I am adding my notes from their last 5 annual reports.

FY16AR:

- Has 38 ANDAs with 16 approvals (including 4 tentative approvals); filed 33 DMFs; Expect 10+ ANDA filings over next 2 years

- September 2015 Successfully completed the issue of equity shares for Qualified Institutional Buyers (QIB) subscription with gross proceeds of 340.88 crore

- Launched 3 HepC product; Foreyed into gastroenterology

- NCE program:

o The discovery of new medicines and its success is a long journey, filled with challenges on its way. At Natco, we have been extending our horizons with fundamental research on discovery of new molecules in the anti-cancer segment. We believe there are appreciable synergies coming out of generic research and fundamental research that we conduct in R&D. A compact group of clinical scientists and coordinators are an integral part of the discovery group to design the clinical protocols.

o We continue to work on two key molecules which are in clinical phase studies- NRC 019 & NRC 2694. There are also a string of molecules in the pipeline at the pre-clinical stage.

FY17AR:

- Has 43 ANDAs with 22 approvals; 20 PARA IV filings; filed 37 DMFs

- NATCO ramped up by monetizing on years of effort through the launch of first generic version of Oseltamivir Capsules – in the United States and through strong growth in our domestic formulation portfolio

- We de-risked by expanding further in India including the launch of a new division in Cardio & Diabetic therapy segment

- Launch of Imatinib in EU by TP API customers was one of the key highlights of FY 2016-17.

- We saw an accelerated growth during the financial year due to Hepatitis C product growth in India and blockbuster launch of generic Oseltamivir in the USA

- Wish to invest 6-8% of sales into R&D

- As part of our wider strategy, we launched India’s first generic Bone Marrow Transplant (BMT) product, Thiotepa, as we intend to build a full-fledged BMT portfolio

- 8 product launches in India; target 10+ in FY18

FY18AR:

- Has 46 ANDAs with 29 approvals; 16 PARA IV filings; filed 42 DMFs

- With the long-awaited blockbuster launch of the generic Glatiramer Acetate injection and the generic Liposomal Doxorubicin in the US, in addition to other niche and several first-to-launch products in India

- Copaxone: A resourceful collaboration with a partner resulted in USFDA approval for the generic version of the top selling multiple sclerosis (MS) drug in 20 mg/mL and 40 mg/mL dosages. In the same month, through our marketing partner, we launched Glatiramer Acetate injection of 40 mg/mL (a 3-times-a-week injection) and 20 mg/mL (once-daily injection) in the US. The Glatiramer Acetate injection is a key launch for us as we have invested over a decade in seeing it fructify

- Received approval for another complex product, the anti-cancer drug Liposomal Doxorubicin hydrochloride injection. It is one of the most complex drugs to manufacture. We accomplished the development of the product in-house with guidance from our co development partner. This is the 1st complex drug delivery system

- Lanthanum Carbonate, an inorganic compound with high quality standards, was also launched in the US market as a generic equivalent and is indicated to reduce serum phosphate in patients with End Stage Renal Disease (ESRD)

- After a decade of labor led by our robust R&D strengths and resourceful collaboration with our marketing partner, in FY 2017-18, we launched our first Glatiramer Acetate injection of 40 mg/mL and 20 mg/mL in the US.

- US revenues continued to grow with successful launches of first-time complex generics and the success of our blockbuster product, Oseltamivir Phosphate

- Our agreement with Gilead Sciences Inc., Medicines Patent Pool and Bristol Myers Squibb allows us to expand access of our Hepatitis portfolio in 112 developing countries.

- Launched 7 products in India in 2017-18; 3 of which were first to launch in the country

- Our specialty pharma segment witnessed some corrections owing to price erosion and thereby reduction in market size of our Hepatitis C product basket

- Oncology: Our six flagship brands — Geftinat, Erlonat, Veenat, Sorafenat, Lenalid and Bortenat — recorded annual sales of over 100 million each in FY 2017-18.

- Cardiology and Diabetology (CnD): In the year under review, we launched two niche products in this segment, Arganat and Dabigat, which are first-time launches in the Indian market.

- In FY 2017-18, we raised around 9,150 million via a Qualified Institutional Placement (QIP).

FY19 AR:

- Has 51 ANDAs with 36 approvals; 20 PARA IV filings; filed 45 DMFs

- NATCO has seen strong growth in the oncology segment in India and through our high barrier-to-entry products, Liposomal Doxorubicin and Glatiramer Acetate in the US; Some of our key products in the US have seen strong competitive pressures while in India, we have seen market size reduction in the Hepatitis C portfolio

- We filed 5 ANDAs in the US, of which we believe three are potential first-to-file products. We strengthened our pipeline through the filing of Ibrutinib tablets which we believe to be a large potential opportunity for the company

- We have benefited significantly from the sale of Oseltamivir during the past two years with an expected decline in revenue in the coming years due to increased competition and price erosion.

- Number of generic players have significantly increased in US which adds to the tough pricing environment. However, list prices of recently launched drugs, especially in the specialty, orphan and oncology areas are often at higher prices.

- We have demonstrated our ability to handle different manufacturing processes, such as lyophilisation and complete isolation technology to manufacture cytotoxic products; During the past several years the Company has carefully chosen to enhance certain capabilities into new manufacturing techniques such as spray drying and hotmelt extrusion technologies to enable novel solid dispersion methodologies

- R&D diversification: Create multiple products, combination products and innovative dosages; The Company has continued to advance its technology platforms of peptide chemistry and liposomes, with an intent to diversify its product portfolio; the company has also added novel solid dispersion technologies

- Fixed-dose combination (FDC): A combination drug is an FDC that includes two or more active pharmaceutical ingredients (APIs) combined in a single dosage form. While these are more complex to manufacture, they ensure increased compliance by patients and result in lower side effects. During the year, we launched an FDC of Sofosbuvir-Daclatasvir tablets to treat Hepatitis C under the brand name Hepcinat Plus and an oral fixed-dose combination of Sofosbuvir and Velapatasvir under our brand Velpanat.

- Expanded oncology portfolio through launch of 2 new products and non-oncology segments through 4 launches

- Has 6 oncology brands - Veenat, Lenalid, Erlonat, Geftinat, Sorafenat and Bortenat- which have recorded sales of over 100 million in FY 2018-19.

- Net revenue from cardiology and diabetology segment was <10 cr.

- Launched 6 products in India during the year; target to launch 6-8 products a year

- Launched its first generic version of oral tablets Teriflunomide for Multiple Sclerosis in India; and generic Posaconazole injection, available for the first time in India

- Has ten brands in excess of 100 million revenue in the domestic oncology and pharma specialty segment

- We have worked on increasing our capacities across various units and have spent 4,413 million on it. Our new plant at Visakhapatnam is operationally ready and will commence operations in FY 2019-20.

- During the year, we announced a buyback and purchased about 30 lakh shares worth 1.86 billion

- Crop health sciences: We are targeting a unique set of molecules for the Indian market, which have a potential to expand to other regions

FY20AR:

- Has 51 ANDAs with 36 approvals; 20 PARA IV filings; 39 active DMFs; 49 cumulative DMFs filed

- US business:

o Faced pricing pressure and competition for antiviral flu medicine Oseltamivir

o US revenue growth came from Glatiramer acetate and Liposomal doxorubicin, aided by a strong exchange rate

o We also observed a more stabilised pricing scenario in the US market

o In addition to having a strong supply from our manufacturing base in India, we associate with strong partners in the US, some of them with local manufacturing presence, which positions us well for expanding our business - Our API manufacturing capabilities include multi-step synthesis, semi-synthetic fusion technologies, high-potency APIs and peptides

- Launched 8 products in domestic market out of which four were first-to-launch branded generic products; 5 launches in cardiology and diabetology and 3 in oncology

- FY 2019-20 has witnessed significant improvement in the cardiology and diabetology product segments with sales doubling against those recorded in FY 2018-19

- Target 8-10 launches in India each year

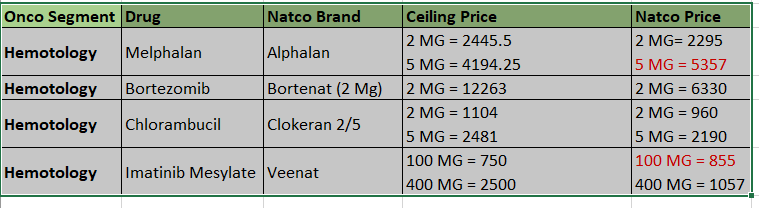

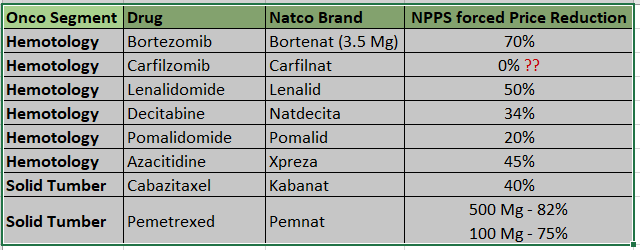

- Our oncology segment suffered due to pricing controls from the National Pharmaceutical Pricing Authority (NPPA) impacting margins along sales channels and our Hepatitis-C business continued to decline due to reduction in market size. On top of this, during Q4, COVID-19 outbreak resulted in cancer patients postponing their hospital visits and chemotherapy procedures affecting the sales of our oncology medicines

- We have a portfolio of 33 brands across two segments: hematology (14 brands) and solid tumors (19 brands). We intend to build a full-fledged Bone Marrow Transplant (BMT) portfolio in India and have already launched Thiotepa, India’s first generic BMT product

- Apigat (Generic Apixaban) is a drug used in the prevention and treatment of blood clot. The drug is safer than other anticoagulants without the side effect of gastric bleeding

- We launched a combination drug Vildanat M (Vildagliptin and Metformin) for diabetes, which has considerable potential to achieve better blood glucose control and improve therapy compliance. This is a first to launch product

- Incurred capital expenditure of 3,492.85 million, a majority of which was used to enhance our capabilities in our manufacturing facilities. A significant portion of this capex was done at our Vizag facility. The remaining part was primarily used in our formulation facilities across the country.

- Crop health: The greenfield project in Nellore district of Andhra Pradesh is close to completion and expected to be commissioned in FY 2020-21. We have disclosed one key product, Chlorantraniliprole (CTPR) and plan to launch other unique products which will be a part of the Integrated Pest Management (IPM) solutions

- In Brazil, majority of sales are institutional or government sales

- Our capabilities span synthetic chemistry of small molecules, peptide chemistry, oligonucleotides, nanopharmaceuticals and new drug discovery

- With the environment in mind, we have improved our capability in solid dispersion technology and built efficient processes that use less solvent. Our manufacturing with hot melt extrusion is one such example

- Over the past few years, we have placed more emphasis on increasing our network of third-party suppliers in addition to our own backward integration. This has enabled us to target more complex processes with significantly greater number of steps to manufacture

- Doesn’t hedge currency risk (consistently through annual reports)

- Capabilities:

o Glatiramer acetate: A complex peptide used in the treatment of multiple sclerosis is manufactured with specific controls of critical process parameters, enabling us to produce quality product effectively The finished dosage, sold in pre-filled syringes, is an example of developing a complex API, tying up with manufacturing partner and drug delivery device provider.

o Liposomal doxorubicin: The liposomal-based product delivers the medicine in a targeted manner. Liposome drug products are complex formulations where physical and chemical stability is vital, including the need for sophisticated physicochemical testing and very narrow particle size management

o Hepatitis-C portfolio of products: The Hepatitis franchise of molecules require to be made suitable for dissolution for increased bioavailability, which is achieved through our our internally optimized solid dispersion process. The bioavailability of APIs depends on its solubility in water. Making water-insoluble drugs more soluble presents a significant challenge in drug development. Hot-melt technology is a proven method for bioavailability enhancement of poorly soluble APIs.

o Lanthanum carbonate: We are the only generic player for this product. The novelty is in the API development of a stable dihydrate form of an inorganic salt for use by patients with end-stage renal disease. The technology breakthrough and IP together have made it possible for us to launch this molecule, accessed mainly by geriatric patients.

")