Results out

Eps nosedives. Revenues take a dip

https://www.bseindia.com/xml-data/corpfiling/AttachLive/bff1ee32-2953-44cb-b130-dd247037237d.pdf

Results out

Eps nosedives. Revenues take a dip

https://www.bseindia.com/xml-data/corpfiling/AttachLive/bff1ee32-2953-44cb-b130-dd247037237d.pdf

“Nose dive” is too harsh a word. It’s 10% lower.

There is a presentation to be released and concall on Monday.

I feel that till Q3 Pharma was not doing well due to destocking globally. The RM was also undergoing inflation. I think this has put a momentary speed breaker on topline. Hopefully, now with Pharma doing well company should come on track with renewed vigour.

Also, need to see the status of API company -Biogenex. They are suppose to get PLI incentives of appx 11 cr annually. With all steroidal APIs being import substitute (mainly from china) sample approval and rampup should be fast.

Eps march 2022 ending quarter 7.02 consolidated

Eps march 2023 ending quarter 1.86 consolidated

On standalone 3.56 vs 6.98

Nosedives anyway you look at it

Look at the paid up capital in mar 22 vs mar 23.

Eps already takes that into account

More shares dilutes yr earnings anyway

Forget eps net profit is 179 vs 512. How is this 10% dip

Seems like a case of oversupply hitting the company when the new capex has not yet started producing profits. So even though topline fell by 17% or so , the operating margin fell from 21.23% to 15.34% . I think the market had anticipated these developments before hand and the stock had fallen from 650 high to 400-450 levels . Unless the new API capex goes live to 1 asset turns of investment , which the management has guided for FY23-24 , it seems the stock will remain around this level, might go to 350-400 levels too, which would be a buying opportunity for me, as the API business in of itself should be worth more than 200 cr .Hopefully with pharma started to do well again from Q4 , the capsule business will recover from Q1 of this financial year .

They are already doing it. 29th 4pm

They have published a revised statement.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/eced586f-0269-4d3c-9f7f-552f2c3ee96e.pdf

Results Presentation and press release.

1). Signed distribution agreement with a large multi billion dollar corporation for Mexico market.

2). Capsule realisations back on track from Q1.

3). API to kick start in Q2 and gradually rampup.

4). Availed benefit of one year extention for taking PLI incentives as next year utilisation expected is 90%. PLI of 67 cr in six years expected.

![]() Concal (Conference Call) - “Natural Capsules Ltd” - Q4 FY23 - my PF stock - First ever Concal

Concal (Conference Call) - “Natural Capsules Ltd” - Q4 FY23 - my PF stock - First ever Concal

Key Highlights -

https://twitter.com/AnirbanManna10/status/1663163476020436993

Rough Notes:

Q4’23 Call

Capsules

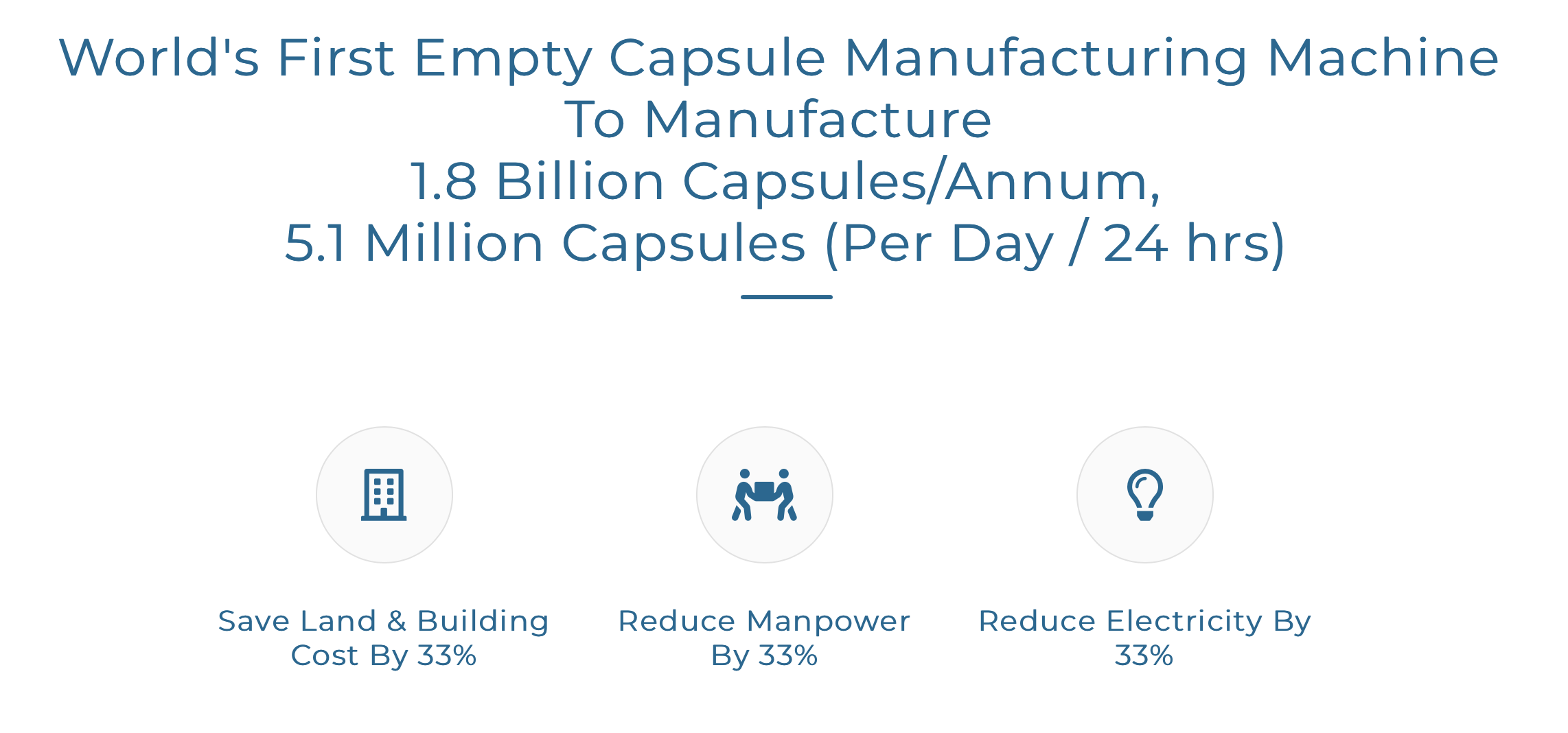

Will become India’s 2nd largest empty capsules manufacturing company after completion of Capex.

Realization have gone down in last Q due to excess inventory and now starting to bottom out and show signs or going up. Some competitors saw price erosion much earlier. There is also softening of raw material prices. So overall we expect margins to be better going forward.

Exports %age could go up from 21-22 (FY23) to 27% (FY24), and 35%+ FY25 because of Mexico order (to start from Q2). Export realization are 15-20% higher than domestic.

Expect around 1.8Bn capsules per annum volume from Mexico contract, .

HPMC - The new high speed machines are first time being customized for HPMC, met some technical issues and hence the delay in installation. Once we find the first line working in Q1, we will try to speed up the installation of next 2 machines.

FY23 gross production, we saw 96% of capacity availability. 17.3B capsules produced vs 18B capacity availability. Can expect similar performance based on HPMC capacity availability for next year.

API

One quarter of delay in overall plan.

Reason for dilution in API - Capex estimates went from 96 to 130 cr. No more dilution planned. Didn’t want to raise more debt. Valuation done on basis of 5 year of forecast, the business should do really well from 3rd years onwards when regulated market exports start.

Opted for PLI from FY25 as anyway we would be utilizing the capacity for only half year in FY24. The rate of incentive per/kg is Rs.6/- irrespective of the qty of production.

Reason for asset turns expectation coming down from 2.7x to 2x: Rise in capex. rates for the target APIs being down. But the rates quoted are mostly for unregulated market for unregistered sources. Regulated markets from registered sources rates are still at old levels. Our target is the kind of customer who are buying from registered source from China.3rd year onwards when we get to regulated markets asset turns can get 2.7x… so roughly 350 cr. revenue potential when regulated market contribute ~35% of API revenue.

Commercial trial batches are right now going on for basic API’s Hexamethasone, betamethasone, predisolone. Most of these products involve 10-11 steps of synthesis and then 2 steps of fermentation. Initially R&D lab had done, gram batches which went on to Kilogram. Now we are scaling them upto 100-200 kg batches. For the base API’s complete inhouse backward integration is being done. As far as derivatives are concerned, our strategy is to import intermediates from China, convert them to derivatives, put them to stability tests, make them ready for market. We are now ready for 16 products stability data, we will approach the drug department for license for them. Once the licenses are with us, we can start supplying these to our customers (For those who are ready to take based on stability data from R&D batches).

There are few customers , who would like to validate the samples from the commercial batches. For them supply would begin (inaudible)

First year we are trying to target the Cat C customer who are sensitive to price, but gradually move up to registered supplier.

Pricing : Betamethasone - earlier 825 USD per kg now 740, dexamethasone earlier 400 USD now 345USD, predisolone earlier 425 USD now 350 USD. This kind of price erosion is mostly for unregistered sources. Exim data sources, imports from registered sources happening at previous rates.

Working capital : Will be little bit higher than Capsules business in range of 90-120 days.

Margins: Expecting to be on lower side in first 3 years when we supply to domestic players, expect it to be higher 3rd years onwards when we supply to regulated markets.

For this year we are expecting 60-65 cr. revenue from API. Hope to breakeven in cash.

natural Capsules currently holds 90% of API division. invested 20 cr. equity and 20 cr debt. (at same interest we are borrowing) operationally we are spending about 20L/month from this qtr. the operating expenses is being absorbed by NC.

Investment of 75 cr : 2 tranches, first tranche we have taken 50 cr. Second tranche is need based. Both have right to refuse (mutual consent).

My take: One way of looking at the current valuation (of ~350 cr.) is, if we assume, the private market valuation of ~250 cr. for API division is right, at close to (or less than) 1x sales for the FY25-26 (max revenue potential from current API capex without considering the exports to regulated markets), then the additional ~100cr. is for API division which can produce nearly 20-25 cr. PAT at normalized levels (post HPMC coming onstream). Seems par for the course to me. Hope the correction is done and we can wait till Q2-Q3 results start showing up nos from both mexico, HPMC and API.

Let’s be conservative and take the private market valuation at 200 cr and assume the yearly profits remain at 15 cr for capsule business . You will get the capsule business at 150 cr valuation at 10 times earnings per share .

I believe the stock is very cheap but the market can test your patience on both sides . Being a micro-cap even more probably .

One of the risks in Natural Capsules story that I see is as following -

All the innovation, cost savings, speed, energy savings etc. are happening because of technology developed by DBDS robotics. My understanding is that this technology is not exclusive to Natural Capsules. DBDS is free to sell these latest machines to any clients they can get.

This combined with the fact that capex to put a new line of capsules is not very high (sub 50cr).

So natural capsule is more of an early adopter of latest technology developed by DBDS and that is the advantage they have. With low capital requirement & easily available technology, any advantage of technology will not be durable and eventually all the efficiency benefits would have to be passed on to the customers (B2B, large customers). This is like Textile industry where everybody moves to latest technology and nobody makes above average ROCE.

A caveat to above observations is that - this is more like a terminal risk where it can take multiple years for this risk to play out. In the meantime, a company can manage to maintain some advantage over a few number of years and investors might make decent amount of money.

Disc - No investments

P.S. The gallery page of DBDS robotics is quite interesting. Both AGC and Lonza have visited DBDS premises to look at the machines.

Firstly, several insightful posts about the company have been made in the thread , including the video interview and have helped me. Thankyou!

I was going through the AR today and it seems that the API production has been pushed by another quarter, now commencing from Q3 FY’24 instead of Q2 but the management says any temporary setbacks (caused by the delay) will be compensated by the capsules business which they are hoping to pickup in the coming quarters probably based on the sequential addition of HPMC capsules which may bring better margins.

While I was preparing myself for such a likelihood(for the short-term), wasn’t exactly expecting further delays as regards the API piece ,even though it is heartening to hear them consider Allocating 3.5-4% to R&D. It’d be very helpful if experts and the sector watchers could add their thoughts. Thankyou.

P.S - Invested and could be biased

Hi @Vik,

Even Q3FY24 should be taken cautiously as the management in their last con call indicated that the PLI payments will be live on FY basis. That is why they had initially postponed it to FY 24 instead of the present FY. Given that, We should expect it to get commercially live only in FY25 until which capsules should hold.

Disc: Invested

Yes, got it. Point taken. Thanks! Would be interesting to see if the capsules margin picks up owing to domestic neutraceuticals in the upcoming quarters.

They mean margins will come down from 21% to 14-15%?