I am posting my portfolio here for feedback from esteemed fellow boarders.

The basic theme of my PF is the following.

Create a concentrated portfolio with less than 10 stocks and less than 5 tracking positions. Because only a large bet can make sizeable portfolio returns.

For 50% of my portfolio, I want to invest in companies that will grow 3x in 5 years with moderate risk from NSE 200.

For the remaining 50% of my portfolio, I want to invest in companies that will grow 5x in 7-10 years with low risk from the NSE 500 and 1-2 select small caps.

I look for firms with good management, decent execution history and huge opportunity size.

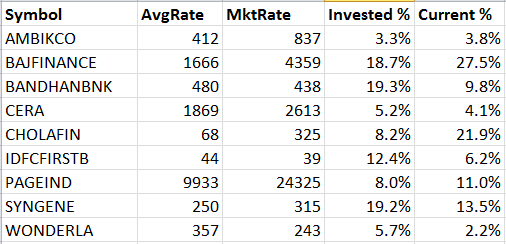

Stock

Percentage

Buy-price & Business

Bajaj Finance

26

1670 ----- Consumer Loans

Cholamandalam Invest & Fin.

21

68 --------- Used vehicle financing

Syngene International

13

250 ------- Outsourced Pharma research

Bandhan Bank

10

480 ------- Banking for the Unbanked

Page Industries

10

9933 ------ Premium Apparels

IDFC First Bank

5

43 --------- Fast growing Private Bank with a retail focus

Cera Sanitaryware

4

870 ------- 10 crore new homes need 20 crore toilets

Ambika Cotton

4

412 -------- A textiles related firm with pricing power

Wonderla Holidays

2

357 -------- Lowest cost provider of water-themed parks

The above stocks are all well documented in VP and I did not want to repeat the full investment thesis again. I believe that all the above stocks will grow into 5X their current market cap.

My goals in the next 6-9 months are the following.

Invest cash savings accumulated over the past few years which were stuck in FDs. SIze of cash savings is 3X the current portfolio size. So I will need to deploy that into the current block and selected new counters.

Keep the number of stocks to below 10 and preferably to around 8-9 or so.

I plan to exit my tracking positions in Arihant Capital (.5% of PF @182), Future Consumer (1.3% of PF @76) and Skipper (1% of PF @194) due to concerns about management quality.

I am losing my patience and conviction in Cera, Ambika Cotton and Wonderla due to lacklustre performances.

I wish to enter the following stocks in 4-5 tranches.

Tech Mahindra - Doing the right things in IT and Digitization.

GCPL/Marico - Fast growing and nimble FMCG cos.

Havells/Vguard - White goods for the next 10Cr people.

PSP projects@480 - Very capable management with a long way to go.

Reliance Nippon@300 - One of the Market leaders in the AMC space.

Cholamandalam Financial Holdings@450 - I wanted to invest in a General Insurance company and Chola MS is my choice.

HDFC Life @550 - I wanted to invest in a Life Insurance company and HDFC is my choice.

Portfolio is highly concentrated on financial institutions at 62% - You may want to diversify a bit.

Also, I would not call GCPL/Marico as fast growing and nimble FMCG cos. - both have hardly grown over the past few years and have their own challenges on segments to grow.

And Reliance Nippon is definitely not one of the market leaders in AMC space.

The stock picks you have are good companies, but most can’t grow their profits that fast unless we are having a tremendous bull run where PE rerating can accompany profit growth. Also, companies like Bajaj Fin, Page, Syngene, Bandhan doesn’t have much scope for further PE rerating, but we can’t say how irrational market’s exuberance can become.

So, it is better to reduce expectations to the level of inherent ‘future’ earnings growth capability, which I believe is ~ 20% with you current picks, in ‘good’ times.

The concentration you see is a natural result of the returns and performance of the stocks. And I am going to deploy 2X capital in the next 9 months. So it would not make sense for me to sell them now.

You are correct, GCPL & Marico sales have grown slowly, but they have been able to generate incremental profits even during periods of low sales growth. This shows that their managements did things right when facing a difficult environment. Can you please let me know what challenges you see in the segments they are in?

In AMC space, the Leaders are obviously ICICI & HDFC with ~3L crore assets under management. Aditya Birla & Nippon comes in at approximately ~2.5L crore assets under management each. So Nippon is in the top 5 overall and have a significant brand recall. HDFC AMC being the only listed peer is very expensive for my liking, that is why I choose Nippon.

Thank you for pointing that out my mistake. My expectations for the riskier part of the portfolio was 21-25% and the lower risk part was 15-20%. I will update the numbers accordingly in the main post.

Personally, I would never prefer to have any stock 20% weight age irrespective of market Gains. Concentrated portfolios will provide great returns when most of the constituents perform well, but takes away sleep when most of the constituents fares bad.

Unless you know in and out of all the your portfolio stocks, I would recommend 20 stocks in common investor’s portfolio. If you cannot increase to 20, at least think about 15.

Next question is related to your FD funds. It’s always good to have fund something like that so that when market provides good bargain, we will be able to gain the most. But I am wondering why did you allow it to reach the 3X of your equity portfolio considering that last 2 years, there are so many mid-small caps avaiable at attractive valuations.

Finally , return expectations seems to be unrelatistic. In the long run if we can beat nominal GDP returns, it would be ok. Anything more than that would be bonus.

Thank you for your feedback. It’s always good to have your convictions questioned like this.

The FD funds are actually from a family inheritance that had been lying in an FD, after years of bugging, they finally allowed me to take it out.

I am investing over 6-9 months and hence I will be having a cash allocation of 15% or more in the portfolio at all times.

I hear everybody talk about Mid-caps and small-caps being a good hunting ground after the last 3-4 quarters giving some good numbers for some companies. Let me take do some snooping around on that front.

As someone said, financials have a strong weightage. You have been a good stock picker to do good in financials in last 10 years. Seing IDFC bank makes me believe you are patient investor and give strong weightage to business enviornment, management people than just numbers. Regarding Bajaj finance at 26%…did you buy it as a momentum buy when you bought or you envisioned significant growth ahead even on a good base and in a turmoil nbfc enviornment? How did you react and what were your thoughts when nbfc meltdown happened? Did u increase allocation or thought to sell but still held on? Would be interesting to know your thoughts as it is you largest holdings…and lastly, with the FD source you mention above, would it be better to invest an FD into risky direct equity or say a mix of debt and equity mutual fund? Just good for thoughts…thanks

Thank you for your kind words. Yes, I am betting on the jockey in most cases. The main concept is that you have someone competent and with decent integrity working for you.

Once the management quality check is done, the only real number relevant for me is the “Market cap” vs “Total Available Market” opportunity in the next 5-10 years.

The problem with MF is that, I would want to know who the Asset Manager is for your fund and measure him up + look into a host of other factors. As a complete newbie to that domain, it would not be productive use of my time.

That’s an interesting metric to consider. Never thought of it before. Would you like to elaborate on this approach, as to how do you determine it and what sources do you trust for obtaining numbers?

Completely exited tracking positions in Arihant Capital, Future Consumer and Skipper last week and I bought some more of Bandhan bank and IDFC first bank.

I feel frozen in fear from entering other stock counters.

I had tried to enter into Info Edge as a very long term bet. But that did not Pan out due to price moving up suddenly.

Are you still adding Bandhan? if yes what is the level to make fresh entry? Although CAA / NRC protests started in Nov, Bandhan has not stopped declining. Do you see any specific reason behind this fall apart from MFI protest in Assam/ NRC-CAA confusions/ Promoter shareholding?

Bandhan is a really long term bet for me. I am confident that Bandhan will become a 5L Crore Mcap in the next 5-10 years time. So based on that assumption, I am holding and adding more in tranches.

The purchase price is actually much lower than what is shown in the screenshot (Approx 300), because I had gotten the Bandhan shares from my converted Gruh finance holding.

“Do you see any specific reason behind this fall apart from MFI protest in Assam/ NRC-CAA confusions/ Promoter shareholding?”

As a “Buy and Hold” kind of person, I just think, will this issue matter to the profitability of the company 12 months from now?

How much impact will it have in the worst case?

Am I ready to live with that?

In my humble opinion. The MFI protest in Assam/ NRC-CAA confusions and Promoter shareholding are all temporary issues.