I think Navin Flourine International deserves some research. I first noted this company in 2011 when it’s dividend yield was quite high on common screening websites (due to special dividend). I made a small investment and found that carbon credits were a good source of revenue. Since then, the stock has gone up like 3x and currently trading around 950 levels.

Last few important developments:

a) Acquisition of Manchester Organics UK (2011)

b) CRAMS business (2011)

c) 120 Crore JV with Piramal Enterprises at Dahej (Specialty Flourochemicals focussed on healthcare. Navin has 49%)

As of now, CRAMS contributes just 6% revenue on standalone, Refrigerants-36%, Specialty chemicals - 39%. Inorganic Flourides -19%. (All this in latest presentation)

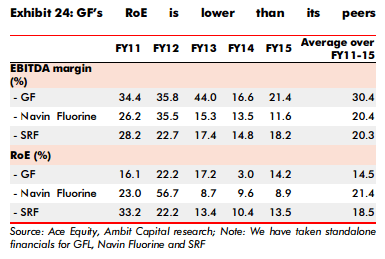

Some data from latest Ambit report (17-June-15) which analyzed Gujrat Flourine in report titled inox power

One of my concerns has been - low ROE inspite of generous dividends. But I believe this company deserves a closer inspection. Institutional investors like DSP Microcap Fund, Atyant Capital, hold some shares (above 2%)

Highlights of the Concall by Capital Mkt

Net revenues rose 16% to Rs 150 crore for Q1FY’16 on a YoY basis while EBITDA increased 117% to Rs 26 crore and PAT jumped 113% to Rs 18 crore.EBITDA margin of the company improved to 17% in Q1FY’16 from 9% in Q1FY’15 mainly on account of operating leverage.Revenue growth across business units was driven by higher volumes and better realizations

Refrigerants revenue increased 22% on a YoY basis in Q1FY’16 to Rs 61 crore and 24% on a QoQ basis. Domestic revenues were 59% while exports were 41%.Inorganic fluorides revenue decreased 8% on a YoY basis in Q1FY’16 to Rs 24 crore and 4% on a QoQ basis. Domestic revenues were 87% while exports were13%.Speciality chemicals revenue increased 22% on a YoY basis in Q1FY’16 to Rs 55 crore but decreased 4% on a QoQ basis. Domestic revenues were 55% while exports were45%.

CRAMS revenue decreased 8% on a YoY basis in Q1FY’16 to Rs 10 crore but decreased 38% on a QoQ basis. This segment has only export revenues.Greenfield Facility at Dahej, Gujarat, a joint venture project at Dahej with Piramal Enterprises to develop, manufacture and sell speciality Fluorochemicals for healthcare segment is expected to come on-stream by H2FY16 with an investments of around Rs.140 croreDemand for refrigerant has surged substantially leading to improved realizations. Increasing usage of R22 in pharmaceutical companies and agro chemical companies as feed stock is also augmenting demand. Overseas demand for R22 has remained stable.

Speciality chemicals continued its good growth in both domestic and overseas market.Inorganic chemicals growth was flat during the quarter as this BU was impacted by the weak domestic steel industry. However the company is now targeting exports market.CRAMS business has performed in line with expectations with clear visibility of the order book supporting its growth

Capex completed for manufacturing facility for multi ton batch size for CRAMS business unit at Devas at an investment of Rs. 60 crore .New facilities will be India’s only plant with high pressure fluorination and cGMP complaint capabilities. Customer audit for the business is under way and it is getting a positive response.Benefits of capex at devas would be seen at later part of the year.

Today , Vanderbilt University bought 120,000 shares from Atyant fund @1892. Seems, Vanderbilt has its first investment in India and highly involved on Medical research.

Surprised that this company has not got the attention it deserves yet. The management has shown superior capital allocation skills and is increasingly focusing on the crams and spec chem business. No incremental capex is being done in r22 refrigerants business which is expected to act as a cash cow for the next few years. The cash would be reinvested in high roce crams business. With agrochemicals cycle turning around the only headwind I see is the flourspar prices currently

Attention from where? Stock price has moved very fast in last 4 years its almost 10-15X from jan 2014, its only the last 1 year the stock price is consolidating, which is expected

Revenue grew by 6 % to Rs 226 Cr compare to 212 Cr in Q3FY18

EBITDA grew by 2 % to 52.4 Cr compare to 51.5 Cr in Q3FY18

EBITDA margin stood at 23.2 % for the quarter

PBT grew by 2 % to 45.9 Cr from 45.1 Cr in Q3FY18.

PBT margin stood at 20.3 % for the quarter

Refrigerant Segment

Gas business revenue grew by 8 % to 57 Cr from 53 Cr Q3FY18

Inorganic business Segment

Revenue grew by 24 % to 47 Cr compare to 38 Cr in Q3FY18

Specialty Chemical Business

Revenue grew by more than 40 % in Q3FY19 to 73 Cr as compare to 56 Cr in Q3FY18.

Crams Business

Revenue stood at 49 Cr compare to 64 Cr last year same quarter

Nine Month FY19

Revenue grew by 17 % to 711 Cr compare to 609 Cr in Q3FY18.

EBITDA grew by 8 % to 153.8 Cr compare to 165.9 Cr in nine month FY19.

EBITDA margin stood at 23.3 %.

PBT grew by 9 % to 146.4 Cr from 134.5 Cr in nine month DY18.

PBT margin stood at 20.6 %.

Refrigerant Segment

Revenue grew by 12 % to 197 Cr compare to 175 Cr last year Nine month

Contributed 28 % to overall sales in which 45 % revenue come from exports.

Inorganic business

Revenues grew by 40 % to 146 Cr compare to 104 Cr last year Nine month.

Contributed 21 % to the overall sales of which exports was 10 %.

Specialty Chemical Business

Revenue grew by 41 % to 232 Cr compare to 155 Cr in nine month FY18.

Contributed 33 % to overall sales in which 41 % was exports.

Crams Business

Revenue stood at 135 Cr compare to 163 Cr last year same period.

It contributed 19 % to the overall sales and it was 100 % export.

Operating EBITDA growth of 4 % and margin expanded to 40 basis points to 23 % for the quarter compare to last quarter

Key Highlights

Taken price hike with 3 customers

All business had done well except Cramps, Cramps exclude the Dahej operation and it impacted due to shift of campaigns into next fiscal year

Operating performance was impacted due to significant improvement in the raw material prices specifically for Q3.

On refrigerant Gas in this particular quarter there was strong demand in domestic markets. Export have perform well both in terms of volume as well as price realization.

On Inorganic fluoride there was demand from the domestic steel industry somewhat flat but growth in the Glass Industry remain very robust. On export front company have completed successful trials with customers in Korea and also some other new customers company have develop in japan.

Specialty chemical show significant growth on the back of efforts to increase domestic sales primarily driven by demand from the pharmaceutical segment. The export segment which is mainly towards the agro chemical industry also improved both in terms of volume as well as prices. Company did price increases across the products across the markets in the specialty chemical segment.

Cramps business impacted due to push back of campaign of few of company customer to next financial year which has shown slowdown in overall growth. CAPEX in Dahej is progressing well and as per schedule.

Company is continuously building its project pipeline. For new unit and capacity expansion will be as per expectation.

Outlook

Company is extremely positive on Crams business.

Normal margin expectation will be in range of 22-24 %

Raw material price continues on increasing trend

In coming financial year company will be working on full utilisation level.

The contribution from CGMP 3 was not significant in Q3FY20 because commercial production started in December 2019

The complete impact of CGMP 3 will be visible from Q1FY21 onwards

The refrigerant business has seen subdued performance due to seasonal issues and performance was helped due to easing cost pressures

Lot of opportunities in specialty business will majorly start happening from Dahej were the capex for specialty business is happening

The normalised margin for specialty business should be taken between 22-24% and there could be quarterly fluctuations in this

The second customer which was to come back to the company for the CRAMS business is taking time because they have not finalised the route for the order yet

The capex in Dahej is going to be in excess of Rs 450 crores to be spent over the next two years

The specialty chemical division is divided in the following segments

a. Pharma: 40%

b. Agrochemicals: 40%

c. Industrials: 20%

Going forward the split between specialty segment products will remain the same

Expecting good growth in industrial segment over next year and have spare capacities available to service that growth

In pharma & agrochemicals growth is coming from new molecules launches

The additional capex of Rs 90 crores in the specialty segment is a subset of the total capex of Rs 450 crores

Currently in discussion with Honeywell for 3 new opportunities and will be hoping that one of these could transform into a large scale manufacturing capacity

The Honeywell pilot plant is in Surat

There has been a price increase across the refrigerant segments

The impact of fluorspar prices being lower will have an impact in the current calendar year

Contracts with respect to fluorspar are yearly in nature

Keeping a continuous tab on China corona virus situation and as of now no impact on fluorspar prices. It could happen in some other businesses but as of now that has not been seen

The Dahej capex will take place through a wholly owned subsidiary and it will be due to the new tax regime

US continues to provide steady flow for enquiries in the CRAMS business and in Europe the company has been aggressive with relationships with new companies

Have received the environmental clearances for the facility and actual work on land will start from next month onwards in the Dahej facility

The debottlenecking opportunities taking place in the Surat facility are minor in the terms of quantifying

Navin Fluorine announces $410 million multi-year contract with a global company

Navin Fluorine International Limited (‘Navin Fluorine’), one of the largest

manufacturers of fluorochemicals, announced today that it has entered into a $ 410 million (~ 2900

Crores at current exchange rate) contract with a global company for manufacture and supply of a High

Performance Product (‘HPP’) in the fluorochemicals space. The contract is for a period of 7 years and

this product is not part of Navin Fluorine’s existing product portfolio. The capex and project will be

executed through its wholly owned subsidiary, Navin Fluorine Advanced Sciences Limited (‘NFASL’).

Navin Fluorine, through NFASL, will be investing$ 51.5 million(~ 365.50 Crores at current exchange

rate) to set up dedicated manufacturing facility and approximately$ 10 million(~ 71 Crores at current

exchange rate) to set up a captive power plant. The facility will be located at Dahej, in the state of

Gujarat and will be funded through a mix of internal accruals and debt. The supplies are expected to

commence from Q4 of FY22.

Commenting on this Mr. Radhesh Welling, Managing Director of Navin Fluorine said: 'This

Agreement, which represents Navin Fluorine’s largest contract to date, continues to establish us as a

leader in production and delivery of high-performance products within fluorination space.

This Agreement will help further expand our product portfolio and it reinforces the trust global

customers have in Navin Fluorine’s capabilities. It is testament to our deep and wide fluorine

experience and our strength in successfully scaling up of complex chemistries.

This is beginning of our entry into higher value HPP segment and we shall continue to add more

products in this segment."

Does the market know

what is the product?

who is the buyer?

when will commercial production start?

when will contracted supplies start?

what happens if there is a delay in commissioning?

what happens if the contracted buyer rescinds the contract?

what is the input material?

what happens if the input costs go up?

Is the product/ process under patent ?

What happens if some competitor gets a stay.?

So many unanswered questions and the stock is up 20%!!

The possibility of thinking market dosent know anything will be wrong, Market is always ahead, my sense is 2900cr is the contract , so if that comes in in a few years time also, there is visibility of revenue for the future on top of the current revenue.

20% upmove surely is a bit of overreaction for the size of the order , but market also starts extrapolation in such cases. And clearly , this supplements the uptick already shown by the company in terms of sales , magin and earnings growth in last few years. Also, market would be very volatile for chemical stocks during the current china situation.