I hope my post didn’t turn out to be nasty, as the markets corrected a bit…but still, not enough correction IMO. Anyways, it all boils down to one’s risk profile when it comes to equity exposure.

1 Like

I am waiting for more correction to take entry! ![]()

![]()

2 Likes

Dear friend, I suggest that you go through the following article.Cheap markets should not be bought - Weekend Investing

1 Like

Hello,

In my opinion as a CFA aspirant, you have a rather high exposure to HDFC Bank.

It is not only about the individual holdings but I suggest you also look at the stock composition of your mutual funds. Since you have the Index Fund, it is highly likely that you also have HDFC Bank exposure through there.

I am not aware of the composition of your Parag Parikh Fund but if the fund is also holding HDFC Bank shares it further increases your exposure.

I strongly suggest you atleast cut down your direct stock exposure to HDFC Bank.

Also, 35% cash which you hold is also not a good indication since inflation will affect it. I suggest you look at Liquid Funds to temporarily keep the cash until you choose to spend/deploy it.

1 Like

Can you suggest some Liquid Funds?

I am waiting for a correction to deploy the capital.

Hey! Why did you say “just 2 cents if i were you”? ![]()

![]()

1 Like

best way to access a situation is to be in the other person’s shoes. and my words should not be “pathar ka lakhir”. just take the points that makes sense for you. hence.

like for others it can be a basket of stocks…

but for me when i am <25, i can have a very high risk taking appetite since my portfolio will be negligible(compared to the veterans here)… hence, i concentrate my portfolio with just 3-6 at the max(influenced by pabrai’s style of investing). with a couple of stocks to sprinkle money… hence, different risk appetite for different people.

More or less, they all are the same. They hold papers that mature in 91 days. So you can go with the bigger fund houses or the fund houses whose names you know or are comfortable with.

If you want to park your money in these funds, redeem them to buy stocks, in the time of a correction in the equity market, it is better to have some funds in liquid ETFs too, as you can sell the ETFs and use 80% of the proceeds instantly on the day of the fall. Just to make use of the fall which sometimes happens for a day or two, like when it happened in the last few days. And market can continue going up or consolidate for a month. With liquid funds, there could be instant redemption limit, and it could take a couple of days for the funds to get credited to bank account.

1 Like

Liquid funds are more or less the same.

A correction will happen or not is another question in itself.

What I personally did when I had a lumpsum a year back, I found a Mutual Fund I wanted to invest in but didnt want to risk all capital at the same valuation. So I put all the lumpsum money into the Liquid Fund of the same Fund House and Started an STP from the liquid fund into the Fund I wanted.

That helped me flatten out the short term buying prices a bit.

1 Like

IMO, if you are looking at long term investing (5 year plus horizon) temporary corrections should not really matter. So you should seriously consider deploying your cash as its giving you negative returns sitting in your bank account. You can reduce your risk (somewhat) by dividing your total cash into 12 equal installments and start investing thru monthly SIP in a basket of MFs with an allocation of 35% in Large & Mid cap, 25% in Mid / small cap, 20% in an index fund and 20% in a hybrid / multicap fund. This should fairly diversify your portfolio. If you are really confident with your stock picking abilities, you can forego the index funds and use that for direct investments. With this strategy, you will not miss out if the market rises and average out if the market corrects but you will atleast be in the market and make money going forward. You can even do the SIP bi-monthly or more as per your comfort to further fine tune the deployment.

Coming to your gold investments, I would suggest not to increase allocation or as others have suggested, wait till after your marriage to take a call on that. Gold as an asset class is traditionally a hedge rather than an investment and there are many other instruments offering a 10% return with capital protection. I notice you are also invested in SIlver. Whats your outlook with that investment?

On your direct equity investments, I will suggest to keep them at max 20% of your portfolio and take some calculated risk with those to generate a higher return as you are already taking professional help with your MF investments so there is no point taking on the same types of stocks in your direct portfolio as well.

Hope i have been able to help. I should congratulate you on starting your investment journey so early in life. Wish you all the best.

1 Like

Thanks a lot for explaining!

I am currently doing weekly SIP in a Large Cap, Flexi Cap and a Small Cap fund, I will try to increase the SIP amounts.

Gold I am currently investing some as Gold-ETF so that I can use them during marriage for making some jewellery. SGB I will hold them upto their maturity.

Silver I am investing to diversify among metals.

Thanks a lot for your help and your wishes! ![]()

As of 17th Oct 2024, I am clearly seeing a reverse Head and Shoulder pattern is getting formed. I am thinking that the markets may go down from here and maybe ~23K is a good support zone.

What do you guys feel?

1 Like

Update on the previous comment. As of 25th Oct 2024, the reverse Head and Shoulder pattern clearly played out. Still feel that ~23K is a good support zone.

1 Like

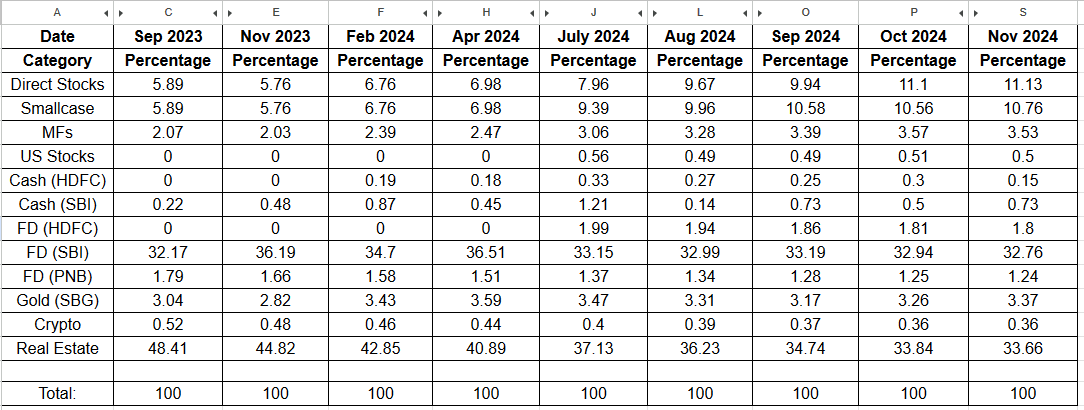

Its one month. Time to update my portfolio allocations.

The October 2024 was quite a volatile month, lost some of my profits, but at the same time without any panic invested more, could move some of my cash holdings to equity.

Equity exposure increased from 25.74% to 25.92% month-on-month and Cash holdings decreased from 36.8% to 36.68% month-on-month.

PS: I am not adding any price appreciation to my real estate, so the % allocation gets reduced month-on-month as other investments grow.

1 Like

Nifty50 is now below 200 dma and 10.71% down from its peak. Its a good time to use some of the cash positions. What do you guys think? : has it bottomed out or we have more to the show.

Let me know in comments/reply!

Stay strong! Enjoy investing! ![]()

1 Like

Only 40% stocks out of Nifty500 universe are trading above 200 DMA, which I believe is a good point (looking at historical data) to deploy cash. Rest market is supreme

2 Likes

Portfolio update Dec 2024.

November 2024 was quite a month. The stock market experienced volatility, but key indices like Nifty and Sensex saw recoveries. Mid-November saw notable rallies driven by strong buying across sectors such as IT, FMCG, and energy. Adani Group stocks and domestic institutional investor participation provided further support, despite foreign portfolio investor (FPI) outflows earlier in the month.

Despite short-term challenges, strong domestic economic fundamentals and growth in key sectors provided a positive outlook for the Indian stock market as it prepared for year-end trading.

Equity exposure increased from 25.92% to 28.94% month-on-month and Cash holdings decreased from 36.68% to 35.03% month-on-month.

Bulk invested in Nifty50 ETF around 23500 level and its already up by ~5%.

Bulk invested in HUL and Nestle (FMGC) both available at around ~18% discount from the top.

Let me know if you guys have any suggestions for me! Happy investing! ![]()

![]()

Nestle & HUL ?

May I ask the rationale behind apart from 18% discount??

1 Like

Sure. Among all the sectors FMGC is the most beaten down sector if we see the past 3 months data. Nestle and HUL are buy and forget type of stocks (defensive) for me since my horizon is 30+ years, so whenever I get to buy them at good valuations I accumulate them to generate the extra alpha.

P.S. Nestle India is trading at ~19% discount from the top.

@JoyD As I have mentioned earlier, we both are in almost the same age group. Considering this fact and your cash & real estate position in your portfolio, I do think that you’re being conservative with your positions in HUL & Nestle.

Not to mention about skyrocketing Food & Retail CPI, Slowing down GDP and Fall in Rupee.

HUL is at the same price as what it was during 2020 and Nestle is up 56% over 5 years which is 8% CAGR well below Nifty. Please revisit your risk to reward ratio considerations.

If you’re comfortable with minimum risk, totally fine, on the long run (in your case ~30 years) this will pay off

1 Like