As promised, follow up post on some current exciting opportunities and future pipeline (near, mid and long term horizon) across US and RoW subsidiaries:

Natco Pipeline.xlsx (17.2 KB)

US Pipeline:

-

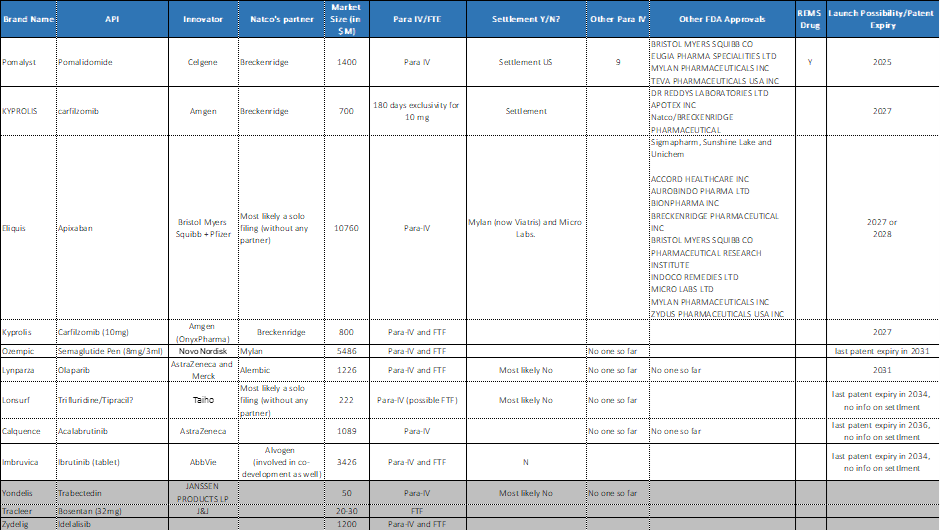

Pomalidomide (Pomalyst) - 1.5B USD market where they do have settlement and expected launch date is 2025. This is an old filing with Breckenridge so margins will be shared between partners. Mylan, Teva, Eugia are other players with US filing in place.

-

Carfilzomib (Kyprolis) - 0.8B USD market. Expected launch date of 2027. They have 180 days exclusivity for 10 mg strength. Other key player in the market are Dr. Reddy, Apcotex.

-

Eliquis (Apixaban) – Real big size drug (within world top 5) even bigger than Lenalidomide, with ~11B USD. Some estimates suggests that first generic launch is around 2027 or 2028. Bad news is that Mylan (now Viatris) and Micro Labs already have settlement with innovator BMS+Pfizer. Even otherwise, close to 10-12 other players are eyeing this tempting opportunity. Therefore, will be hard to capture meaningful share in US market. Natco has picked the right battles, they have started aggressively on this wonder drug in RoW subsidiaries (Brazil) .

-

Ozempic (Semaglutide Pen (8mg/3ml) – Have FTE status. Another BIG and meaningful opportunity however may be riddled with litigation and time delay. US revenue of 5B USD+ for FY’22 for innovator Novo Nordisk. There are no competitors in sight so far. Novo has monopoly position in Semaglutide family of drugs like Ozempic, WEGOVY (solutions) and RYBELSUS (tablets). As a possibility, Natco may look at the other two possibilities as well (there was a very good question around this in Q4’23 concall and management deflected the question smartly).

-

Lynparza (Olaparib) – FTF filling with 1B USD+ revenue run rate. No competition in sight so far except innovator AstraZeneca and Merck. Again, may go through litigation and time delay for prolonged period of time.

RoW subsidiaries:

Canada –

-

Natco has launched PrNat-Lenalidomide Capsules, the first generic alternative to Revlimid to be approved by Health Canada in Sep’21 – . Canada sales is $400 - $500 M. (link)

-

Natco Canada has launched NAT-Apixaban Tablets in Sep’22 (link)

-

Recently (March’23) Natco announced the launch of PrNAT-Pomalidomide capsules, the first generic alternative to Pomalyst. (link)

Australia

-

Pomalidomide - Natco Pharma stated that it has launched first generic version of Pomalyst (Pomalidomide) Capsules in 1,2,3,4 mg strengths in the Australian market. Pomalyst registered sales of $35.6 million in the Australian market for the year ending March 31, 2022. (link).

-

Also, Natco and its partner Juno Pharmaceutical had arrived at a Patent settlement for Lenalidomide and reached out to Australian Competition and Consumer Commission (ACCC) for approval however same lawsuit was withdrawan after some initial critical adverse observations by ACCC. (Link). Subsequently, looks like they have reached some other format of settlement.

Brazil (websiste):

- Everolimus -Biggest success in Brazilmarket. Monopoly position for fourth consecutive year

- Apixaban – First to launch

- Azacitidine - second generic in the market

- Launched Gefitinib - first to launch and the only generic

Market success can be confluence of multiple factors however, this company never fails to amaze with big hairy audacious goals (aspiring and delivering on world’s top 3/5 drugs, repeatedly) and long horizon thinking (7-10 years ahead). Only challenge in our part is to find a way to model such moon shot businesses.

Regards,

Tarun