to the competition of the client as a principle even after 5-7 years.

#Demand from end user industries of pharma and agrochemicals continues to be robust. NFIL is also seeing good demand coming from the industrials segment however this is yet to reach a sizeable level.

Investor Presentation – November 2021

When valuations are high, one should have the ability to predict growth triggers beyond the other market participants to retain the conviction for the story. Lets see the upcoming growth triggers in continuation with posts on Navin for the last entire year on this thread.

Growth triggers:-

365 crore capex for HPP segment is going live in Q4 of this year with 71 crores of investment for Power plant. Entire capex will give 400 crore types of sales with 26-28% Ebitda margins.

195 Crore capex for MPP plant going live by Q2 of FY23. This will lead to sales of 260-280 crores. At a similar margin profile for the company. This MPP will initially have 5-7 molecules. Many of these in agro can get commercialised in dedicated blocks as the volumes scale up.

Dedicated contract capex of 125 crores, which will sales of 160 crores per annum. This will go live by Q4FY23.

There are 20-25 Molecules in the Pipeline in the spechem division out of which 15 are qualified opportunities. These will start getting commercialized over this and next fiscal. Can result in more capex. Source FY21Q3Concall.

Debottle-necking of cGMP 3, approval likely by the end of this fiscal. Secondly, cGMP 4 capex to be announced next financial year. In total Navin has approval to set up 6 cGMPs for the CRAMS Business.

Navin is one of the only companies in Western Asia to have the capability for HexaFluoro Platform that they acquired from the JV with Piramal. Already in talks with a European co for commercial applications. This platform is largely used in pharma (inhalers/Inhalation anesthetics).

Company is first time looking to raise debt to finance upcoming capex opportunities in the next few years. This is the biggest signal for me, that tailwinds that the co is witnessing are getting stronger. Those who have tracked the company, know how conservative the management is. Indication of raising debt to finance capex really points to the longer term growth aspirations.

Large size capex for new age ref gas is also likely to be announced. Moreover, for newer applications in the area of 5g and EV’s the co is setting up a R&D centre in Mumbai. This is what they had to say in a recent management interaction:-

“Navin is working on 2 Lithium Based molecules on Hexafluoride chemistry. One of the molecule is in collaboration with a French Company. The molecule is manufactured through Organic route and is touted to replace Lithium.”

Navin vs Pi

That’s a question I have often asked myself in last 2.5-3 years of owning both the positions. Pi has been facing severe challenges of scaling up the Pharma vertical. We have been hearing about the pharma foray since 2014. Acquiring a pharma asset and just getting it CDMO ready itself will likely take more than 5 years. No other CDMO co in Pharma has been able to scale up the business in less than 5 years.

Navin on the other hand has been through the gestation in pharma cdmo of nearly a decade after acquiring MOL, and still has approval to set up 3 more cGMPs. Moreover, many agro CRAMS opportunities are fructifying for the co, another indicator is that they might change the name of spechem business to Contract Manufacturing services.

Most importantly, both growth and ROCE profile coupled with base effect is in favour of Navin over Pi Industries.

Disc:- Just wanted to post my views for my own benefit and everyone else’s benefit. I own the stock. Not sebi registered, and no transactions in last 30 days.

Coming to the negatives:-

Valuations are stretched. No second doubt about this. One has to see how they think about what the correct valuation for this business is.

Senior Management churn with the cfo who was long associated with the co leaving.

Significant capex plan and its implementation. Let’s see how they execute, as they have never implemented such large capex’s together in the past.

Management bandwith is an issue in the real world. Let’s see how they tackle this.

HONEYWELL PARTNERS WITH NAVIN FLUORINE TO ADD HYDROFLUOROOLEFINS (HFO) MANUFACTURING CAPACITY IN INDIA (Earlier announced in Feb’20 but client name revealed today)

One of the probable triggers, announcement being made.

Approval is here for cGMP 3 debottlenecking:-

@Dr.Midhun @Worldlywiseinvestors @harsh.beria93 @Dev_S @Chins @phreakv6

https://pubs.acs.org/doi/10.1021/acsomega.0c00830

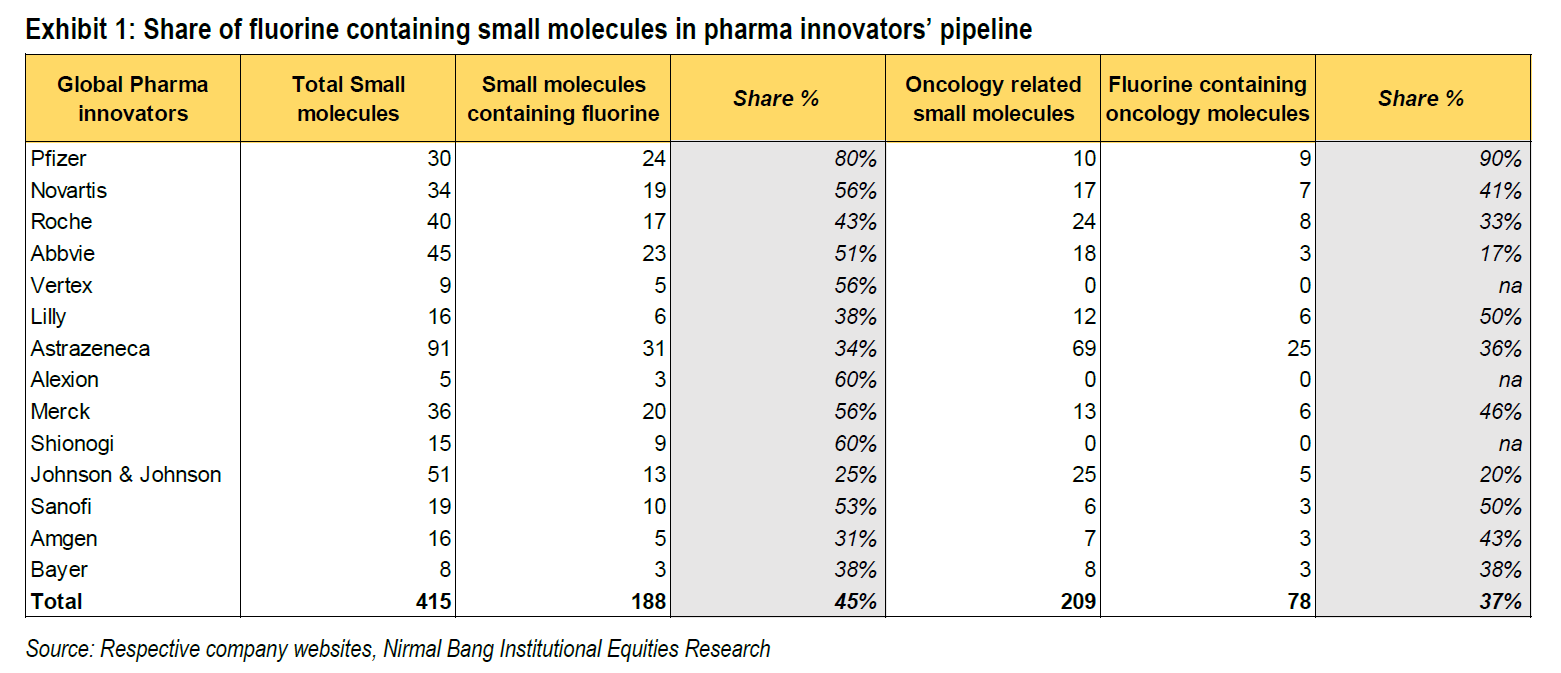

From the above report it is evident that the usage of Fluorine is increasing in Pharma. Could someone explain in simple terms (a layman can understand) what is this means ?

The value chain of any drug is KSM - Key Starting Material - > Intermediates → API → Formulation

In this value chain where exactly Fluorine fits in ? Whatever little reading I have done so far, my understanding is Fluorine is used in small molecule (link to understand what is this )

Found Some answers here

Many Thanks

Good report on Fluorination along with Navin & SRF

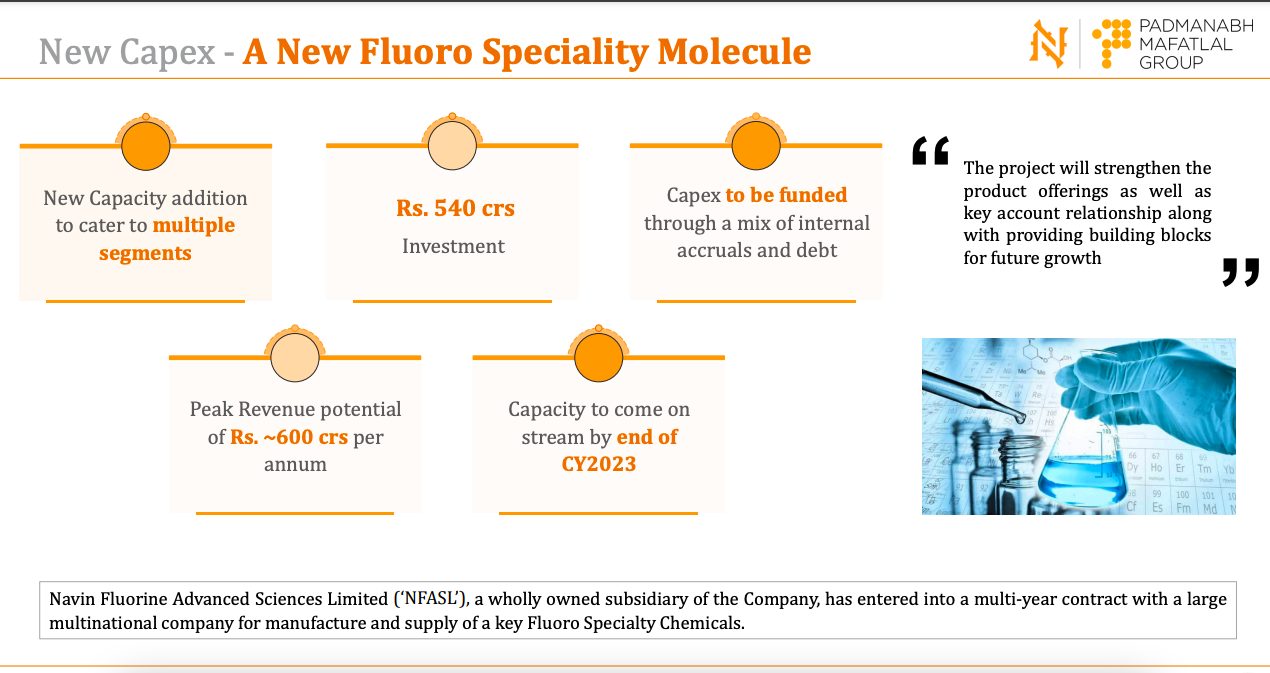

I have been tracking capex guidance of Navin very granularly, another huge development this Quarter

Another 540 crore capex announced for a dedicated capacity

With all capex projections ( hpp+ mpp+ Agro chemical intermediate+ New flouro specialty molecule ) and subsequent asset turns they can double their top line in 2 years.

Hpp : 2800 over 7 yrs = 400 cr/Annum

Mpp : 250 cr/ annum

Agro intermediate new contract : 800 cr over 5 yrs = 150 cr approx/ annum

New specialty molecule : 600 cr/ annum

Total new revenue proj in FY 24 : 1400 cr.

FY22 Revenue : 1400 cr.

New businesses must be higher margin profile compared to legacy businesses.

Disc : Invested

Hi @Midhunjoe - directionally the calculation is straight however I have reservations on timelines. This new specially has potential run rate of 600 Crs/year at peak utilization. This has been announced just recently. Production commencement is expected by Q4’24. Will need another ~2 Years post commencement to reach peak utilization.

Nevertheless, positive direction. Just that we need to keep the timelines realistic.

Thanks,

Tarun

Just to add crams Debottlenecking of 70 crores which can lead to 200 crore topline. Debottlenecking in FY23 too

Calculate the project level margins.

540 crore fixed assets

200 crores working capital

740 crore capital deployed

According to Management, significantly higher Roce and margins Vs 3 projects. Which have Roce of 24%

Thus, assuming 30% Roce

222 crore of Additional Ebit and Roce of 30% + Margins close to 40%.

Just some rough math

Very comprehensive Annual Report. Resonates strong business undercurrent. Some key readouts:

Capex:

R&D:

Others:

Disc: No investment as on date

Regards,

Tarun

FY 2022-23 looks to be interesting year wherein new facilities will be commissioned and growth trajectory will be get heads up… If they are able to maintain the current margarine then it should do well in medium term

More on hydrofluoroolefins| The end molecule Navin is manufacturing for Honeywell

The global hydrofluoroolefins (HFOs) market is expected to grow at a CAGR of 20.8% during 2017 – 2023 to reach USD 5,784.3 Million by 2023. Factors propelling the growth of HFOs market include exceptionally low GWP compared with HFCs and HCFCs, few facility modifications required to transition from HCFCs, EU regulations phasing out HFO from other fluorinated greenhouse gases, and low to mild flammability.

The increasing use of HFO in refrigeration, mobile air conditioning and foam are attracting the investors to generate business from HFO market. Moreover, environmental issues have made these industries to transit from HCFC to HFO. The companies are now taking lead in manufacturing HFO grades. Industry pioneers have patented HFO and markets them under a brand for instance Honeywell markets HFO under the name of Solstice and Arkema markets HFO as Forane. On the consumer side HFOs are being blended with hydrocarbons and water in order to reduce the incremental operating cost.

It seems HFO is replacing HCFs and HFCs+Other ref gases. Worth a deeper inspection for those invested in fluorine companies

Hydrofluoroolefins (HFOs), a low GWP Solution to F-Gases,.

Disclosure:- continue to remain invested.