GSK selling horlicks to fund novaritis deal. Is that a big deal?

I know this was big news a month back…considering slowing down malted drinks demand going forward, this might be a good move. But honestly, these brand sell off, mergers etc can be like a double edged sword. Some reports say, its right time to exit horlicks…approx $ 4 Bn cash gain.

Analyse delta corp for your Pf. On verge of multi year run given the land policy is abt to come.

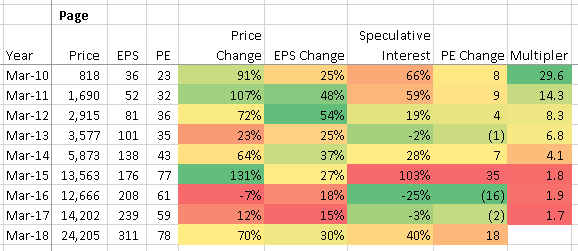

Very intersting concept Amit. However i feel that its a bit flawed. If you know a company is growth stock and it has a long run, the entry level did not matter (in hindsight). To check that I added another aspect to your data called Multplier i.e. how many times the stock price multipled since I bought it. Also I added PE change which shows the confidence of the market on the company´s future.

This what I find - As long as you are convinced the growth will continue at high rate, waiting for stock to cool off would reduce your returns - except in event of extreme PE change. If I had Rs10,000 to invest in this stock in Mar-12 I would make more money investing Mar-12 (83k) vs Mar-13 (68k).

There is a variance in the data that you and I have for stock price and EPS - if we both are using the same source, I am not sure where the gap is coming from. However over all dont find it big enough to change this observation.

Disclaimer: I do not recommend to buy at any price - I am believer in intrinsic value based investing. It can be noticed that in hindsight if you knew a company can growth for a very long period of time, maket will mis-price it almost every time This study has explained me why great investors always says that do not wait to time entry into a stock if you are convinced of it prospects - all thanks to your idea! ![]()

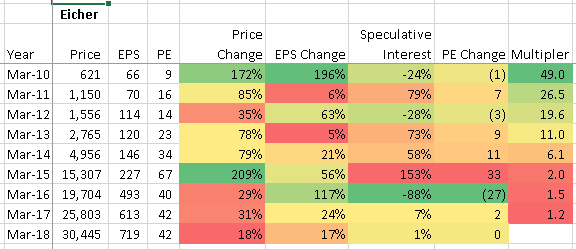

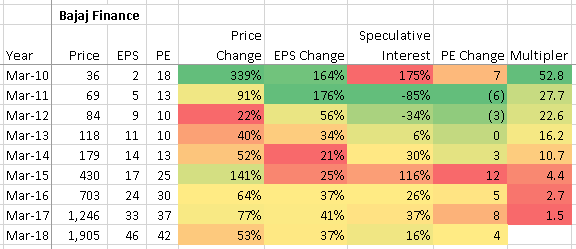

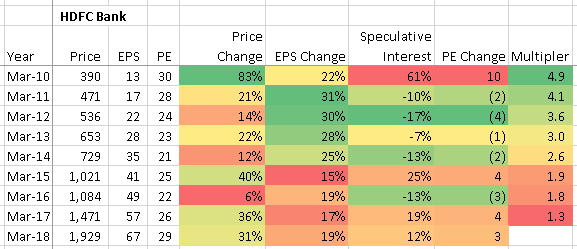

Some cross checking

HDFC is very unique!!

8 Likes

Please start your own portfolio thread and carry on the discussions there.

This post will be deleted in 24 hours

Hi. Yes Bank is not in a good state …I think you should wait till mgmt is confirmed on a new person. I think there will be volatility and skepticism until a good person holds the baton.

For Yes bank, management is a concern. However I think India Inc has plenty of world class CXOs to drive business in right direction. Its not a big challenge. However undisclosed NPA can play a bigger spoilsport in quarters to come.

1 Like

If ones assumption is that as long as EPS is growing share price will only go north.

That does not mean that there isn’t a downside. Time immemorial has proven that.

Most reports are marketing oriented going gung-ho on Horlicks brand, 4 bn USD valuation… Giants like Coca-Cola, Nestle planning to acquire and all that… Even i am looking to understand whether minority shareholder will have anything to gain or will bite the dust… Will share as soon I catch any good analysis. I will not self analyse, simply because M&A is not my cup of coffee.

1 Like

Very good portfolio…slightly focussed on banking/finance.

I guess already many people have expressed their concerns about Yes Bank which is valid.

Rest of the portfolio is really good.

Think adding Reliance, HDFC Bank, Asian Paints should be even good.

May be M&M in place of Maruti?? (Views invited)

1 Like

Would like to add that, large caps tend to give very little returns, or even negative, in the next five years, if they are bought expensive. This is a fact, not a subjective opinion.

Now the real question is, is your portfolio expensive? I’d say very expensive, but it’s anybody’s guess; only time will tell.

@jamit05

I suppose you mean PE contraction in next 5 years will limit stock price increase right!

I read sanjay bakshi article on quality. He gave example of bosch. Often you find quality Co stock at high price. You expect mean reversion. But quality with time becomes better and bigger and so thus the stock price… I am no sanjay bakshi, but don’t you think its equally risky to go for value picks as they can be value traps…

I still remember picking up unitech stock for Rs 5 yet making a good 30% loss… Long back though… Dont know present status…

1 Like

Yes absolutely, if bought expensive it can lead to very less returns. Hence timing is important.

I see few of the stocks you have timed really well like Maruti, HDFC. Others like Avanti, HDFC Life etc might show some more downside.

I remember Asian Paints trading in 1100s, HDFC Bank, Reliance very difficult to get it cheap.

Ah! Another stock Larsen, which was a bargain @ 1200 a month back could be a good buy

Asian paints was a bad miss. @hitesh2710 suggested also. Bounced from lows like a tennis ball…I think I should have a list of excellent quality stocks and a buy price alert. This will help me catch the bargains on time.

1 Like

In the current market there is no need to chase prices. Just keep patience and determine levels you are comfortable buying the companies you want to buy and keep placing orders in those ranges. On a really bad market day, sometimes these orders do get filled.

17 Likes

Since I don’t follow this stock price so it will be a audacity for me to comment on anything but being a quality investor I never looked for any valuation but yeah obviously a value bargain. I believe a quality stock like Asian Paints has a long way to go considering the mid range housing yet to get it’s momentum in India also the repairing market is yet a big market for them. So 15-20% up from a low is not a big deal in case their are no further downside. Since I personally believe that Crude Oil price will go up from here until the Aramco IPO gets launched since Saudi will definitely force OPEC to keep the price at high level to get a bigger subscription. So I guess the calculation needs to be done for how much the inventory and margin will be affected for this rise to Asian Paint.

1 Like

Oops. I conveyed wrong message. Meant try to invest in large caps at a reasonable price. If done at expensive levels it can result in flat/ less returns in the coming years.

But yeah, generically you are correct @dumboinvestor

Would it be then wise to do a SIP at some of the quality names like Asian Paints irrespective of price fluctuation, fellow members thoughts?

Agree and I clarfied the same in my disclaimer already. My point was about using “low Speculative interest” as an entry level.