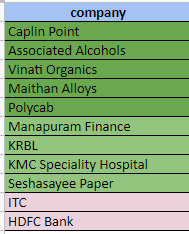

I have started to build a portfolio 6 months back to create wealth over the long term. I started SIPs in MF from 2017. Now I have all my MF holdings in Parag pargh multi cap fund with active SIP. Also i started to learn investing &markets from 2017 and chose the below stocks based on my knowledge &conviction.

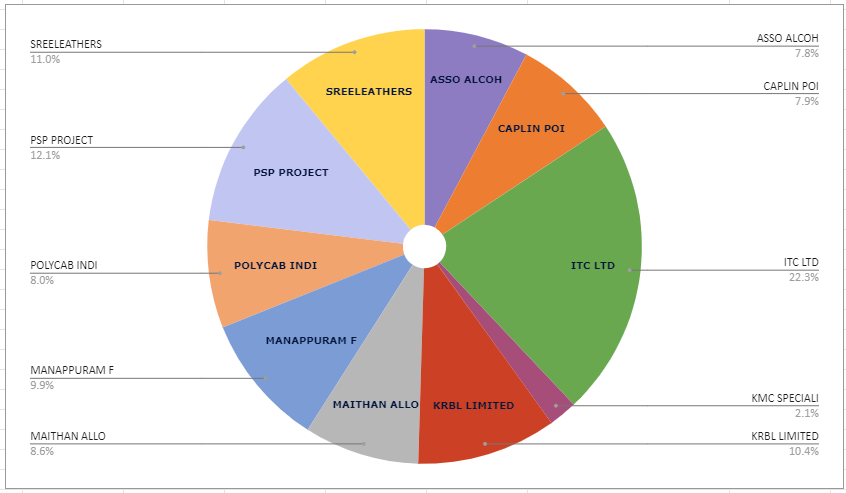

Allocation:

I have 63% cash and rest of the money in this portfolio as of now. I am slowly buying these stocks for past 6 months as there is no clue where markets headed and open to buy more if any downside.

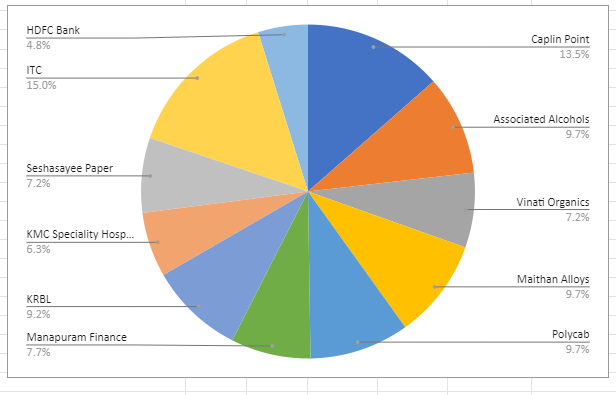

I will increase ITC allocation to 25% and HDFC Bank to 8 or 10%

Applied for Happiest Minds IPO

I have some other stocks in my watch list and waiting for low levels to enter and don’t want to have more than 16 stocks

I dont prefer stocks with high PE

I choose stocks based on,

growth in either profit in PNL or cash in Balance sheet

Reasonable price

Reliable management with good industry knowledge &experience

Please feel free to share your thoughts on this portfolio.

Vinati, ITC, HDFC bank and Polycab are definitely excellent for long term as well as short term., PPFAS LT is also a very good fund. It will be interesting to see how this fund position itself in the light of recent SEBI circular.

PPFAS multi-cap is one of the MF which can satisfy the new sebi rule better than its peers(some of the peers might merge with large cap). PPFA need to increase 12% in small cap to adhere with new rule. They can adjust that in either India/US market. Lets see.

Pardon me the nativity, but does the 37% you are invested into also include your mutual fund corpus ?

If it doesn’t then I believe it’s more reasonable to calculate the cash percentage including that. I follow that approach because I think that money is every bit a part of my overall portfolio as any other.

Yes, I am following on KRBL’s current case. If there is any price drop, I will add more as long as their profitability remains good. I am expecting decent(not extradentary) growth in long term.

I like CaplinPoint:) Though its not a leader, it satisfies most of the parameters which I consider.

usually beats their sales &profit YOY.

high ROE with no debt

Good promotor

I will stay with Caplin as long their profit growth is intact.

management’s capability in business and successful model

Debt free and cash rich (almost 50% of total assets is cash)

Consumer business

cons:

Risk related to Promotors communication, interest and reliability in sharing profits

Expectation:

Decent growth in EPS with re-rating can give good returns in long term.

Promoters increasing their shareholding to 75% by buyback which will complete in current quarter. Once its done we can expect the below cases

Normal case: Continue the same/decent growth and increase the cash (I don’t find any meaning in increasing the cash for very long time which they have done already)

Best case: Management may start to give dividend and/or expand business from Cash

Worst case: Management may further plan to delist due to low valuation for prolonged time (we can expect the price at least 160 in this case)

I don’t find any downside in all these cases until their business is profitable.

Managements capability of executing projects (my confidence will increase on completion of SURAT DIAMOND BOURSE which is delayed by 1 year)

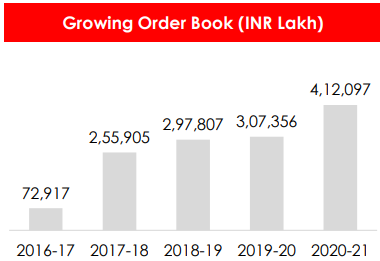

Growing contract order book

Balance sheet is pretty clean especially when I compare the borrowings with peers in construction industry

Stock is reasonably valued (20PE for 22 EPS, earlier PSP posted topline as 35 EPS)

Risks:

Most of the contracts are from Gujarat - I don’t think anything to worry on this

Government contribution towards order book is more (around 60% of current order book) - I couldn’t verify how political change could impact the government order flow to PSP(winning bids for govt projects)

Industry risks and covid lockdowns. They pass the material cost fluctuation to customers

Profit margin is not so attractive at this point. Growth is mostly driven by increase in order book. Company growth is directly related to economy.

profit for 2020-21 was impacted by Covid lockdowns. I will keep it in my portfolio as long as company shows decent growth.

I made few trades in last few days. Actually trying to avoid looking at broader market valuations and only focusing on my portfolio and watchlist.

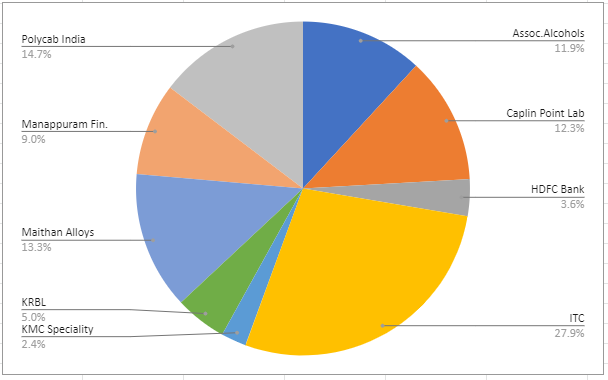

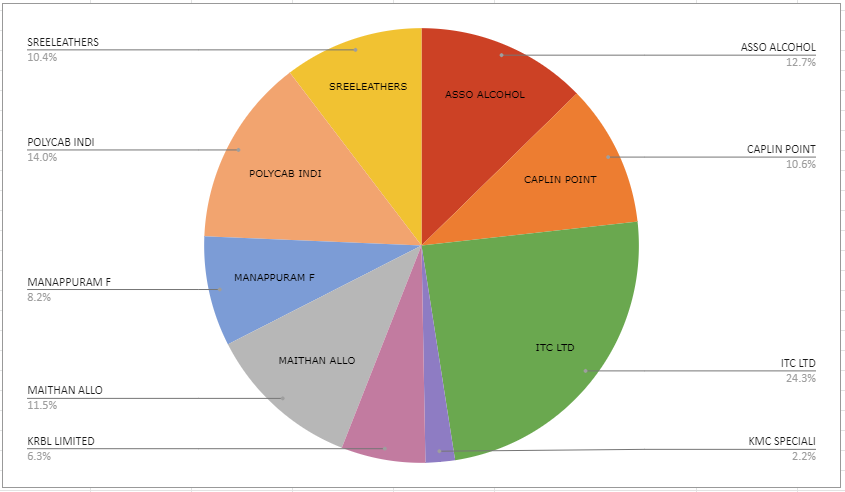

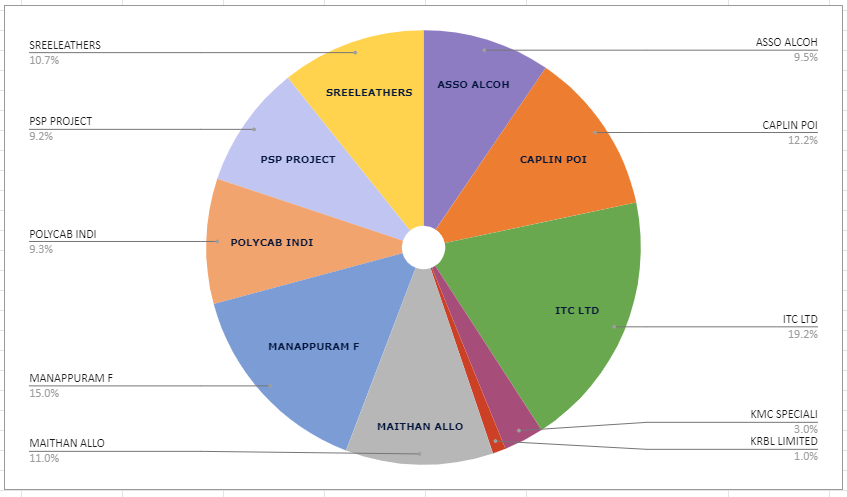

Sold most of the KRBL positions and bought Manapuram, Associated Alcohols and Caplin. I will again consider KRBL in case if it goes below 200.

Increased positions in Sreeleathers and ITC. Actually I feel little comfortable to buy Manapuram, Sreeleathers and ITC at current valuations (though not very attractive)

Fin/Fintech is one my favorite area in which usually companies makes good profit with less Capital and distributes great payout. However I am not conformable with current valuations of these companies (like cams,cdsl,hdfc amc) so just watching. ICICI Sec looks reasonably valued out of this.

I am considering to take a position in ICICI Securities for long term but still not comfortable since stock price would reverse if market turns. So I am just thinking to take small position now and increase it later. I will share my rationale of ICICI Sec in case I buy.

@manoopatil - Below is my rationale behind Associated Alcohols

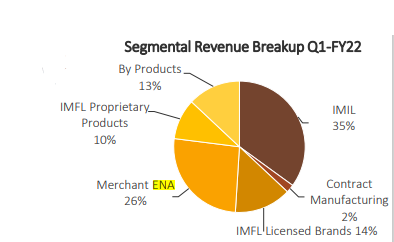

AABL is producing IMIL, IMFL(licensed) and ENA in a single manufacturing unit from MP which is one of the largest manufacturing liquor unit in India.

Revenue streams:

Positives:

Company is in liquor sector which is expected to grow at CAGR of ~7-8% India

AABL is still small and management already shared the expansion plan till 2023. We can expect a decent growth to continue in coming years

Good balance with zero/negligible debt

Promoters have good experience in industry and also have a good track record of capex expansions

Current Valuation looks reasonable for me

Concerns:

It may not get the great margins - apart from own brands all other income streams(ENA/contract manufacturing) has limitations in margins

License renewal and cost could impact the business

All regulatory concerns related to Sin/ESG sector

Concentrated sales- Most of the sales comes from MP and Kerala.

Promoters credibility is not proved yet (I don’t see any major concerns for investors)

Same promotor runs one more liquor company(MEBL) as separate which produces beers. so AABL don’t produce and no plan to enter beer market

Single manufacturing unit which is growing bigger with expansions… Management considers this as a positive because they are able expand the capacity without increasing labor and also in latest concall they mentioned in future if needed they may start small unit in south

Overall I am expecting decent and continuous growth in sales and profit in long term.

Taking a position in PTL Enterprise, bought small quantity today and going to slowly build a position.

I am considering it as REIT a kind of investment with other some advantage,

Around 20 acre land at Kalamassery, Kerala with building is a major asset for this company and it has been leased to Apollo Tyres from 1995.

As per the current lease contract Apollo Tyres to pay 63cr (6 EPS) yearly from 2021-30. Its possible to revise the contract earlier 2030 like they did before.

Land worth is 568cr as per 2016 valuations(without haircut) and its not revalued after that.

330cr market cap company generates around 40cr PAT consistently

Company owns 1.61% stake in Apollo Tyres and its keep on accumulating.

Investing 1 rs in PTL share is indirectly owns 60 paise worth of Apollo share(I consider it as bonus/free)

Currently dividend is 2.5 rs (5% as per CMP, out of 6 EPS) and its expected to increase

Promotors own this property for very long and there is no pledge in promoter holdings.

Director of this company Neeraj Kanwar is part of Apollo Tyres board and one of the key person.

Risks:

Concentrated asset in one location and more depends on Apollo tyres business

Company has a 52 cr of borrowings and 126 cr deferred tax and few other liabilities (I feel its manageable and doesn’t have much negative impact)