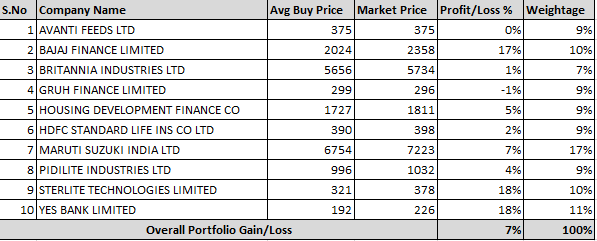

I come from non finance, non business and non tech back ground. I used screener for almost a year but never knew it comes from same family of ValuePickr. I am very new to investing in stocks and I find all financial formulas, ratios, graphs, macro-economic and political factors to be bit difficult. Having said that I have learnt few basic concepts of EPS growth, PE, PEG, ROE & CAGR from Investopedia( Its Like Wikipedia for finance). Few of my friends suggested Motilal WC study and after cursory reading I realized that above basic formulas are very important and basic. I have invested a small capital in 10 stocks in October 1st/2nd week and want to share my portfolio with you all for criticism and feedback. Thanks in advance !!!

Overall Rationale of investing

15% return on average. Approx doubling every 5 years.

Max loss absorbing ability (30%).

Limited no of stocks- max 10 as tracking, gaining knowledge is impossible for me

Select a common set of (known names, past winners, present bargains, good outlook, and good ratios). Ideally all together but should have most of them

Max 10 stock portfolio- any new addition will be after exiting one of them

Holding period- min 1 year or -20% whichever comes earlier. Max- as long as growing

Many Thanks for your inputs. Out of your suggestion, I am tracking Page, Nestle, Asian Paints. Also these are relatively easy to understand business. However, if at all I buy, I will add only after exiting equivalent nos of stocks in my portfolio. Else, will get confused with too many stocks. 1 from pharma & 1 from IT is also a good suggestion…any specific names…please do suggest. As far as financial stocks are concerned, Bajaj Fin is a past winner, HDFC is a reliable brand, HDFC standard life is possibly the best private insurer.

Yes bank & Avanti Feeds are kind of bargain buys- i think I bought them cheap

I would not like to allot 17% to a cyclical stock like Maruti. Good for bounce back trade but won’t allocate so high for the long term. I suggest you to look at asset management companies in place of insurance for the next few years. Insurance players are too expensive but ok for 10 yr holdings. Also some duplication like Gruh and HDFC - same line of biz and from the same group. Club these two into just one stock. I would suggest exchanging yes bank with IndusInd or AU Small bank unless you are playing a bounce back trade.

Imo, Maruti is steady and not cyclical. Budget, fuel efficient cars will have steady demand. Gruh & HDFC are duplication is a fair point. Although, I think they cater to different buyer segment …LIG/MIG & HIG respectively. Insurance , I am biased, because I see a huge trend in term insurance esp click2protect suite of HDFC life. As many as 4-5 friends have taken plans in last 1 year. Yes bank & Avanti are based on hope of recovery…low confidence. I plan to make a watchlist shortly. Either I will replace stocks or add new ones…Meanwhile lets see how it goes.

Hi - I’m in no way an expert but most of the companies that you’ve mentioned, albeit all high quality, are not available at a good price (forget about a very attractive one) and successful investing is as much about reasonable price as it is about quality.

And as for Yes Bank, yes it has had NPA undereporting issue in 2016 and 2017. But we should really ask ourselves, whether that is a reflection on the entire institution or the people running it currently? In my opinion, it is the latter. Look at the egs. of Axis Bank and ICICI Bank. They’re not bad institutions but, maybe driven by personal greed or overambition, the people at the top goofed up.

And as people at the top change, as is happening with all the 3 banks now, the institutions might outperform.

This is just my opinion & my views are biased for Yes Bank.

well, Maruti had a serious downturn during 2010-2014 and the current bull run for the last few years is partly due to easy financing, low commodity prices and Ola/Uber tailwind. Most of these are receding while competition is going to intensify going forward as both Hyundai and Tata going to attack small car segment. Let’s see … I might be wrong as well.

I don’t want to give any suggestion here. Just add my philosophy of investing.

High ROE , ROCE coupled with High Growth.

Low or nil debt coupled with Growth stability [i.e. operate in a industry which is having under penetrated large pie left or growing at a very high pace which to sustain atlest for 5-6 years]

Strong Business Moat [Monopoly or Duopoly,Low cost producer, Strong distribution network, simple lean easily replicable business model etc ]

Mainly non cyclical even if a cyclical one I will look to enter only at the bottom of the cycle.

these are the point I look for along with some discounted valuation to enter for having some bargain.

Given the above criteria I have only 3 company in my radar which I have invested in.

D-Mart, Bajaj Finance, SSWL …

Another company is in my purview but not invested in yet is Natco Pharma since I am not yet very confident about the pharma sector recovery . I might safely give it a pass for another quarter. But even under the downturn of this sector Natco has perform exceptionally well as a business but not as a stock though and thus gives a very good opportunity to enter at this level considering the sector revive in coming years.

Nice inputs !

However financing and commodity will affect overall auto sector. Competition is omni present. What is interesting is Ola/Uber led demand. Any idea what % of total sales was due to these cabs. e.g. out of 100 maruti cars, 25 were cabs kind of figure. This can help me estimate the impact. Having said that, renewal orders will also be there from ola/uber…cabs dont last long may be 3 years i suppose.

Natco is indeed interesting…PE 15 and PEG 0.3. Very attractive price. Also lots of Pros rating by screener. But understanding pharma business, needs bio chemistry degree

I don’t think so. Since we are not drug inventor but investor. With my limited knowledge what I understood about Pharma Business …

There are two types of company operate one which sales Branded Generic [where low cost operator moat works very well ] others are Contract Manufacturer [where bulk drug selling and stong B2B clientele is a good moat ]. Apart from that there are marketing company who along with a strong distribution network either have some backward integration of manufacturing facility or operate as asset light basis by outsourcing it to some contract manufacturing.

All these business have different moat where Natco falls in the 1st category where the moat it was having not only as a low cost generic producer but operate in a niche market like Oncology , Cardiac etc.

Risk in this segment is ANDA,UKMHR inspection of the facility apart from other geo political risk. To mitigate that natco has a strong record of these approval and regular training program conducted at it’s different facilities for it’s employee to adhere to all the norms.

For rest of the understanding VP has a separate links for each good Pharma company.

Some thoughts on Maruti (many borrowed from Rajeev Thakkar (PFFAS Director) talk here (Learning hack - watched at 1.25 playback speed)

Per 1000 population cars is still low in India compared to developed countries - given our state of public transport market potential remains high.

Agree that demand from ride hailing apps Uber / Ola isn’t sustainable but it also has created an aspirational class of people who now want to own car contributing to demand

Maruti has close to 50% share of PV and has maintained despite tough competition (next year Kia will also be vying for a share) over the years. I expect it to adapt, innovate to survive and thrive due to their ubiquitous network and their proven track record.

Another threat is Electric vehicles (a minister recently remarked that he wants to put fossil fuels out of business) Maruti is already working on this and when battery becomes a commodity, it can leverage its network and experience in design. In the medium run, CNG will play its role till EV picks steam.

-True Value centres usually lure with good exchange deals and hence higher prob of retaining customers. And pre-owned cars market is 1.2x of new cars. (This was hit due to GST and now recovering). Maruti biggest adv is their network, I reckon.

Also new emission norms force people to upgrade (already happening in Delhi)

Am also betting on their entry into LCV segment (Supercarry) to grwo / expand at a good pace.

I would avoid Yes bank because of the well documented reasons for its fall. I think in the short term Maruti is also going to suffer because there seems to be some headwinds in sales this festive season. They have pushed a lot of inventory to their dealers but thats not true reflection of their sales.

Sterlite Tech is having strong business momentum and could be interesting in view of the data boom happening. Avanti has reported poor set of numbers but part of it might be factored in at current price but if it goes down some more it could be interesting. In case of Avanti the management quality and market dominating position is a great asset to have but as demonstrated in the past too, one has to catch the cycle right to make money in Avanti.

Instead of these kind of names I would like to include Asian Paints and Bata on declines. As of now I feel the valuations dont offer too much comfort in terms of safety.

In the immediate near term I am not too sure about market direction so it might be prudent to buy in small lots it at all.

I must say great picks for long term…Britannia, pidilite, hdfc life are companies not to be sold for any targets…these companies can create world leaders in future!

Wonderful thought!. And conceptually I am with you. Lombard, Pru, HDFClife, some FMCG / Consumer plays (all quality names) should not have targets and should be part of long term portfolio by default. They are multi year compounders, and you don’t exit these stories unless the macro thesis related to these names change.

After having said this, now please pardon my dumb question - I am not able to wrap my head around this thought though.

Let’s take the example of HDFC life. If that scrip were to provide a 15% return (Why 15%? - Because Top league Mid Cap MFs have provided that kind of return over 5-7 years) over 20 years the stock price needs to return 16x, which at 80k CR Mcap is ~over 12,00,000 cr Mcap at the end of 20 years. - Which at current exchange rate is ~$180 Bn -~$200 Bn Mcap. This will mean that some of our quality bets need to transition into global TOP 10 leagues (Berkshire is $450 Bn in Mcap) - which is not impossible, but a tall order. Most of our scrips from the current level need to have over $50Bn $100Bn kind of Mcap.- Just my thoughts.

not sure about Lombard though in very long term…as general insurance I find a much riskier business and feel that years of accumulated profits can be lost in a single bad year if the underwriting was not proper.

We must remember that US is decades ahead of us, so the gap will remain but certainly reduce with time. Berkshire and other US giants will also grow in 20 years, so even a 200 billion $ mcap after 20 years may not feature in world top league

Which is all fine and I agree as well. My numbers are high level, has several assumptions and 20 years is too long time frame.

But we should be cognizant that today we have no more than 3 or 4 insurance companies in the world with over $100 Bn in Mcap (all mature markets and won’t outgrow). So invariably for some of our Indian bets to be double digit compounders they need to be global leaders.