That’s exactly what I made of it as well. If the HPMC capsules don’t take the margin back to 19-20 then probably it will hover around the mentioned range till API gets approved for the regulatory markets which may seem some time away. Ofcourse any favourable price movements of the API products under consideration can affect the overall margins positively. Just my humble understanding.

Natural Capsules making 5.5 crs of investment to get 10.66 MW of renewable energy… After raw material, power is the second biggest cost for them… In last 4 years, they have already reduced power cost as % of sales from 15% to 8%… even in the subsidiary where power will be one of the main raw material due to the manufacturing process that they will follow, It would be interesting to see how this cost will behave over next 2-3 years…

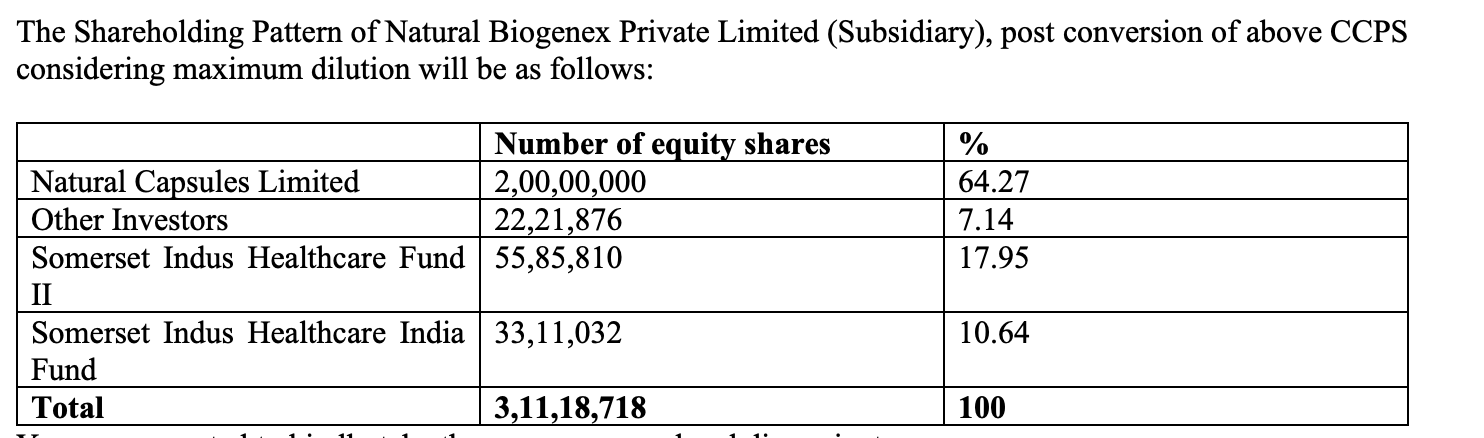

M/S SOMERSET INDUS HEALTHCARE FUND II and M/S SOMERSET INDUS HEALTHCARE INDIA FUND have invested 2nd tranche, Rs. 25 Crore in M/S Natural Biogenex Private Limited, at a pre money valuation of Rs. 250 crores.

The timing of the move does make it look like it was a “news” driven move.

But the strength of the upmove remains to be seen, as there’s no “new” news.

This is just the 2nd tranche of the announcement months ago, and at the same valuation. So does the market know something we don’t, or is this just a big day after a “big news” dropped, moving after months on consolidation. Will definitely need to see the price-action in the coming days/weeks.

Any updates on the PCB approval that was pending as the regime changed. I had mailed them but they are a bit busy to respond to that. The last update on Concall was that they were ready to start commercial production as soon as they got the approval.

This is what they stated during the last call during Nov. They quantified it to 3 to 4 weeks for the PCB which was delayed due to the regime change. But there were no blockers for the drug license. Surprising to find both pending till now.

Yes, this is concerning. But bureaucratic processes in India can be complicated so I’m okay to give it another quarter. They say they should have it wrapped up in a week and hope for a positive resolution, this should be wrapped up soon. Otherwise will reconsider staying put.

Meanwhile, expecting some correction, provides a decent oppurtunity for entry, given the overall market is pretty out of whack w.r.t valuations

I think capsules business may take 3-4 more quarters to improve margins. Installing HPMC lines may not boost the neither revenue nor margin due to poor demand of the capsules in the market.

I feel they are intentionally dragging the commissioning of HPMC lines as they are not able to run the existing lines at 100% capacity due to poor demand.

Even after few quarters 20% margins in the capsules business is seems to be unlikely, we may expect an avg 15% margins.

API is very long way, we may not see any significant contribution to bottom line in FY25, we need to wait long time for recovery in the numbers & stock price as well.

PCB approvals are electronic now. Though you do spend some bucks in getting it, It is not as tough as it used to be. Seems it will be tough for chemicals/ Pharma companies given the stuff they are dealing.

Same, Staying put for another quarter and begging dear god that they don’t come up asking another week.

Today was a 6% drop, Waiting to see if it will drop anymore and would top up (≈ 300) will be sweet.

On API you are very right, The companies promise of Q1 FY25 for the small volume commerical sales should probably be taken up with a truckload of salt.

I am genuinely confused whether it is taking them so much time as they are just venturing into the field. But there exist people who take care of projects, approvals and equipment installations to make the entire job seamless right.

Did the company not engage them and is trying this out as a DIY?

I am concerned that if a new player comes in for the same Steroidal API mfg stuff and reduces the market size for NatCaps.

HPMC commissioning has to have happened by now, Shot off a mail asking if they can share an update and called them. As usual, You will get a response sir was received. Let’s see.

I have exited the most of the allocation as uptick in revenues and profit is seems to be impossible in the FY25 itself.

Something wrong with capsules business also, earlier they were telling sluggish demand due to pharma companies are with excess inventory. Now all pharma company numbers are good still they are not able to see jump in numbers, this could be due to price erosion and excess supply from competitors also.

I will revisit once API segment make some +ve EBITDA

Think this Q result should confirm on this. I’m holding this until then.

The management is sweet on asking us to mail them for queries but don’t get back - It will be great if someone does.

Does commencement of production of small volume batches means they have received final clearances from the Pollution Control Board and the license from the Drug Department? any idea?