I started direct equity investments recently from April 2020. I understand business related to software & healthcare those; hence my portfolio has heavy presences of it. As I lack stock market knowledge, try to stick to large cap mostly. Expecting 12-15% return??

I will highly appreciate any comment, assistance…. From you all.

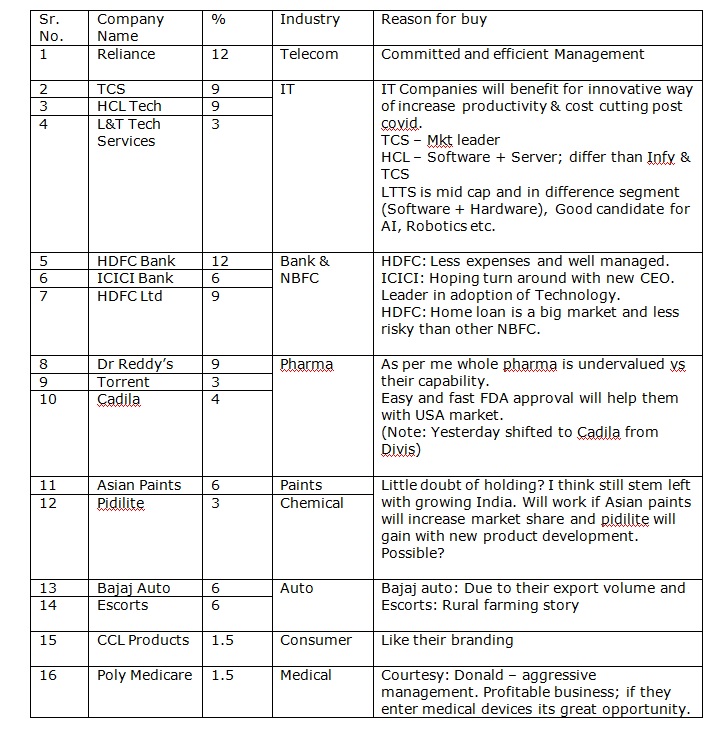

As suggested mentioned reason for buy. Concerning to sale I am hoping to continue with investments with periodical reviews hence not defining period etc.

Watch List:

17. PI Industry: Thinks costly as of now?

18. Maruti Suzuki – Doubt on PV segment?

19. Britannia or Nestle - High valuation but like to have one FMCG.

20. Ultratech – Cement is commodity but ultratech presence across India is attractive. Can have it for long term?

Rejected with pain:

21. HDFC AMC

22. ICICI Lombard

23. ICICI Prudential Life Insurance

High contender for disruption. Fintech start up will take market share from brick and mortal players eventually that’s what I think. Still have pain of letting them go. Open to change my mind as per your advice.

Ideally I like to hold 10-12 companies, which to leave is my dilemma?

Highly appreciate your feedback and assistance. Thanks in advance.

Any specific reason for selecting Britannia or Nestle or you just want a FMCG? if you are just looking for a FMCG, then look at Marico also… fair value, management is great, recently acquired Beardo, LIC also increased their stake in Marico.

look at their products/brands if you like or use them.

Disc:- I’m invested in Marico, I like and respect Harsh Mariwala, my view can be biased.

I liked your strategy especially your IT basket. Your overall thinking is in line with mine.

I have most of the stocks in my PF except Torrent, CCL and polymedicure. Could you please share your views as to why did you choose cadilla rather than Cipla or say Lupin.

Additionally, I own Insurance stocks which you rejected with pain…

In my view, insurance business is a long term growth story due to low penetration level and Covid19 would bring an awareness on life and health security. The customers would like to go for reputed entity like HDFC life or ICICI or say SBI life and these companies have very good distribution channels i.e all bank branches which will cater to the walk-in customers and also they have digital platform.

Discl: I own insurance stocks and my views may be biased.

Thanks @1957. My preference for pharma was DRL, Divis and Torrent; Cadila was 4th in list. Selected Divis due to pure API player different than DRL and Torrent. As indicated just shifted to Cadila from Divis recently. I want only 3 companies in my portfolio.

For Cadila

Management; Pankajbhai and his son. Am passing their HO daily so hard to resist.

Cadila Healthcare is also promoter of Zydus wellness.

Negative for cadila - has debt; don’t know it for cipla and lupin.

cipla and lupin; as per me they are also good companies. Like in IT we gets wide choice in pharma hence difficult to choose.

Its my POV, looking for comments from Seniors @hitesh2710@manish962 and others. Thanks.

Regarding insurance; Yes agree with you that penetration will increase and covid will make it fast than anticipated. However we need to think;

Will this be with our businesses?

Even yes, will it be profitable?

India’s innovation in fintech is amazing. As example UPI, other developed nation is also looking toward India for it (G pay is first implemented in India). In finance field we have Zerodha who is No. 1 ahead than HDFC and ICICI frenchises.

Its not about companies; As per me Tech will revolutionized brokering and insurances businesses. Like; USA is paying less than we did for stock brokering and MF.

Insurance and Brokerage is easy to transform as its negative cash business. Easy for start up to enter in this field. If you have noted, we easily trust VC funded start up like paytm, phone pe etc even for critical job like money transfer.

Some business like HCF, which needed upfront cash, can’t be transformed easily.

Said so United health Ins is USA’s top 10-20 company in mkt cap (need to check exact position). They are in to health insurance. So not sure and don’t want to conclude. You may be right…

Just my pov.

Disc: Not invested hence my view is biased. May change my view in future.

@Deven good to see another fellow Ahmedabadi passing through same route as mine I would like to know if you have considered Eris Life sciences? It is also a well managed company from Ahmedabad which is totally domestic facing. So, one doesn’t have to worry much about USFDA regulations for growth.

@1957 what do you think about LIC being dominant force in Life Insurance segment? From what I have gathered, Life insurance market is not as under penetrated as general insurance or Asset management market. LIC have more AUM than whole Mutual funds sector combined. So, room for growth is rather low in Life Insurance sector. You can see ICICI Prudential’s last decade results to see how companies in life insurance sector can lag if they focus too much on ULIPs. Here is an informative episode of Capitalmind podcast that throws light on how life insurance sector is quite mature compared to other financial services in India

Thanks @Chaitanya_Tanti

Not only FDA Eris even saves on R&D.

Have you studied that AR? How you said well managed? …

Yes I briefly studied their AR and immediately rejected it for investment. I have very bearish views. As I immediately rejected co, I find no need to study it more. So my opinion is from limited study.

Who in AR give graphics of their share holding indicating investment by FII and DII. Ok Ignore it - not a big issue…But

Total Employee: 3399

2000 MR, 880 Field Managers, 223 manufacturing .

Even if nos are correct it basically says its trading company with fancy name as life sciences. Its sin to compare it with Cadila.

Nothing wrong to have trading company. its profitable business but should not give wrong impression by fancy name.

If you are invested; than red flag - promoter is reducing stake. (May they have good reason - I don’t know).

In general am not so much loud in my opinion but in this case I remembered to have awkward sense while studying AR.

Note: As indicated my view is from limited study. Glad to be proved wrong. Not invested and no plan in near future. May change my opinion in future.

Very nice portfolio indeed and I like the high allocation to RIL.

Can you please let me know why large wtage in companies TCS and HCL Tech. I feel over the years, their margins have been under pressure only and without the rupee devaluation Indian IT sector cannot generate good profits. I say so because I myself work in the IT services industry and see less growth in it. Also if from tech - I would have preferred to invest in new internet based companies like Infoedge, Indiamart and Affle which are growing in faster rate. Infact I am invested in a couple of these.

Also after the recent crash, dont you feel bajaj finance can be more attractive than HDFC.

But overal I like ur PF and I am invested in 7 of the companies which you have.

@Deven

(1) With regards to Tech disruption on Brokerage Services, I tend to agree with you…as Zerodha like start-ups can emerge disrupting the business of ICICI securities / ICICI direct and HDFC securities who have trading platforms with a charge. So , I may not buy the stock “ICICI Securities” though it is available at attractive valuation and though it is reputed brokerage company ( please recall the recent Karvy episode) , However, I may tend to invest in ICICI AMC if it gets listed…I have invested in HDFC AMC.

Because in my view AMC business as a whole is a different ball game. These fund houses have their own well experienced Fund managers who manage the mutual funds and there is a trust factor on reputed AMC’s . Currently HDFC AMC manages AUM of Rs 3.79 Lakh Crore and SBI AMC 3.82 Lakh crore. Mutual funds SIP are very popular among investors in general who don’t venture in to direct equity like you and me…neither they have the knowledge, skill and time to invest in direct equity…AMC charge every year some % of AUM as fees on MF investors- whatever platform they use whether Zerodha or ICICI direct…Further Each AMC has their own direct MF schemes where investors can directly invest. Corporates, SME’s also invest their surplus money in mutual funds…still Equity MF penetration in India is as low as 10% as against 90% in developed countries.

(2) Coming to insurance business, India insurance penetration level is low at 3.49% FY 2017 as against Global Average of 6%. Some advanced countries have insurance penetration level of 8-20%.

The average age of an indian in 2020 is just 29 years…

Coming to Life insurance LIC had 100% market share say 10 years back… But once the Pvt players have entered the market, LIC now holds only 75% market share … Still when it comes to Life insurance term plan, trust element comes in to play and an indian would prefer LIC…But things are changing, HDFC life , SBI life are gradually becoming popular with a customised product…Another Growth area is non life insurancr product such as Health insurance plans, General insurance/Marine insurance etc. where the Pvt insurers have a strong hold.

In spite of withdrawal of tax concessions, there are a section of people would prefer to buy an ULIP from ICICI pru or HDFCLife which ensures both investment in stock market and life insurance…

Attaching few links for your Study:

Discl: Invested in AMC and insurance stocks… I may be biased

I have done some basic research on Eris and from that I found that company has low debt levels as well as domestic portfolio. I am aware of the fact that it doesn’t have R&D expenses and it buys brands from other companies. I always thought of it as domestic pharma company which has tax break on its manufacturing plant.(Guwahati) But regarding AR, I haven’t gone through them. Also, I didn’t realise it was trading company because I haven’t gone through employee numbers.

That can’t be right. Because as far as I remember, by 2010 there were many life insurance companies in India. Even historic report I found for 2010-11 shows share of private insurers to be at 30% in 2011. I get the general sentiment of your argument that private companies are growing and under penetration of life insurance but I don’t think Private companies are snatching market share of LIC like private companies did with PSU banks.life-insurance-industry-in-india–an-overview.pdf (1.0 MB)

Thanks for comment. Rupee devaluation will continue.

Info Edge +, are not my cup of tea. Never bothered to check it before; just checking…PE 165?

Are you guys invested?! Naukri.com is there since I started my carrier; 1997. Sanjeev Bikchandani was famous speaker that time… Why Mr. Market giving 165 PE now? There is no change in business model revenue, profit.? Any experience person please comment, its beyond my understanding… It is due to zomato investment?! Please note to find 1 zomato you need to lose investment in 10 start ups. Costly affair.

Jaisish, brother check ROCE, ROE, Sales growth on screener, why you should give that high PE?! This is insane.

HDFC is housing finance, default rate is low. BF is also good but i prefer HDFC over it.

What I said is :

(1) when it comes to Life insurance products such as term insurance, LIC still enjoys the trust of people. But the insurance sector as a whole in India is grossly under-penetrated… You may please refer the statistics from the attached link when compared with global peers. People open accounts in banks and now banks are agressively cross selling the insurance products customised especially in the form of ULIP and other insurance plans…and overall gradually the Life insurance market would expand…

(2) Apart from ULIP and other term insurance plan , wanted to add that the PVt insurers are very strong in Health insurance plans, General insurance/ marine insurance which is also grossly under-penetrated in India.

I think infoedge has invested in multiple tech start ups like naukri, 99 acres, jeevansaathi, policy bazaar, zomato, etc…and the high valuations is due to internet based companies have high valuations even in Nasdaq…so with the growth of base their revenue and hence profit growth can increase…see amazon for example which has grown 30 times in last 10 years…