They did sell 14 acres earlier this year to microsoft for some 114 crores… So empirical evidence is there… Whether they have sold/disposed in earlier years since after the article was written I am not aware

3 Likes

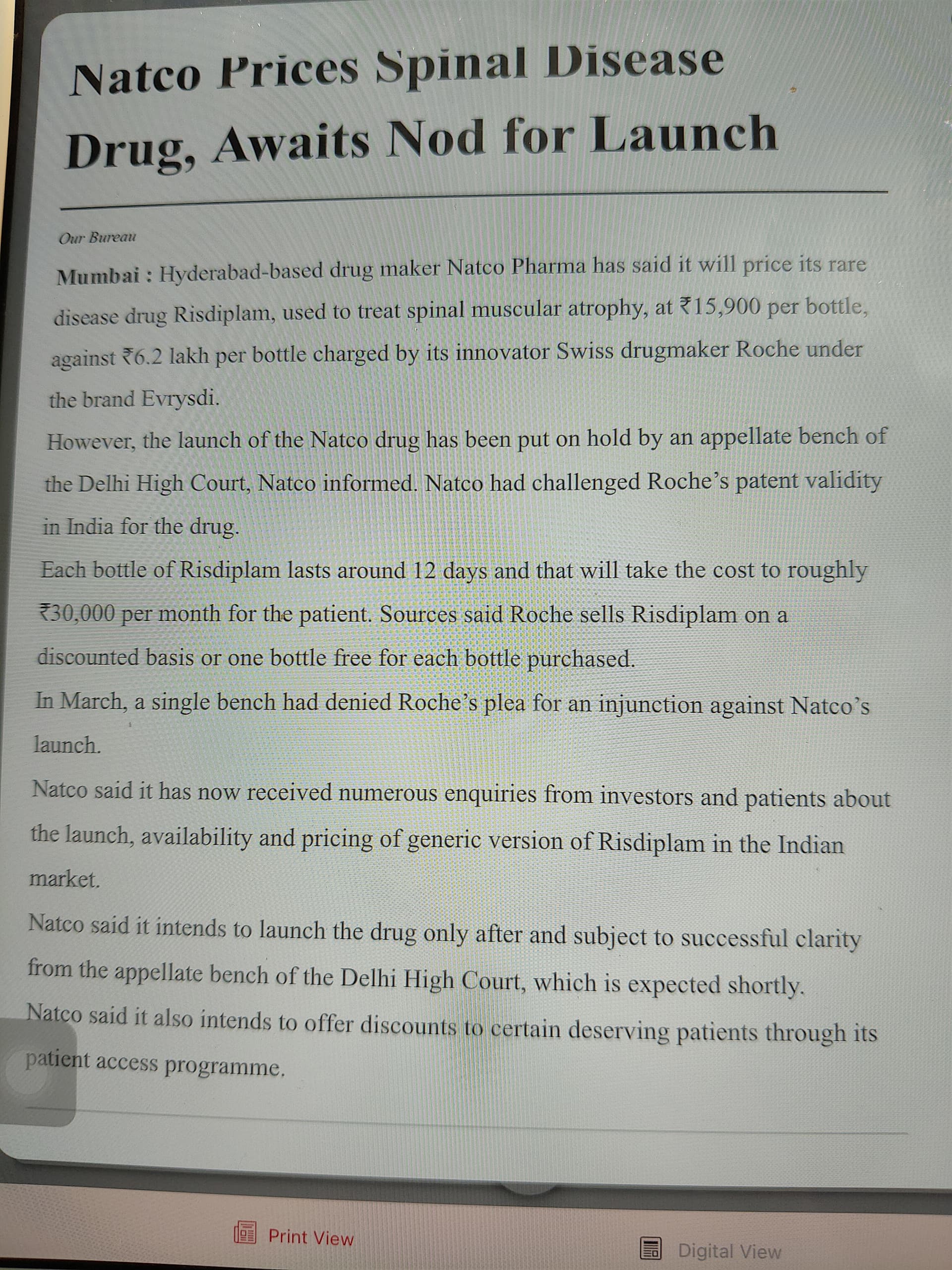

Natco has been fighting many of the patent protected drugs in India for domestic launches… most of them do not move the needle for domestic formulations business for Natco Pharma and only bring the cost down significantly for the patients.. Risdiplam as well, the number of patients needing the treatment is very less, thats why Roche has been able to price it the way it has, it is quite a rare disease in terms of volume of patients … and if Natco gets favourable judgement, the price at which it will market the drug will not make it earn anything significant in terms of its present market cap or annual sales..

more recently, the CTPR agro chem battle with FMC Corp is significant for the crop science division of Natco Pharma…

I was just thinking something aloud.. and wanted to put it here for broader discussion…this looming tariff thing that US may or may not impose on pharma imports from India.. how will it affect gRevlimid imports? Natco must be exporting at a predetermined cost + mark up formula (which is extremely low relative to the sale price of gRevlimid in USA) and it is the 30% profit share that get repatriated back to it .. therefore, tariff will only impact the import value and not profit share repatriation to it, isnt it? Tariff impact wont affect gRevlimid USA business for Natco in the current year is what I am concluding…due to most of the money coming from profit share

9 Likes

Having a lumpy business of Natco pharma, what should be the mindframe of long term investor? It is roller coaster ride running parallel to the ground for few year. when will Roller coaster rides toward upward is very difficult to predict? I think for making money in Natco, one needs lot of luck with great patience. Both are must for Natco long term investor. Disclaimer: Holding and biased.

2 Likes

I believe one has to look at it as a cyclical business, much more like a commodity like sugar or metals, where the classic cycle goes down for some time and then upticks, which in this case has been big opportunity drugs like Copaxone, Revlimid and Semaglutide/Ozempic in the coming years

One has to keep reasonable expectations from the company in terms of earnings for at least 1-1.5 because, anyway, post Mar 26, profits will be dented due to Revlimid, which has been a classic in NATCO’s story in the past until Ozempic or any other drug becomes a hit.

If you understand the business and are ready to wait for the next cycle (which has a defined tentative timeline if the approvals come on time, which has been pretty much the case in past), accumulating the stock at these levels is a decent opportunity in value terms, probably.

4 Likes

Can you please throw some light on this? What would lead to this profit dent? Is there an expiry of some agreement or something like that that is set to happen?

1 Like

Because the gRevlimid patent expiry will happen at that point in time, leading to massive price erosion due to the open market for other players to enter, impacting the company’s overall margins

2 Likes

Race to semaglutide is going to start. It seems Dr Reddy and Zydus are heading the race. Natco seems to be not interested much as it’s not suit it’s business profile.

3 Likes

For the geeks who like to get into the nittiegritties.. the master purchase agreement between Teva and Allergan Plc..

The clause 2 therein and it’s sub clauses covers US lenalidomide sales, Natco Agreement and the modality of the declaration of Earnings report by Teva for the lenalidomide sales and it’s verification procedure etc. as well as settlement of counter party claims…

Natco has an indirect association with Teva through this master purchase agreement which mentions Natco Pharma lenalidomide agreement (probably with celgene)

It is moot now as only 3 quarters of windfall profits remain … Just sharing for theoretical knowledge

10 Likes

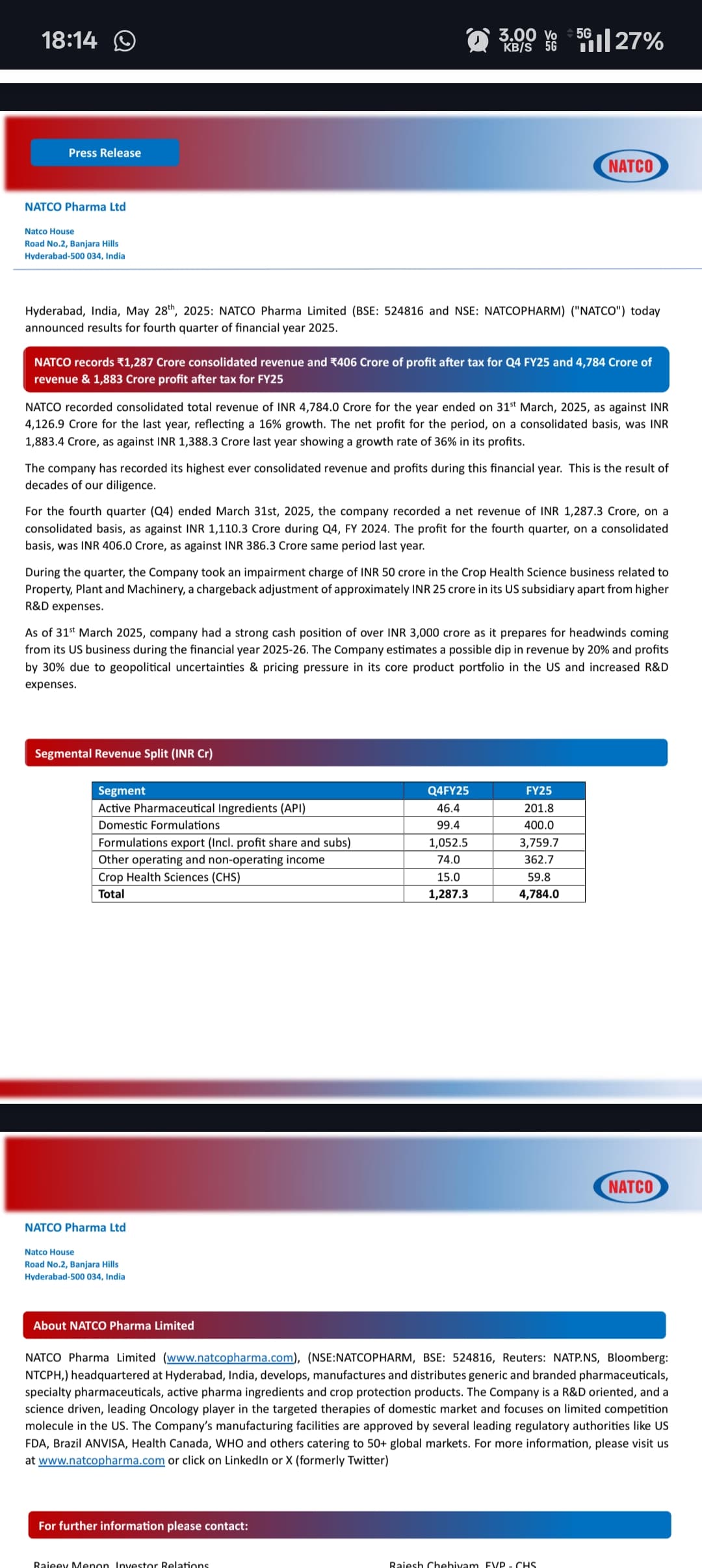

Disclaimer: Results are out and seems quite satisfactory. There is no point in comparing them with last quarter as it was disastrous one. In comparison to last second and third quarter results eps seems to be quite down. Reason for same might be pricing pressure from revlimid.

Let see what management says tomorrow on concall at 11 am. Read the last few lines of press release and it tells all about management integrity and sheer honesty. Business can be here and there quarter on quarter but such commentary makes them class apart.

Holding & biased and it seems some day Natco day will come.

4 Likes

there doesnt seem to be gRevlimid pricing pressure… they took a 75 crore hit this qtr for other reasons than lower pricing of gRevlimid + higher R&D as stated in the press release ..

Good show and good clarity by a straight forward management.. wish they stop burning cash on the crophealth division.. a 150 crore annual loss on 50 crore revenue is pathetic

7 Likes

gives god details https://www.bseindia.com/xml-data/corpfiling/AttachLive/d43e2593-6819-4d99-b9a6-c3019c901490.pdf

mgmt is very conservative - whether on projections , estimates or impairment.

even with the guidance of 30% lower profit and 20% lower revenue there are possibility of couple of postive surprises eg India business , Semaglutide and one more molecule.

plus 3500 crore cash as warchest . at CMP still a decent bet

3 Likes

why is Natco Working capital so big does not come under control.

1 Like

I think working capital managment is a lot more imp than an absolute number of working capital

The number looks inflated usually beacuse whenever a new drug comes up they have to get the capacities at full throttle and make excess of it so that they can meet the excess demand coming from the market which impacts the Inventories

The receivables tends to go up beacuse of their partenships with foregn pharma companies which elongates the recivables cycles

Licensing & Partnership Models is one of the being reasons cash is collected after partner collects from distributors in froeign country

But that is not a very stressful case just beacuse the cash on balance sheet is healthy which can fund the working capital requirements if something goes bad

3 Likes

NATCO PHARMA:

Mistakes I Made While Investing

- Invested at the peak of the sales cycle due to FOMO.

- Didn’t dig deeper into the financials, which on the surface looked very strong—low P/E, high growth, good ROCE and ROE.

- Didn’t realize that Revlimid sales were a one-time boost, contributing 50–55% of revenue and 70–75% of EBITDA.

- The agrochemicals business is currently operating at a loss.

- Overall financials are expected to deteriorate going forward.

- Not a good investment from a 3-year perspective since sales were at the top of their cycle when I invested.

- Very high cash conversion cycle, which could hamper growth down the line.

- If you exclude Revlimid sales, the P/E ratio spikes to around 55 and ROCE drops to 13–15 at all-time high price levels.

Lesson learned: Always look behind the headline numbers to understand what’s driving them. If growth is due to a one-time factor, exclude it. If it’s sustainable long-term growth, then it’s safer to go all in.

20 Likes

Natco Pharma isn’t a bad company, but its business is lumpy, with heavy R&D investment and volatile results. This doesn’t align with my investment style, which favors stable and predictable companies.

I made a mistake by not fully understanding the business before investing.

Disc: I have exited my position and booked a loss

7 Likes

In the recent concall Mr Rajeev saying that he will close one acquisition by end of this FY or end of CY that will increase base business and sustainable revenue for the company. In addition to that from 31st Mar 2026 semaglutide will be launched in India both BtoB and BtoC format. Based these statements I feel that down cycle and market pessimism will come down. But all in all how he will execute

- Good acquisition

- Scaling of semaglutide sales

- Turning around Crop science business this year.

I hope at least 2 factors come true in this year.

Discl - Invested and biased.

7 Likes

Hi Madhavojha,

Thanks for your post, Can you please help in understanding the numbers for 55 P/E and PAT assumption of around 300 Cr post revlimid.

25% of FY25 profit is 470 Cr (assumption of 25% EBIDTA/ profits are from Non-revlimid businesses) valuing company at 33-35 P/E post revlimid.

Disclosure: Invested and Biased.

4 Likes