Could you share your reasoning on investing in these stocks?

For ex: Balmer Lawrie Investments doesn’t have operations of its own, rather just holds Balmer Lawrie Company shares and hence depend on Balmer Lawrie for any growth. That company is far too diversified for growth in 1 of their segments to make a significant impact on the growth of the stock price. Could you share your opinion on the growth driver in Balmer Lawrie Investments?

@alokinvestor Just sharing my views on the names you mentioned. Since you are new here, I would recommend you to read the individual threads for these companies you shared to get more information/views.

PFC is definitely a good one if you don’t have any expectation on market price movement and happy with the dividends (I think would increase slowly). It may be valued better at some point of time. I found many people value this stock by comparing with FD returns:)

I don’t track GSPL, Bengal Assam Company Ltd

Balmer Lawrie Investment Ltd - Holding company of Balmer Lawrie & Company Ltd. I tried to value this multiple times since its interesting by looking at the assets and price discount to that:)

But I am not sure how efficiently these assets are managed for their diversified businesses. It was very difficult for me to predict the growth &future.

Cupid - It was in watchlist for sometime. Good one with growth factors. If it gets FDA for female condoms, it will become a next level trigger which may take long time to know that. You may need to keep on monitoring their order book because their major revenues comes from big government contracts and it has to sustain.

You didn’t mention what is your goal/expectation with this portfolio. In general portfolio with more dividend yielding stocks with lesser growth factors may looks safe but it won’t help to create wealth in long term .

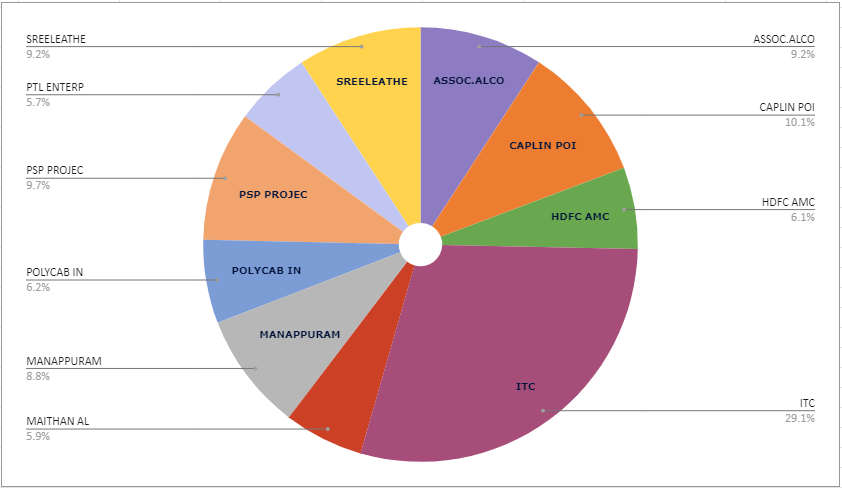

@sumitjain0014 Manapuram Finance:

My investment in manapuram was medium to long term by considering if the growth aspects and results is intact

I picked Manapuram over Muthoot based on valuation though Muthoot looks like bit better in quality and only in gold business

Positives,

The most familiar and reputed gold lending company in India

Great long track record of management in this business

Attractive valuation for the current growth

Diversified into non gold business - Its subsidiary Asirward micro finance is slowly growing and Manapuram also into Home finance and insurance

Concerns:

Management capability on adapting and driving the business with new age competitors and other banks. Also succession planning is not at satisfactory level

Gold is a cyclical commodity

Management is relatively new in non gold business

Gold lending is centuries old traditional business however its future over long term is still questionable.