As a R&D scientist my views are like below….

Setting up a fermentation plant requires very high capital investments and since this industry has been highly marginalised by an import onslaught from a single source, it needs special attention. Initially, huge capacity was created by both the public and the private sector to cater to the growing demand. However, because of the cheap rates, a substantial quantity was being imported from China, forcing local manufacturers to shut down operations as production became commercially unviable. Today, India does not have any manufacturing facility for fermentation-based products and is completely dependent on a single source.

Natural capsule is going to setup the fermentation plant facility & they are targeting steroids & there intermediates. Which are easy to manufacture by using fermentation technique rather than organic synthesis.

Natural capsules Is able to produce betamethasone (don’t know about gram or kilo scale), & only the import value of the same were around 126crores of INR (98% Percentage of dependency on a single source (of total import)). Domestic sourcing of betamethasone around 20%.

Search for ‘Chandan Raj’ on linkedIn, R&D Manager, what I have heard is, he is the tech brain behind this venture.

Company continued it’s execution and posted good numbers. Few important updates from the IP & Press release.

-

Installed capacity for capsules currently stand at 16.2 BCPA. FY21 ended with 14.4B capacity, The addition was done in month of June (hence contribution to numbers was limited to that extent).

-

4 new generations machines to be commissioned by Q4’23 taking the capacity to 24.1 BCPA. So about 50% increase in capacity by this year end.

Q2 - 1 line of gelatin capsules was added in Aug.

Q3 - 2 lines of HPMC(Vegan) capsules to be added.

Q4 - 1 lines of HPMC capsule to be added.

Note: HPMC capsules have only 50% capacity of gelatin capsules, but with 2.75 to 3 times realizations and with higher margins. So the 24.1B capacity should be accordingly revised. -

On API front, capex figures have been revised from 96 cr to 115 cr. So accordingly asset turns expected has been revised from 3x to 2.7x

-

Commercial production to begin from Q1’24

-

Export figures for all 3 API’s has been updated in the new slides for FY22 (older numbers were for FY21).

Dexamethasone import remained constant at 19 MT for FY21 & FY22

Betamethasone import increased from 20MT(FY21) to 25MT (FY22), growth of 25%

Prednisolone import increased from 30MT (FY21) to 39MT (FY22), growth of 30% -

Company has received Letter of Intent (LoI) for it’s API’s products from buyers in US, Japan and domestic markets for more than 100 crs on an annual basis. So Mgmt is confident of exceeding 50% capacity utilization in first year of operation (which is hopefully FY24)

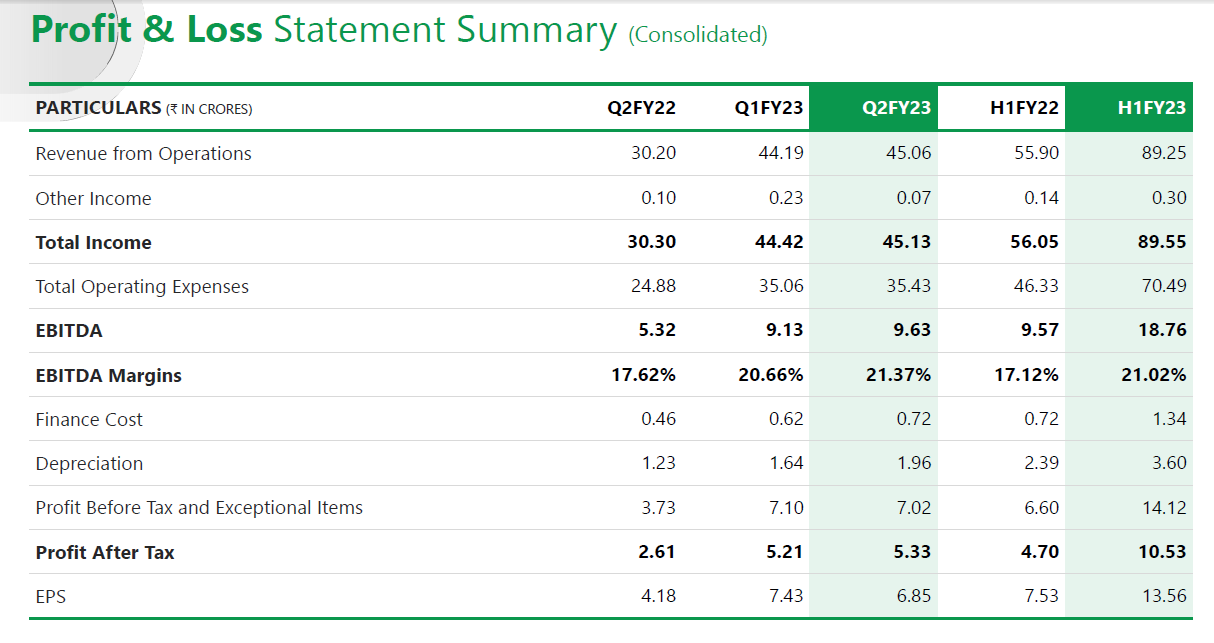

Getting external funding for the API business , valuing the API business at 225 crore . The capacity of th capsule business has gone up from 14 BCPA to 18 BCPA. they should start seeing volume and slight margin expansion in the coming quarters. This capacity will go up to 22 BCPA by the end of Q4 FY23. If the Q2 net profit was 5.3 cr, I believe conservatively at the end of Q4 results the net profits will be around 6 cr . This will lead to an yearly profit of 24 cr at least for FY24. So the stock is trading below 15 PE for conservative FY 24 profit.

At full capacity with slight margin expansion quarterly profits will sky rocket to 8.5 cr , yearly profit for 36 cr, which would mean the business is trading at less than 10 PE.

I do believe margins will expand as these new capsule lines are said to produce higher margin capsules, but also the fact that slowly the power, packaging and logistics cost will be coming down, there should be some margin expansion as well.

Add to it the fact their API business got external funding , valuing just their API business at 225 cr (https://www.bseindia.com/xml-data/corpfiling/AttachLive/99c656a8-49a9-4121-bcb3-825f6931c902.pdf) . The stock seems extremely undervalued .

Let me know if I am missing something .

Disclaimer :- Invested from lower levels. Thinking of adding more.

What is the moat for Natural capsules? There are other domestic players as well. Do you have market size and market share data?

Anant, if you look at the P&L, there are 3 main cost items for this company namely, raw material, employees and power cost. Raw material costing I believe is same for everyone (size could play some role, but broadly same). Employee cost and power cost is where one can save money if the machine can make higher number of capsules per day. Employee cost will provide the maximum operating leverage, and power cost to some extent.

This I believe exactly what is playing when the operating margins move up from ~9-10% to ~20-21%. Earlier like everyone they also had machines making ~2 mn capsules per day. But due to its R&D efforts they have been able to get machines making ~5 mn capsules per day. And that has made all the difference.

Apart from that, consistent quality, desired volumes and lowest cost are the basic hygiene factors that every company need to follow.

But just take a look at broad picture. The largest player is Associate capsules (ACG) which has 120 bcpa capacity out of India’s 250 bcp, so 50% market. They targeted last year to double the capacity soon. How natural capsules would have advantage over this giant?

vegetarian capsules could be a big play, because to supply issue of Gelatin, but all companies are doing veg. capsules.

After coming up of this large capacity, margin may not stay at that levels.

If anyone had a word with the management, can throw some light on it.

ACG is 50% of the market capacity is a fact. And Natural Capsules will be ~10% of the market capacity is also a fact. The answer to your question lies in P&L. It is the speed of machine (5 MCPD vs 2.5 MCPD) which will determine the costing.

Like I mentioned in my previous reply, lowest cost producer along with other hygiene factors will get the business. Since ACG is not just a capsule manufacturer, it is difficult to understand the comparable business profitability.

Vegetarian capsules is not a novelty, I agree with you.

Regarding the supply chain issues of Gelatin, in the western world this is an established industry with enough supplies. Temporary disruptions are difficult to call out.

Any idea about the other Steroidal API players in India? Any update on fermentation process. I heard its very tough to crack, very few manufacturers cracked the fermentation technology thorough collaboration only.

Anant, suggest you to listen to Gujarat Themis calls. Fermentation is a tough process, but it is energy intensive. India had a head start over China, but as Chinese took lead, we stopped this process completely. That’s why we don’t hear about fermentation in India.

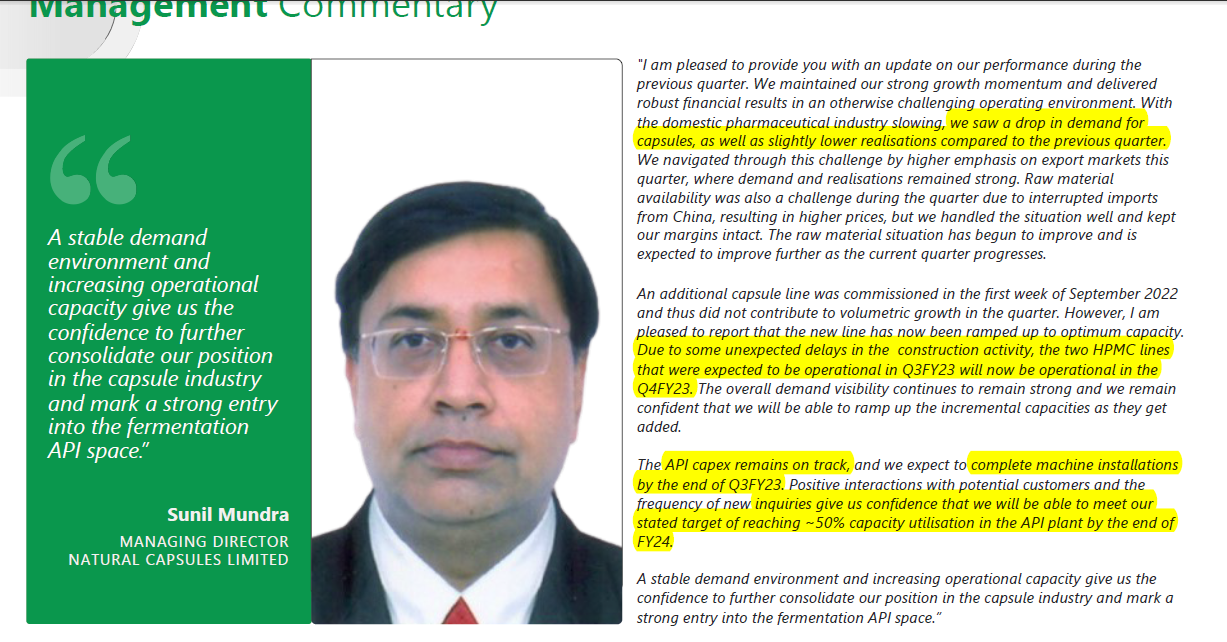

Results press release

https://www.bseindia.com/xml-data/corpfiling/AttachLive/c3a752f5-30b7-4722-8c74-13d2c7a8ee7c.pdf

There was a very nice management interaction where they talked in length about evolution in their business. I have captured the notes below.

07.03.2023 (Smart Sync interview)

Capsule business

- 95% of revenues come from gelatin capsule

- All competitors have expanded capacity in capsules, current capacity is excess of demand which should get absorbed in next 2-3 years

- Global peers: Capsugel (Lonza; largest co), Qualicaps (Mitsubishi; second largest co), ACG (largest Indian co)

- India: 60-70bn capsule demand, 8-10bn is HPMC capsule

- Had introduced HPMC capsule in 2002 (5-years earlier than competitors). But their size was very small to gain a lot of market. Also, in 1999 India had introduced a green dot on capsules (which causes demand for HPMC capsules) which was later withdrawn in 2004 and this effected the HPMC capsule market demand

- Demand for HPMC capsule comes largely from nutraceutical market. For e.g. in US 75% of nutraceutical market is HPMC capsule

- New capacity is coming in vegetarian capsule (HPMC capsule), product mix should change from gelatin to higher realization HPMC capsule (15-17% contribution from HPMC capsule in next 3 years). With this, EBITDA margin can increase to 23-25% from current 19-20%. They have installed a 5bn capsule machine (higher capacity than other machines), where they have MOU that they will be exclusive users of the machine if they keep buying from them (not clear for how long)

- Raw material for HPMC capsule is imported (RM chain: pine wood / cotton → wood pulp → cellulose → chemically treated to make HPMC)

- One of their peers strategy is to give filling machines on lease to get more business

- Indian unlisted peer is doing higher margins: very old and entrenched player and has the first mover advantage and are the only suppliers in certain regulated markets. Natural capsules’ latest expansion gives them better machinery

- Its very hard to get into other customer accounts for existing filings as the filing is already done with the current capsule supplier and cost of capsule is miniscule. Unless there is a big supply hiccup, there is no need to change the capsule supplier

- Export: 25% of capsule revenues (blended realization is 108-110 per 1000 capsule). Export realizations are higher by 15-17%

- Supplies to Pfizer in India, currently discussing with their Mexican operations

- In 2015-18 cycle, they had a lot of exposure to Nigeria (direct + indirect supplies; 60% of total exports) which got impacted thereby impacting Natural Capsules. Didn’t supply to government, only private buyers

- Strategy to deal with this was to diversify and go after volume based clients in domestic market and sell on just-in-time inventory model (operating leverage cuts both ways?). Even during covid when International market demand was higher, they focused on high volume domestic customers

- Receivable in pharma were always higher, during covid this reduced to 60 days. It is going back to 90-120 days

- Their strategy historically (until 2018) has been to buy used machines to ensure higher asset turns

- R&D spends will increase from 2-2.5% of sales to 3-4%

API business

- Capex: 130 cr. (expect 1x asset turns in FY24 and 2x on full utilization)

- Steroid API: Customers like Lupin and Cipla are looking for alternate suppliers due to Chinese supply chain problems which is opening opportunities. Natural Capsules will do fully integrated manufacturing (starting from raw material phytosterols which is available in India and exported to China). It’s a sandwich process (fermentation then chemical synthesis then fermentation and 3-4 synthesis steps) making a long chain. It takes time to crack these processes and this gives them leeway to get regulatory approvals and establish customer relationships before competition comes in. Have brought in a separate team with experience in commercialization of fermentation based APIs from China

- Fermentation is done on batch mode

- API margins: 10-12% in domestic market, 15-18% for customers who are exporting formulations in US but buying intermediates from China, 15% in ROW, regulated market like US and Japan (25-27%)

- First product will be Hydrocortisone (don’t have PLI approval, but huge demand in domestic market) followed by Prednisolone (1 step fermentation ahead in chain of Hydrocortisone). After that, they will introduce Betamethasone followed by Dexamethasone

- Commercialization has been a bit delayed (validation batch from March to April-May). Can potentially contribute 1x fixed asset turns in first year of operations (140 cr.)

- Starting out with importing intermediates from China and will then backward integrate

Disclosure: Not invested (no transactions in last-30 days)

As per recent allotment of shares API business is valued around 250Cr, Parent company available at 390cr. Some more capex (Vegetarian capsules machines)is yet to come on stream, this product has higher realization as compared to gelatin capsules.

Standalone business is available Price to sales < 1.

I think still some more room available for investors

Couple of interesting things happening here. Elevator pitch pointers;

- Capacity augmentation by ~80% within FY’22.

- Sharp jump in Operating margins (from 10% in FY’18 to 21% last fiscal).

- Promoter holding increased by 4%+

- Significant capex 150 Crs.+. Getting into low domestic competition fermentation APIs with eligible for sizable PLI subsidy.

I think key broad monitorable on the legacy capsule side of business are:

- Competitive intensity - possibility of supply glut considering the kind of huge capex in last 4/5 years by each of the key players and few players accelerating the capacity even more aggressively going ahead.

- Margin profile has improved in recent years. However historically for them and even across rest of the players in the industry has been in the range of 6% - 10% of Net margins. How much of margin improvement they are able to drive with change in product mix (high proportion of HPMC) and significantly improved production yield (using high productivity machines) will be important.

Have tried to map the competitive landscape for the legacy Capsule (Gelatine/EHGC) and HPMC/Vegan) business

- Global empty capsule market size - ~1000 Bn/Year

- China empty capsules market ~450 bn/year (45% marketshare)

- India empty capsule market size - ~220bn/Year (22% marketshare)

Lonza:

- Must have capacity ~220 bn capsules/year. (mostly equal to all Indian manufacturers put together)

- In 2020, announced an investment of 93M USD To expand its overall production capacity of capsules within Capsugel® portfolio by 30 billion capsules annually. The investment allowed them a 15% increase in capsule production capacity. (link).

- This investment was to be be made over two fiscal years, 2020 and 2021, across eight global Lonza manufacturing sites including the one Lonza site in Haryana India

- This announcement came in quick heels of previous announced capacity expansion in 2019 where they had increased the capacity by 10 bn/year.

ACG Capsules ( link):

Must be within top 5 globally and number one in India. The group has a capsule manufacturing capacity of around 115 billion units per annum. spread across six plants located in India (4), Croatia (1) and Brazil (1)

- The group’s diversified customer portfolio consists of marque clients such as Cadila Healthcare Ltd, Aurobindo Pharma Ltd, Alkem Laboratories Ltd, Sanofi S.A, among others.

- Revenue of ~1550 Crs and PAT margin of 10.60%.

- PAT Margin is 10.6% for FY20 and 14.9% for FY19.

- Unencumbered cash and bank balance stood at Rs 99 crore as on March 31, 2020. Cash accrual, expected at Rs 450 crore each in fiscals 2022 and 2023.

- Debtor days of 120 days (very high as compared to rest of the India players)

- Significant capacity ramp-up: From 83 bn capsules/year in 2017 to 115 bn capsules/year.

- Further, doing a capex of 600 Crs to double the capacity. Mostly into fast growing HPMC capsules.

Natural Capsules:

Is engaged in manufacturing of Hard Gelatine Capsule Shells and Hard Cellulose Shells to be supplied to various pharma companies in India as well as abroad (primarily un-regulated markets). The company has two manufacturing units; one in Bangalore and one in Pondicherry

- Impressive 70% revenue growth. Revenue of 135 Crs against 80 Crs for last fiscal. ~20% revenue from Exports for FY’22.

- EBIDTA of 18%. PAT margin of 10%

- Good discipline visible in cash cycle. Cash cycle of 170 days in FY20 to -6 days in FY22.

- Had a combined capacity of 13.3 billion capsules per annum as on March 31, 2022. Which has been rapidly increased to 18 bn within 3 quarter of the fiscal FY’23. Further projection to take total capacity to 22 bn by financial year end at a capex of 38 Crs.

- Significant capacity augmentation made possible by tech breakthrough in machine line optimization (from 1 million capsules per day to 5 MCPD).

Sunil Healthcare:

BSE Listed player (Link) with <50 Crs market cap (for context Natural capsules has MCap of 365 Crs.). SHL is mainly engaged in the manufacturing of Empty Hard Gelatin Capsule (EHGC) shells and Hydroxypropyl Methylcellulose (HPMC) at its sole unit at Alwar, Rajasthan.

[Trivia: The company was earlier also engaged in the trading (including merchant trading) of agro based commodities since 2013, under brand ‘Sunloc foods’. However, the same has been discontinued in FY20]

- Revenue of 116 Crs for FY22 as against 90 Crs for previous year. Net margin 6% (was reporting net loss for previous 3 years). Cash cycle has improved this year and both debtor and creditor days have reduced significantly.

- Had capacity of 13 bn in FY18 has been increased to 15 bn by FY22.

- Company is planning to increase proportion of HPMC capsules in revenue from operation which is likely to further improve profitability going forward.

Medicaps:

Again a BSE listed player with market cap of <50 Crs. (link). The company is in the manufacturing of the Hard Gelatine Capsules and is equipped to produce 7.5 billion pieces of empty hard gelatine capsules per year.

- Presently, the company has discontinued its pharma business operation and has entered into real estate business.

[Trivia, they had invested a small amount in share of Natural Capsules. What to make out when competitor trust you with his money?] ![]()

Gelcap:

Couple of years back Aurobindo Pharma went into short of tooooo far backward integration. Gelcaps, a partnership firm, is entirely owned by the promoter family of Aurobindo Pharma Ltd,

Gelcaps has an installed capacity of 3.51 billion capsules that will go up to 5.07 billion capsules with the ongoing enhancement.

- Gelcaps is expected to register strong revenue growth over the medium term, as it has now become the majority supplier of gelatin capsules to Aurobindo Pharma.

- The firm also booked a strong EBITDA margin of 29.7% (FY20: 27.1%; FY19: 4.23%) during 11MFY21. The margins are likely to remain strong at around 30% over the medium term as Gelcaps sells capsules to Aurobindo Pharma, which are then sold to regulated markets and thus command high margins.

- Revenue of Rs 44 crs in FY20 as against 29 crs in FY19. PAT margin were around 6%. Interest cost must be diluting net margin considering high debt that they have got from promoter group.

- They will have biggest customer concentration risk out of all the players, should any regulatory issues hit Aurobindo.

To conclude, each of the industry players have worked swiftly to a) capture the covid induced demand, b) shift/preference towards HPMC in nutraceuticals and c) void being crated by capacity of ~7.5 bn going away due to MediCap discontinuing operations. However, going ahead, the situation can be challenging:

-

On export side, Lonza is/has augmenting capacity by decent 30%, mostly into high growth HPMC.

-

Likewise, in domestic, ACG is aspiring to further double its capacity. They are deeply entrenched player with E2E offerings (film and foil packaging, tableting, granulation, encapsulation, packaging machines and all).

-

Finally, Aurobindo’s business may gradually move captive (GelCap) at least for any of the new product launches/dossier submission.

Disc: No Position

Tarun

Now essential drugs prices will be linked to WPI.

Seems reasonable breathing space will be available to manufactures of essential drugs.

Immunosupprents (steroids) are included.

(APIs of Natural capsules).

This move is essential for atma nirbharta in essential drugs

Thanks for the nice compilation of competitive landscape. Adding few observations.

Gelpcaps already went to 5.04 billion capacity in FY22. [Source] (India Ratings and Research: Credit Rating and Research Agency India) and perhaps as a result posted very strong revenue growth of 35% in FY22.

ACG receives roughly 50% of it’s revenue from exports. So roughly one can say out of 115Bn capacity, 60 Bn cater to Indian market, which is ~4-5x of NC’s capacity. A strong entrenched player with close to 25% market.

Some other prominent players

-

Healthcaps India Ltd - capacity 19 Bn Capacity has gone up from 17.4 to 19B in last year.

Seems like Medicaps went into capsules manufacturing through a JV with it’s private arm. The company is still in operation, with about <35 cr. revenue rate in FY20. So capacity can be roughly assumed to be in range of 4Bn.

-

Erawat - 3.6B

-

Renown Pharma - 2Bn

-

Qualicaps - Mgmt identified this as one of competitors. Not much info. on India capacity.

(In the recent interview mgmt. identified the following top top 3 players as competition i. Capsugel / Lonza, ii. Qualicaps - worlds second largest, from Mitsubishi group iii. ACG, India’s largest.

In Capsules, product level differentiation is perhaps very less. It forms the least expensive component in the finished formulation (at Rs. 0.11 per piece). From India perspective while ACG is clear market leader with ~60Bn of it’s capacity catering to Indian market. No. 2, 3, 4, 5 place could be held by Lonza, Qualicaps, Healthcaps & Natural Capsules in any order. I don’t have specific capacity nos. of Lonza’s & Qualicaps India site, so it’s hard to put a proper rank. HealthCaps and Natural Capsules are neck to neck in terms of capacity, with NC slated go in front of HealthCaps with current capacity addition. Sunil Healthcare is perhaps a close follower at No.6 with 15Bn capacity.

Earlier I used to think the capsules market to be highly fragmented, but with this exercise it’s clear that ACG (60Bn), HealthCaps (19Bn), NC(21Bn), Sunil (15Bn), Gelcap (5Bn) put together cater to roughly 120/220 Bn of the market and we don’t know the numbers of Lonza and qualicaps, 2 majors. So these 8 players could be catering to 60-80% of the whole Indian market.

Rest of the players seem to be at lower end with about 2-4Bn capacity. It wasn’t easy to find information about the capacity addition plan’s of these smaller players. It’s clear most top players are adding good capacity.

Like you mentioned, Lonza’s capacity addition numbers are across 8 sites worldwide. So a educated guess would be ~4 odd Billion for India site ? With this addition they would become 25% of the global market (1000 Bn) supplier. Which is huge. But with NC deriving hardly 20% of it’s revenue from exports, which is say 3.6Bn out of 18Bn, they are anyway no where in picture to compete with the likes of Lonza in export market.

Another aspect that i found interesting about the capex and capacity is:

For Natural Capsules, the capacity enhancement from 10.8 to 24.1 Bn (13.3 Bn) is getting done at expense of 38 cr., which is 2.8 cr. capex requirement per 1Bn capsules capacity.

Compare this to Lonza’s estimate of 93Mn USD for 30 Bn capacity which puts capex requirements per 1Bn capsules at Rs. 24.8 cr. (Not strictly comparable as it’s spread across the world)

Compare this to ACG’s estimate of 600 cr. for 115 capacity, which is 5.2 cr for 1 Bn capacity addition.

So no wonder, ACG is upping it’s game to go from 115 to 230 Bn capacity and come in the same league as world market leader Lonza in one shot.

In the mgmt. interview shared above, Mr. Sunil Mundra has explained (at 32 min mark) why it’s easier for entrenched players to keep getting stronger. Natural Capsules is not there in the league of Lonza/Qualicaps/ACG right now but it definitely seems to be rising above the bottom rest in the market. Post this expansion, NC has good chance to be No. 4 behind Lonza, Qualicaps, ACG for Indian market.

As per some research reports, the empty capsules market is expected to grow at rate of 7.9% over next 10 years. While HPMC market is expected to grow by 9.5%.

Supply glut is a possibility, or another possibility could be strong becoming stronger, if just ACG & Lonza put together are going to cater to ~50% of the global market.

Disc: Invested from lower levels. No transaction in last month.

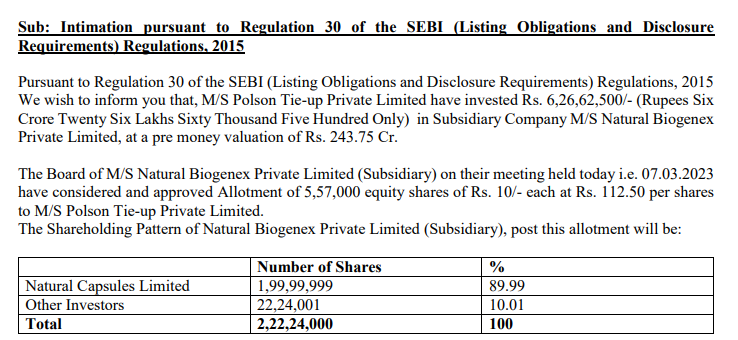

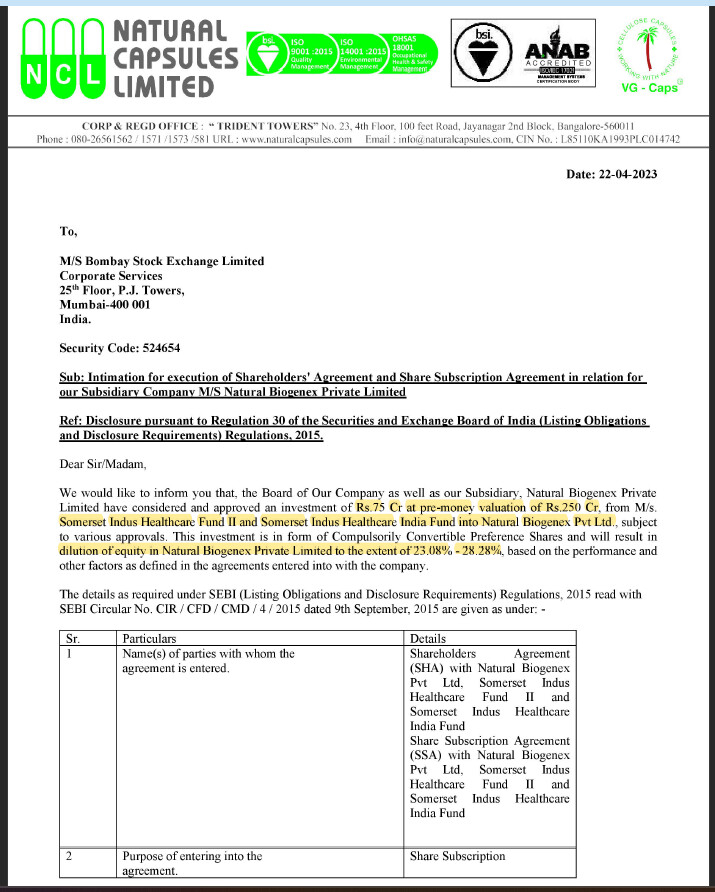

another significant cash raise by the API division of the company. 75 cr. raised at pre-money valuation of 250 Cr. from Portfolio – Somerset Indus Capital Partners for 23.08-28.28% of the company.

Seems excessive dilution at low valuation. Unable to see rationale