I am excited to be part of this community and would like to take this opportunity to share how my portfolio has evolved over time. I am seeking feedback and suggestions on how I can further refine and optimize my portfolio. Moving forward, I plan to provide monthly updates on any changes in my portfolio.

Current Portfolio Allocation:

Stocks & Mutual Funds: 25.74%

Cash: 36.8%

Gold: 3.26%

Cryptocurrency: 0.36%

Real Estate: 33.84%

A Brief Introduction:

Education: PhD in Mathematics, currently a postdoctoral researcher.

Interests: Research and teaching.

Investment Experience: Began investing in 2020 with a long-term horizon of 30+ years. While I stay informed about market movements daily, I am not an active trader.

Age: 29 years.

SIP and Lump-sum Investment Strategy:

Weekly SIP: ₹2000 each in Nifty50 Index ETF, Parag Parikh Flexi Cap, and Quant Small Cap (with a 10% annual step-up).

Additional Investments: Opportunistic investments in stocks, smallcases (Value & Momentum and Growth at Fair Price).

Gold & Silver ETFs: Purchased with surplus cash.

Insurance Coverage:

Health Insurance: Provided through my employer.

Family Health Insurance: Separate coverage for my family.

Term Insurance: Currently not availed as I do not have dependents.

Immediate and Long-Term Goals:

Marriage: Planning to marry within the next 1–1.5 years (age 30-31).

Home Ownership: Aiming to build a home in 7-8 years, around the age of 37-38, with the goal of fully owning it by age 40.

Retirement: Aspiring to retire early, between the ages of 45-50.

I look forward to any insights or suggestions the community may have on how I can better manage or adjust my portfolio to achieve these goals.

Though your investments appear a bit diversified, your 25.74% exposure to risky assets i.e. stocks and mutual funds is difficult to comment on, unless you disclose the details and the thesis behind your choice.

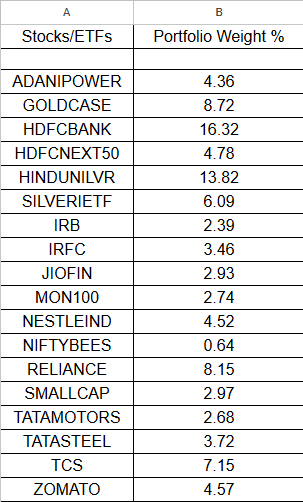

Other than that, I have invested in two Smallcases (Value & Momentum and Growth at Fair Price) and some MFs which accounts for 10.56% and 3.57% of my total portfolio, respectively.

So the total is 11.1% + 10.56% + 3.57% = 25.23% of my total portfolio.

The remaining 25.74% - 25.23% = 0.51% is in US Stocks (Tesla, Meta, Microsoft, Apple and Amazon).

Holy cow I’m in a very similar life position as yours but its just that my asset diversification and goals are a little different. Planning to follow your thread.

This exposure looks fair to me considering your long term horizon and end goals. However, a word of caution on any further exposure to Adani / Ambani stocks. Likewise I think you have excess position in HDFC bank.

Also think about incorporating few good ones, wherein government is pushing locally and which has good potential going forward (such as green energy, defense, semiconductors etc.)

Above are my personal views. Take informed decisions.

My real estate investment is just a plot of land, which is in a good location. I am betting on the overall development of the neighboring areas and the connectivity which will help in increasing the valuation in the future.

Thanks for the suggestions. Yes, I also observed that my exposure to HDFC Bank is quite high, which is 16.32% of 11.1% of my total portfolio, i.e. 1.81% of my entire portfolio. I have not purchasing anymore of it, but will buy other assets, so that its % comes down. I don’t sell things, since I am focused on long term, except re-balancing the Smallcases quarterly.

I think defense sector has already given a run-up and quite skeptical in making new investments in that sector. But I want to explore sectors like AI, green energy, semi-conductors, waste management, and other upcoming areas.

Can you suggest some companies or MFs which I can look for educational purposes?

I think it is good that you are sitting on the cash. To me, the markets are looking for a reason to correct, during which your cash can go to the new sectors that I have mentioned in my previous posts.

I think gradually exposure to equities as percentage of overall portfolio can be increased. You plan to buy a house in probably next 7-8 years which will again skew your asset allocation as real estate heavy, like most of us….but as one of you major goal is retiring early….that would need greater asset allocation to equity and also lot of hard work in understanding yourself as investor. The sooner you get that clarity the better….

1.8% allocation to one stock of overall portfolio is nothing.

I would suggest to complicate things little less, you can remove your real estate land from overall allocation as you currently do not own a home and you can consider it as proxy home. That ways the rest liquid portfolio would present you with allocation percentage of that part of your portfolio which will compete with other relatively more liquid financial assets.

Above thoughts are only for learning purposes and I can be wrong in all my assessments.

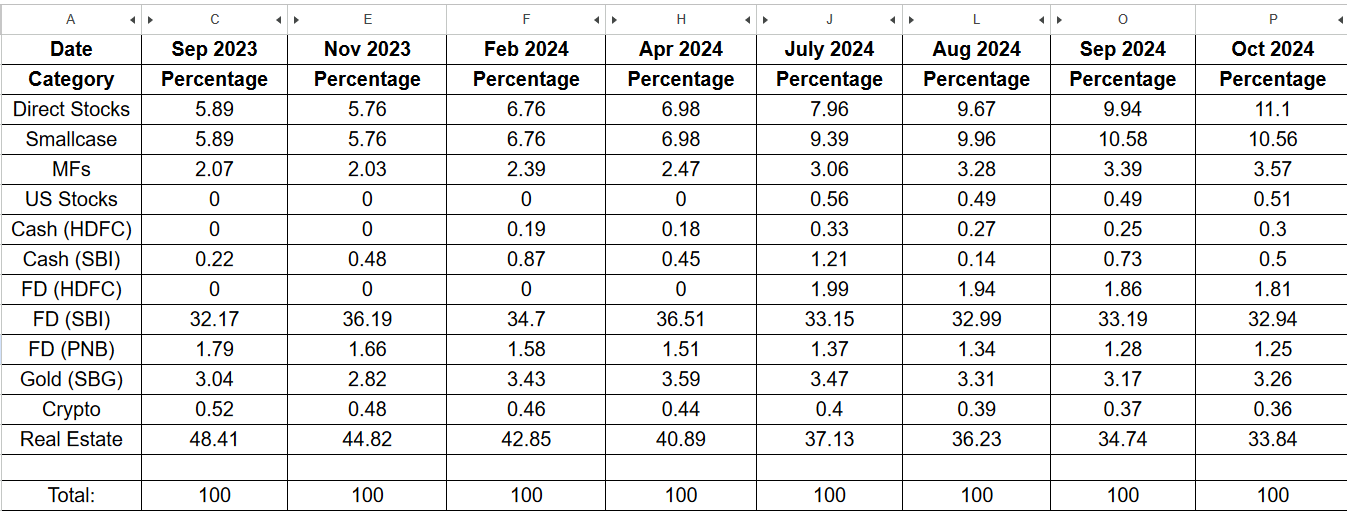

Yes, for most of us, the real estate takes up a huge chunk of our portfolio. I started tracking my investments in excel since Sep 2023. Here is how it has moved so far:

Just to clarify: In the introduction post I mentioned my Gold exposure to be 3.26%, which was not entirely correct, I missed to calculate the Gold-ETF.

The mentioned 3.26% is only the SGB part.

Total Gold exposure is 3.26% + 8.72% of 11.1% = 4.23%.

My aim is to make total Gold exposure to 8-10% of the entire portfolio.

As per your plan (regerring to your post above) , if you have a home by age 37 and loan free home by age 40, have a high growth plot of land in a good location and exposure to quality stocks & mutual funds…why do you need a 10% exposure to Gold?

You may need it till time you are exploring what kind of investor you are but once done, you may leave Gold to a maximum of say 1 year expenses in case of extreme exonomic turmoil in country and collapse of other financial channels (hope this never happens. Physical gold will only help then. Paper gold will have no value in such scenario and collapse.

Rest leave to females in family to enjoy as jewellery as per their liking and even some males like it. Enjoy the art for those who like it.

Btw above just personal thoughts and may change with time. Pls take your own decisions based on how your thinking evolves.

I might not be right but, just 2 cents if i were you, i would keep that much cash in hand in short term fd’s. (atleast 20%) since wedding is an expensive affair. So, your cash part is alright according to me.

The piece of land that you own is all upon you to access as to in how many years will it yeild a good return compared to any stock/mf investment you make.You might have bought it off dirt cheap and it would be great. Just take into consideration of your total capital gains tax that you might need to pay.

The crypto part, no comments,coz even i would have keep 0.2-1% of my wealth there…

Just on the stock/mf investments where i am more concerned for you.

If I were to invest into a nifty50 etf, why will i buy shares of the same holdings directly in my personal portfolio? both the places when i have the same bluechip stocks, dosen’t make sense… apart from keep let’s say 2-3.

Also, i cannot understand your equity investing thoughprocess. Since, i were to plan for a 30 year runway with enough cash, emergency fund & insurance. Good amount of mf investments, i would not invest majority of my wealth into companies with 50k+ cr in mcap…Since, the ability of compound/returns will be less than let’s say a midcap growing at 20-30%.

You might wana look here… And It would be better to cut down on irrelevant stocks unless you can track on all the investements you make. since, you might get busy with work and there personal commitments, will you be able to track all. (but then, here comes the comfort of having bluechip stocks, they are going nowhere )

I am a novice, don’t take anything as an investment advice. I am not SEBI registered.and i myself have made a lot of mistakes and might be wrong here as well.

Joy - At the age of 29 you are very clear about your goal & what you would like to achieve in your life. Having around 4 decades of experience, I would say it may be advantageous to you to restructure your portfolio to a great extent considering you are very young and you have atleast another 35 years of working life. I would suggest you to invest atleast 50% in equity, Real Estate may be 30%, Cash 10% and gold/silver may be 10%. Out of the 50% in equity, depending on the time available for you to handle direct equity investment, I would suggest 60% to be direct equity and 40% in mutual funds. Out of the equity investments, keep 60% in bluechip companies and balance 40% in mid cap companies. As regards mutual funds, keep 50% in mid cap funds and balance 50% in sectors like banking, consumer, defense etc. Hope this helps

I would ideally like to have more weightage in equity as you mentioned, where as my cash positions have more weight as of now. I am waiting to get good market opportunities to enter.