True. Very good thread, more so because he put it before the investor presentation was out. He absolutely captures the things as they stand. Nothing is written in stone. I particularly liked the areas he highlighted for further home work :

→ Economics of capsules, technical advancements, demand-supply.

→ Economics & technical barriers for selected APIs.

→ Domestic production vs imports of selected APIs, cost differential, tariffs.

→ Management pedigree

Thank you for your kind words. Couple of additional points that come out from the presentation:

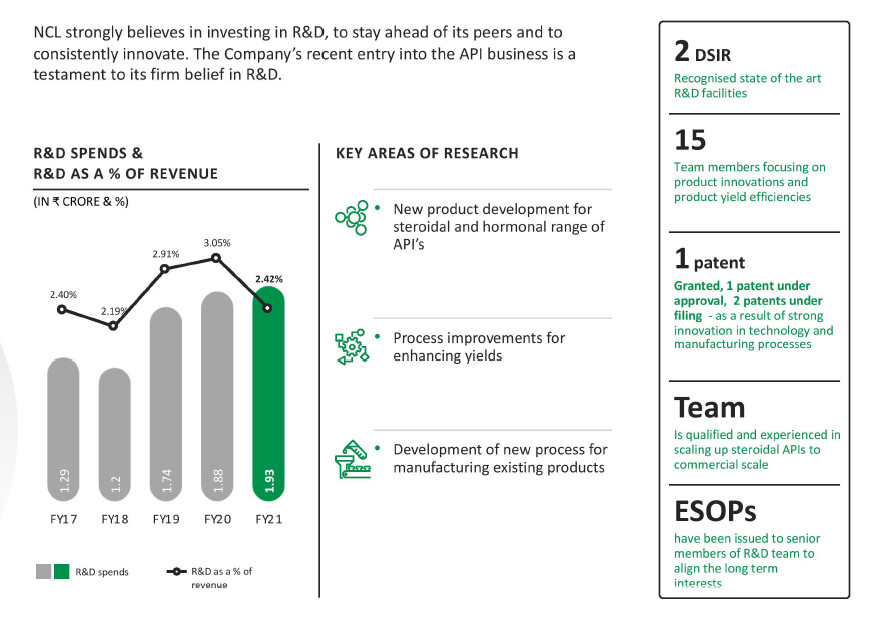

page 18 - issuance of ESOPs to senior R&D employees - good alignment of interest

page 16 - bank loan of 48 crore @ 6.4% - very good interest rates - debt to equity is conservative at 1:1 with rights issue (28 cr) and internal accruals (20 cr).

page 16 - healthy gap between planned capacity and annual imports - growth is possible (barring entry of competition) with NatCap being only manufacturer

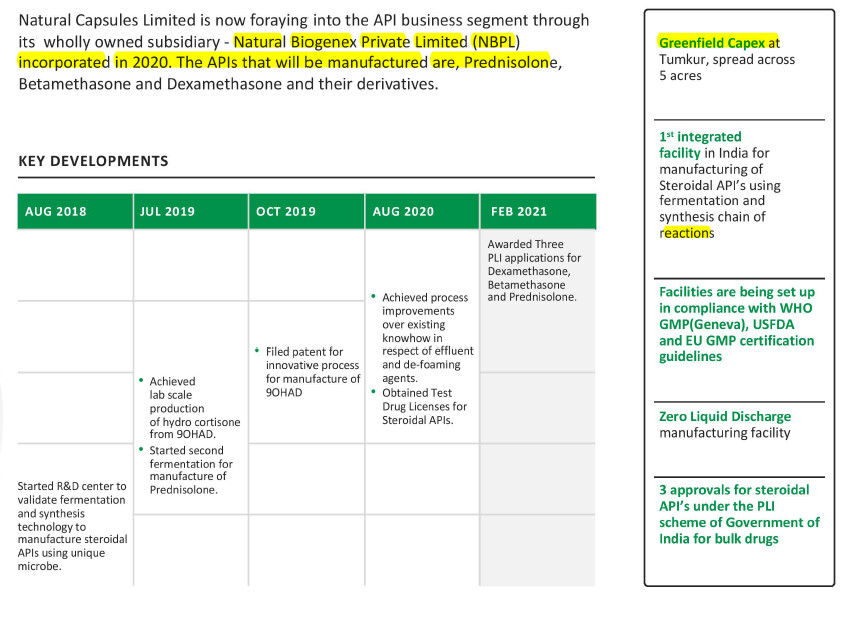

Further, this isn’t NatCap’s first attempt at API manufacturing - they signed to buy an API unit from an Arun Kumar (Strides) company earlier in 2020, but it got cancelled by the counterparty at the last minute.

You are in valuepickr also Great. My conclusion is like this . What is future upside we are looking at - PLI. You have beautifully brought out there is no fermentation capability. That one point is enough to make an investment decision. Ignore numbers and financials. Anyway we know the strength of capsules business which has no pricing power. We need to thank you for such a great analysis which shattered my previous banking on import substitution.

I didn’t understand this point, all @Leading_Nowhere said is “However, promoters don’t seem to have experience in complex fermentation.”

Which is valid apprehension, given lack of proven experience in the mgmt on fermentation chemistry and it’s a new line of business for them.

However, it’s not like they have woken up today to this dream opportunity called ‘fermentation chemistry’ and asking for public money to run after their dream. IP has given details of the steps they have taken so far and their AR in FY20 & 21 has also been talking about it.

As investors it’s our job to consider the situation as “I will not fall for the goli’s” as they don’t have fermentation chemistry experience

OR

I see some info which makes it an interesting opportunity to look at further and now I will work on gathering more info in the line of what @Leading_Nowhere mentioned

→ Economics of capsules, technical advancements, demand-supply.

→ Economics & technical barriers for selected APIs.

→ Domestic production vs imports of selected APIs, cost differential, tariffs.

→ Management pedigree

We all have our own way of handling such uncertainty !!

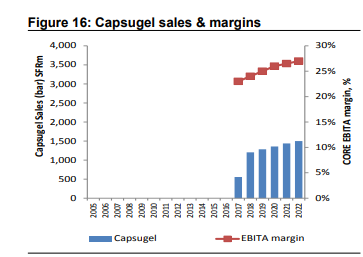

Capsugel is definitely advanced compared to Natural capsules. It has turnover of 1.5 b SFR and was sold to lonza at 5 b USD in 2016. Margins are consistent in the range of 20-25%.

Hi Guys, I found this article in today’s ET

ACG group plans to set biggest vegetarian capsules Unit in Maharashtra

Planning to do capex of approx. INR-800cr.

Link- Here

putting these 2 together… it seems like the story will keep getting incrementally better over next 5-6 qtrs…Capsules business in itself perhaps doesn’t deserve such rich valuations… but this player has moved from being 10% EBITDA margin player 5 qtrs back to 20% margins in current qtr… with strong capex outlook both in Capsules & the new territory of API. Still fearful of adding to current position and also fearful of it being a trap on disappointment in performance…So for now holding on…

For the API foray:

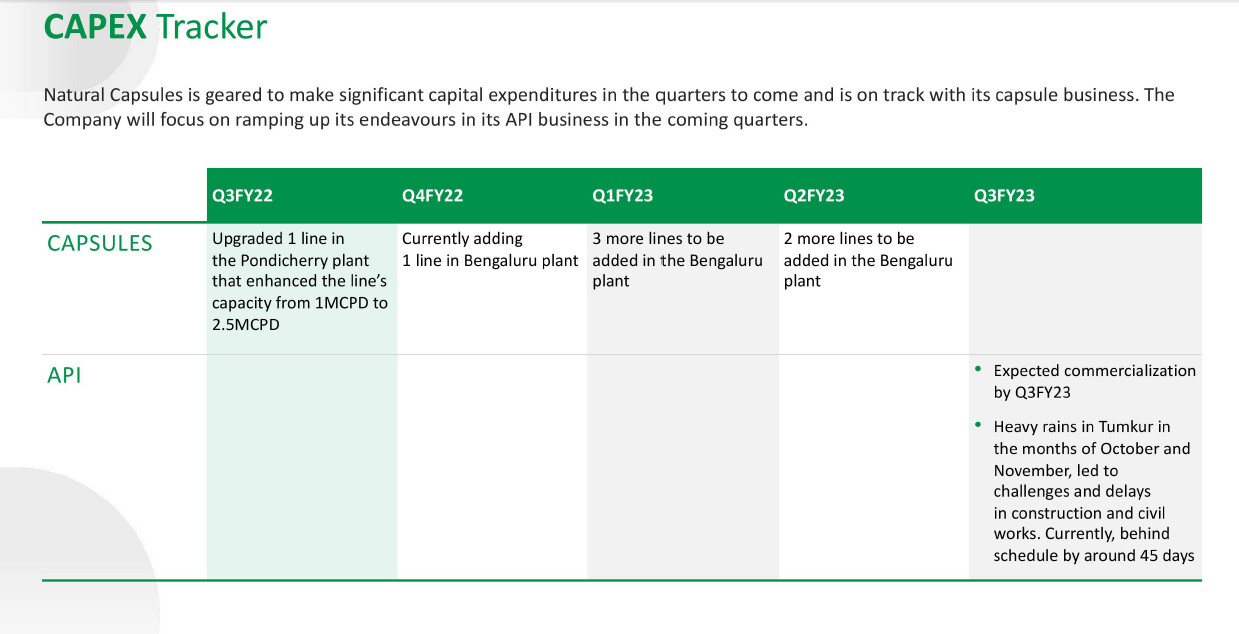

Total 96 cr capex, 48 cr loan @ 6.4% (annual interest outgo of ~3 cr) , 20 cr. internal accruals, 28 cr. rights…payback from PLI, total 67 cr., out of which 20% , roughly 13.4 cr. each in FY23, FY24, FY25, 10% or 10.05 cr. each in FY26, FY27 & 3.35 cr each in FY 28, FY29…IF they execute, this has potential for ~300 cr. revenue and around 45cr. EBITDA generation assuming 15% margins…

Risk of execution in API foray is very huge, if they fail, BS will be badly damaged for the remaining scale of operation. But then Risk hai to Ishq hai…

Share price had a huge run up of almost 4.5x since the company shared their investor presentation in Nov’21. (Have taken right’s allotment also into account for the return calculation)

It feels as if it has run way ahead of it’s publicly known fundamentals. We as small investors would probably be the last to know what’s cooking behind the scene. Like if their API capex is going well or something of that sort which removes the doubt on their execution capability

Disc: I have reduced my position given the huge run up.

I see a huge growth potential in the coming times and I am betting big on their upcoming API products, which are import substitute and probably sole manufacturer of these APIs in India.

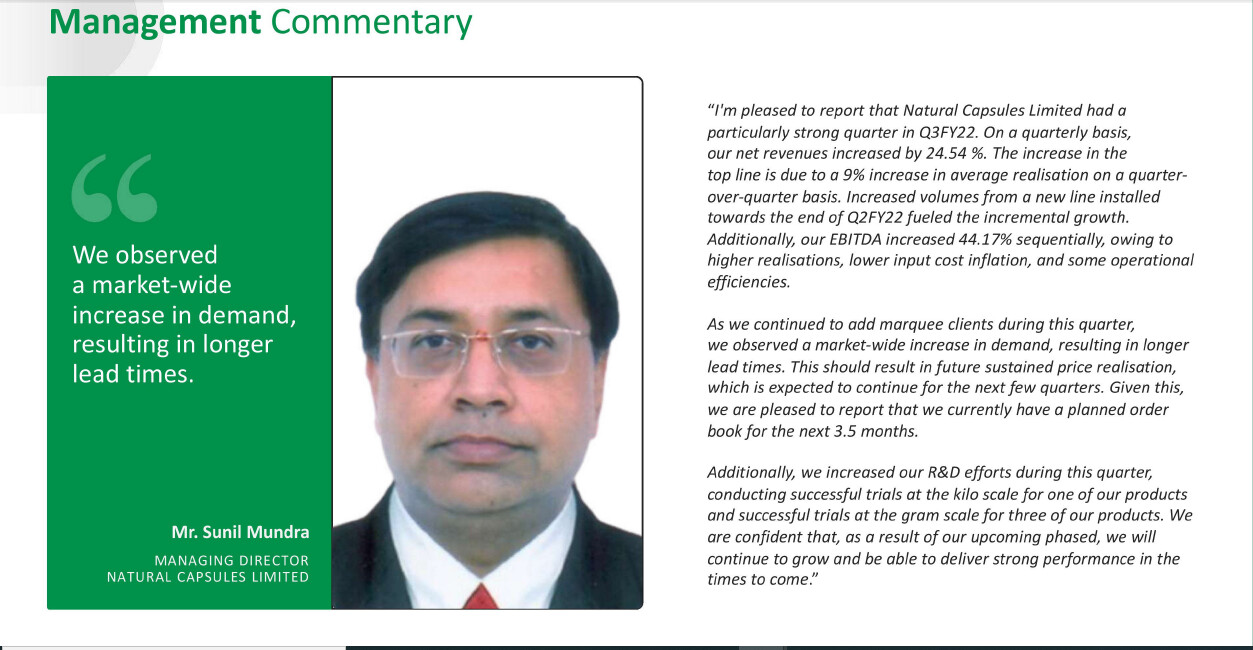

Company has been quiet transparent.Post Q3,they laid out the timelines of capex in their investor ppt.Basically every quarter there will be some incremental capacity addition.Key questions:

→ All time high EBITDA margins sustainable? Inspite of RM headwinds faced by companies across sectors,NC hasn’t faced any issue.In fact,it has seen a margin expansion.Given that the company has been doing 55-58% GMs traditionally a 20% EBITDA should ideally be sustainable.

→ Realisations have definitely risen,how sustainable are they? Can company improve or atleast maintain these realisations going ahead?

→ What is the competition like in the capsule market.What is leading to this kind of strong growth?

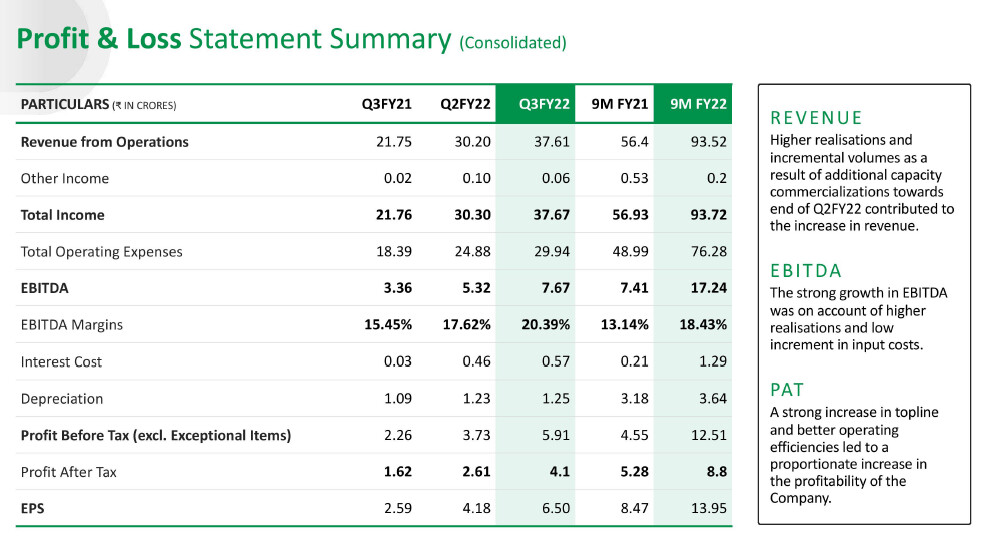

In Q3 company reported 37 cr revenues,there has been qoq growth since last 4 quarters so looking at TTM earnings might not be the best idea.Moreover,since capacity will be coming online incrementally every quarter there is a fair chance that we are looking at a 45-50 cr kind of quarterly run rate next FY.At 20% EBITDA this translates to 36-40 cr annual EBITDA or a PAT of ~20 cr.So at current Marketcap stock trades at 23-25x,not cheap but definitely not out of whack.Bear in mind that in 9 months company will have 80% higher capsule capacity(24.1 vs 13.3 BCPA) so the potential upside to revenues could be even higher.In fast growers,markets usually give a higher multiple.API ramp-up is both a risk and an opportunity but deciphering it beforehand as an investor is quiet tough.But on their capsule biz alone I feel there is enough room for growth.

All in all while the stock run up in short term has been quiet steep I feel it’s backed by earnings and a solid improvement in return ratios of the company.As of today,there are no signs that there will be a deterioration,need to track how they execute.

Disc.: Invested.Views are biased.Do your own due diligence before investing.

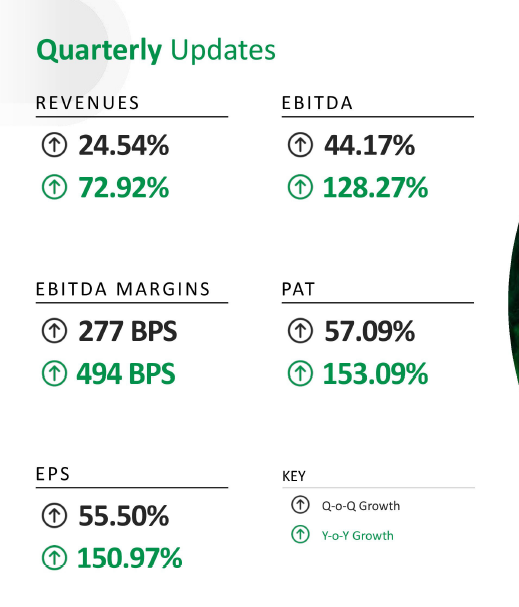

Today the company has declared block buster Q4 results. Revenues, PAT, margins and EPS has seen big jump YOY and QOQ basis. Q4 EPS jumped to Rs 7 from 2.5 a year ago. Full year EPS at Rs.19.5. It appears all round performance on account of increased demand, operational efficiencies, higher capacity utilization. I see a huge growth potential in the coming times as more capacity to kick in and also betting on their upcoming API products, which are import substitute and probably sole manufacturer of these APIs in India.

Discl: Invested at lower levels, views may be biased.

Can someone please throw some light on Rigt Issue declared by the company. The record date seems to be 25th of May.

So If I hold the shares of the co. on 25th, the I would be eliginle fot the right issue? What is the price of the shares offered and when the call money would be asked.

New to the markets and thus don’t have much idea about the right issue process…

@YK_Bu: Rights issues were issued by the company in December 2021 at Rs 100 per share.

These Partly paid (PP) shares are trading in BSE (NATCAPSPP | 890161 | IN9936B01013). On Friday these shares closed at Rs 377. Based on my understanding, one can buy these PP shares, which upon payment of current and future call money will get fully paid shares of natural capsules.

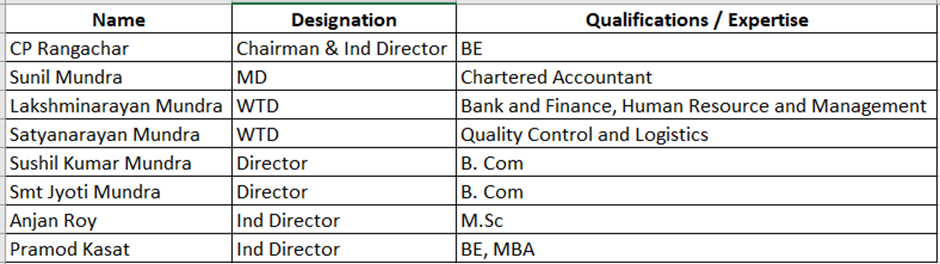

I have a basic question on the diversification into API – where are the skill sets coming from? The Board has 5 members from the Mundra Family and three Independent Directors. The MD Mr. Sunil Mundra – the public face of the company - is a Chartered Accountant. Most of the others also have commerce / finance background.

Only Mr. Sushil Kumar Mundra’s profile says “with expertise in API” but he is a B. Com. by education. He does not seem to be operationally involved with the business.

Of the three Independent Directors, two are engineers.

Only Mr. Anjan Roy is a subject matter expert. His profile says “M.Sc. in Organic Chemistry with 32 years experience in managing large API manufacturing facilities”. However, he does not appear to be operationally involved in the business. He is an Independent Director, earned Rs.45,000 as fees for attending Board meetings and is not eligible for ESOPs either.

The Board of Natural Biogenix Private Ltd – which is executing the project has some of the same people as above.

But the company plans to produce the three APIs using a fermentation based process, a relatively untested process in India. Making API is a completely different matter than capsules, and I presume requires far more technical expertise. Of course, the company can hire scientists and other technical experts. But in such a small company, the promoter needs to be operationally hands-on with the subject matter to take key decisions.

Any idea what expertise the management has in diversifying into these APIs? Or is it that these APIs are relatively simple products?

I have the same concerns about the company and their capabilities. This concern is only aggravated by the fact that they have pushed back the deadline for starting API production multiple times now.

For now, I have contented myself with the fact that they had started R&D into these APIs in 2018. They have already spent a good amount of time trying to develop these APIs. It is not they just applied because of the PLI scheme. And results of their efforts are showing - they are now able to produce 1 API at kilo scale and the other 2 APIs at gram scale. Still, surety will only come once they start commercial production.

Meanwhile, I am pretty happy with their capsules’ business growth.

What i understood from one of the pharmacist, the API which they are proposing is very basic, Cheap and low margin one. Since it is basic and simple chemistry, any company can do if they have required raw material.