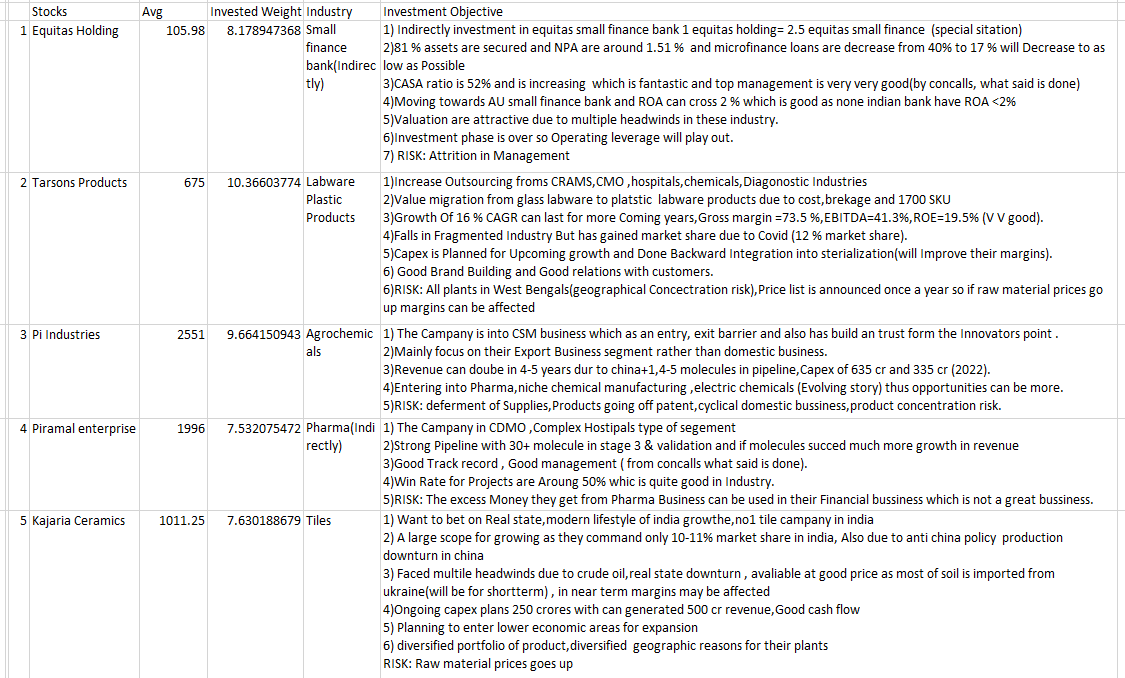

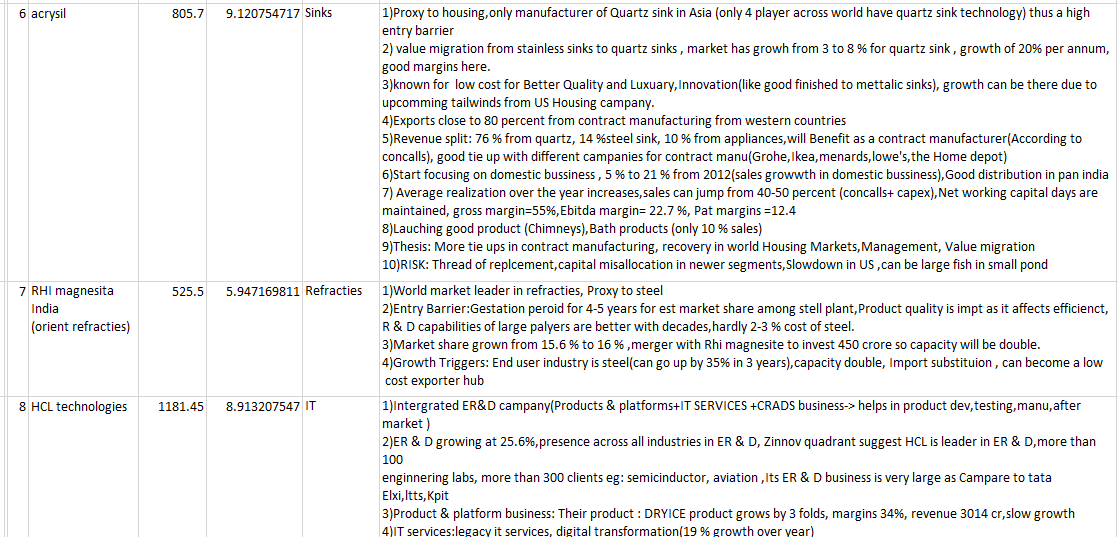

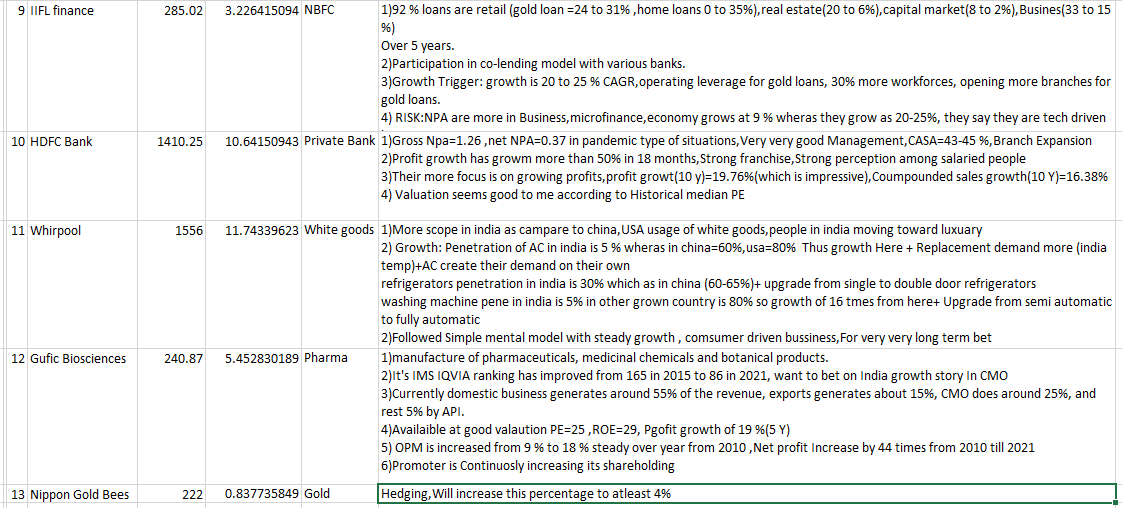

I am new to Investing world .Here is my Portfolio that I have created After many Studies, research and Brainstorming.

Dear members Plz go through it and suggest any changes.

I have not invested in any Chemical companies as I find none of good companies at good valuation

Disclaimer: please do not think of any of this as investment advice. All of these are my personal opinions and I could very well be wrong about any of them. Please consult your financial advisors before investing in anything.

Seems like a diversified and sound portfolio. Although most of them seems to be new entries, based on avg. price, if you can hold on for long term can create good wealth for you. Don’t worry too much about missing out on any specific sector if you are not comfortable with their valuations. Good luck.

your portfolio is well diversified, however the weightage allocated more towards finance, reality theme, which in turn has a relation and correlated to each other. from the legacy data point we could see a positive, negative correlation between these, and what if we see a headwinds in near future and it is higher chance that you end up in consolidation phase. In the current time, we see a tailwind under music, ev, specialty chemical, technology themes, and many of industry experts has a high conviction in these trends, adding a weightage about 10-20% to above will further strengthen your portfolio.

Thanks @BejgamNishanth for your point on financial sector it may be possible

I am studying saragama, Some chemical stocks (privi, neogen, clean science)

Will surely add saragama but valuations seems to be expensive and same for the chemical space .

For EV I can bet on tata elxsi(again valuation), Tata motors(but debt is more),Sona comstart All are fantastic companies.

Surely add some stocks from the theme as valuation seem to be comfortable for me or I am sure that the growth will last for next 4-5 years(if i buyed a stock at high PE).

THANK YOU AGAIN

Nippon India ETF GOLDBEES can be replaced by maybe let’s say 2% of the 4% you tend to hedge… into SOVEREIGN GOLD BONDS.

these are tax free bonds, which are issue by rbi for a max of 7yrs. which give regular interest on the value of gold. can be sold after 5 yrs to be tax free. these are issued at a discount of rs. 51 per gram. can be a good discount for higher allocation.

or if 7yrs end, you can re invest the entire amt again into a new sgb issue.

you can also have some % of your portfolio in cash. or can also invest into index as well if you don’t look into your portfolio let say after 3-4 yrs later. index funds can help.

Thank @Investing_Diaries for your point of Gold Bond I will surely do that

The main reason for buying GoldBees is at difficult times this is the easiest source of money I can get Or if suppose I find good opportunities in market at right time(March-June 2020) I can used this amount .

but instead of having invested into goldbees (currently overvalued as i feel)

dis: sold a significant amt of goldbees today.

instead of investing into goldbees and then liquidating, better keep it as cash investments.

this is becuase you have 2 demerger plays(PEL & Equitas) which is ~14%. If this doesn’t cross 1Lakh of your capital gain in 1 Financial Year after the goldbees transaction then it’s ok. else you might end up going for some tax.

And if you decide to sell some positions for profit booking. then it’s again a thing you need to calculate.

Though its a great list, I would like to add my two cents:

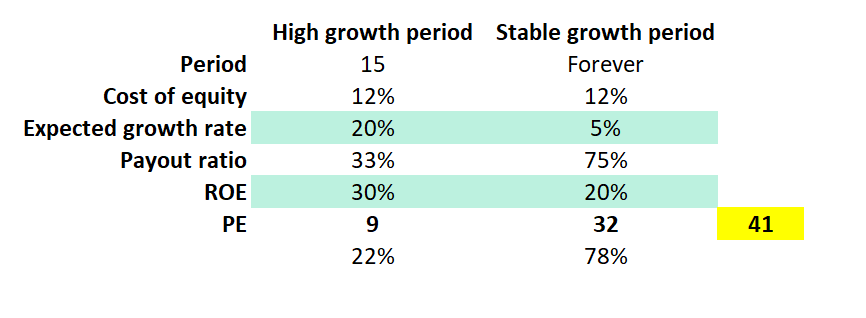

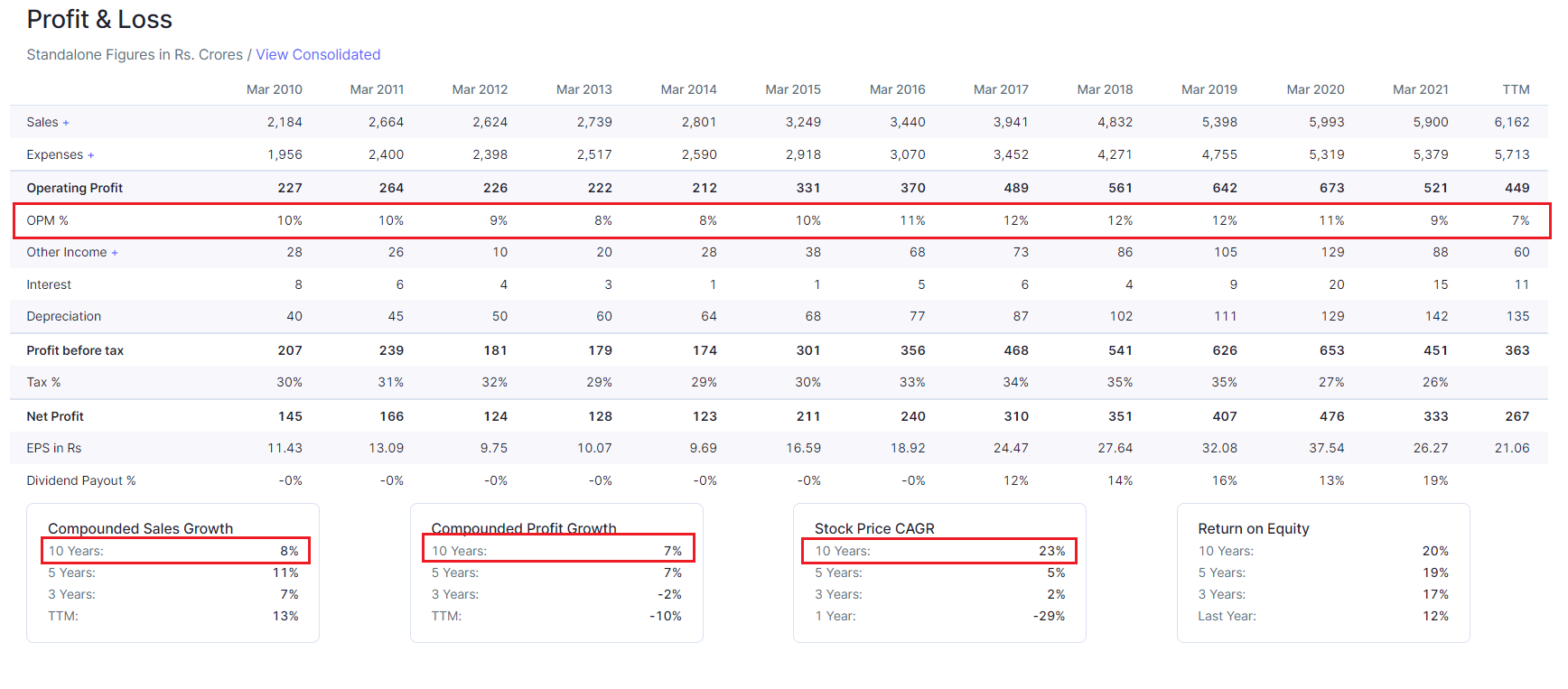

Whirlpool has highest weightage in your portfolio and I assume that has been recently added. What’s your rationale behind that? I agree AC penetration in India is very low but this could have been played with a cheap OEM/ODM proxy as well. Whirlpool is trading at 75x earnings at the moment. Just for context, if we’re confident of its future growth, lets do a quick exercise:

Lets say Whirlpool keeps growing at 20% growth rate for next 15 years and then transitions to a stable growth rate of 5%. Assuming 12% cost of equity, 30% ROE (being very generous), warranted PE multiple would be 41x.

If it grows by 27% for next 15 years then it might justify given valuation, provided other parameters I have assumed hold true. last 10 year compounded sales growth is 8%, profit growth 7%.

I do not intend to suggest you to do DCF every time you value a company. This is just an exercise to make sense of what kind of valuation looks reasonable at given growth prospects. Further, historical growth has not been great while stock price has compounded quite well. In long term, stock returns should reflect business returns.

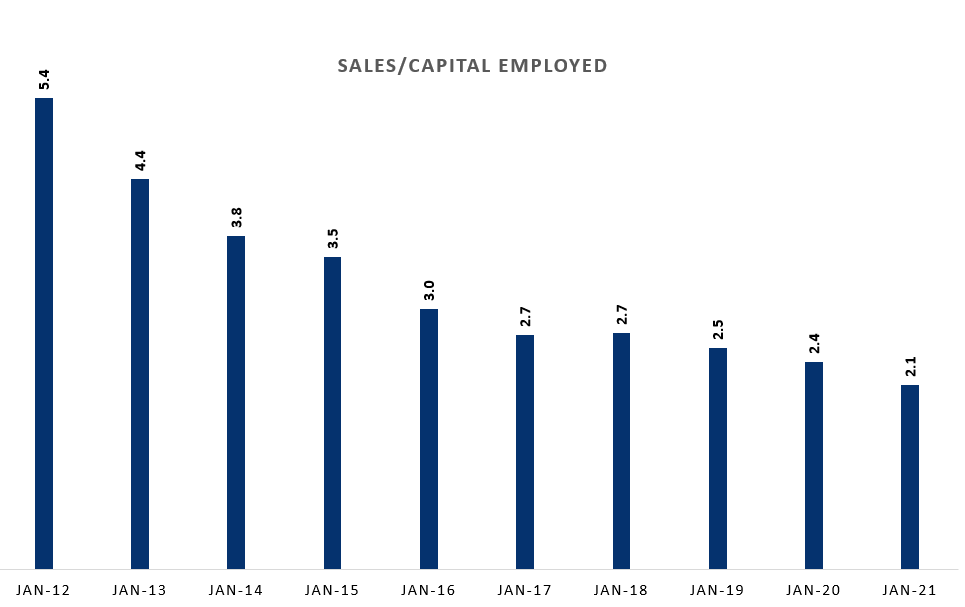

In the image above, you’d notice that operating margins are thin which suggests Whirlpool does not have a demand side advantage. Although ROI is quite decent i.e. they do have some supply side advantage. However, Sales/Capital employed and total asset turnover are on a decline over the last decade.

Some of these high PE stocks in your portfolio are quality stocks that may do very well but since you have recently added these, my advice to you for future is, no matter how good a business is, try to pay as little as you can for growth because growth is only speculation until it actually happens. Hope you find it useful. All the very best!

Your Point is quite good . I will definitely look towards it

What i through is Investing in some debt(might be liquid funds) instruments rather than increasing my weightage towards Nippon Gold Bees

First of all Thank you @KP2018

I find your article very useful

My Intension to Invest in whirpool was to just bet on upcoming India growth in comparison to other countries But your Reverse DCF approch is quite fantastic and make sense

NOTED: would be Reducing Stake in whirpool

THANK YOU AGAIN FOR YOUR EFFORTS

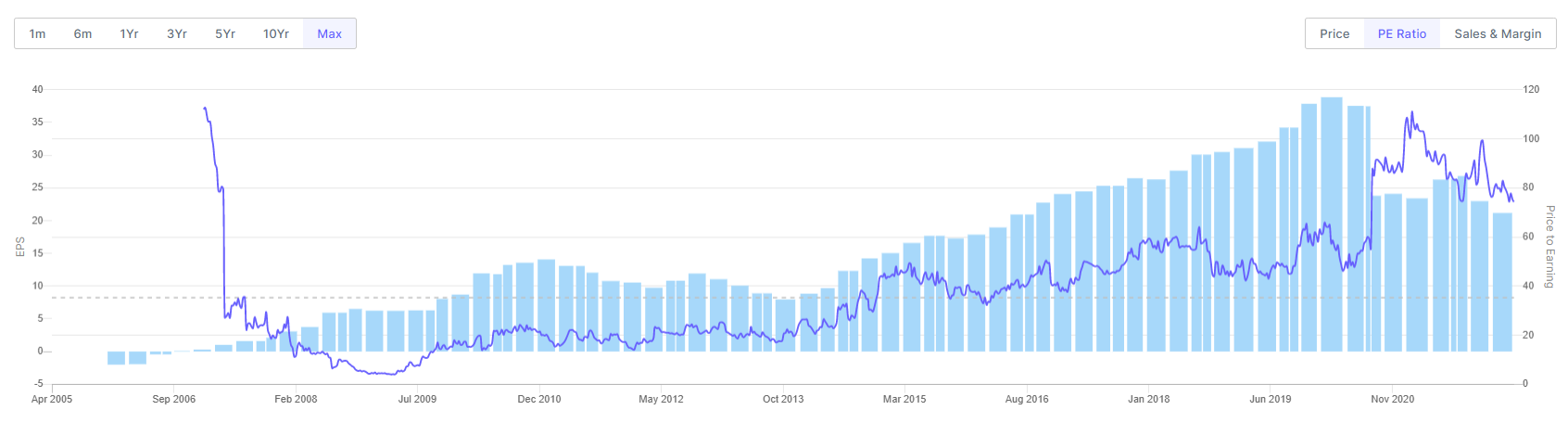

This company has maintained decent RoCEs for over a decade, and has had an abysmal FY21 and FY22 on margins. It doesn’t need to grow at 20% for 15 years, it needs to regain the margin profile of 10-12% seen for an entire decade, and in my opinion, an investment thesis has to be built around the probabilities of this happening.

If they grow at 10% over the next two years and achieve 8% PAT margins, that’s an FY24E PE of 34.17, which is below the median multiple that Whirlpool has traded at in the last 7 years:

I don’t see why a company like this isn’t a contrarian play, with a thesis of mean reversion. There can be arguments around the future of the consumer durables sector and the valuations it can command, but surely forecasts of growth and margins should be grounded in what the company is doing, not a DCF on a low base…

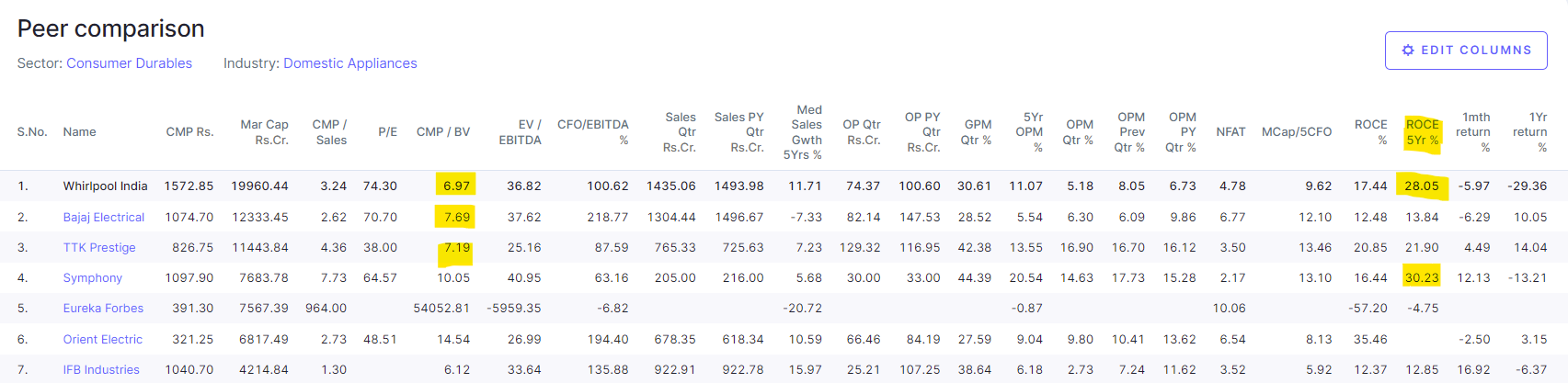

No investments in Whirlpool, just wanted to point out a rebuttal to the earlier post as you’d decided to trim holdings. PE can’t be the only measure of when something is expensive, and it’s worth having more data points.

I liked your analysis of future PEs and discounting to check , what valuation justifies it. Can you please do similar analysis for Nestle, Asian Paints and HUL?

i m worried for the same reason. Many people cite the example of Nifty 50 debacle of US in 1960-70…where such high quality stocks at high PE performed poorly for long period of time…but at the start of decade they were touted as best stocks with coffee-can quality…Will that happen with our blue chip stocks?

I clarified in my post that I am not recommending DCF to value Whirlpool at all. I simply wanted to highlight the kind of growth expectation one should have with such high multiples. Besides, it has nothing to do with whirlpool’s low base as it’s a mathematical expression that simply explains fair value PE multiple based to expected growth rates. I second that 10-15 year growth forecasts do not make sense but one needs to be cognizant of the kind of derating high PE stocks will face if the growth forecast does not come true.

Coming to Whirlpool’s ROCE over a decade, I’ll reiterate, operating margins are thin, but it had supply side advantage which seems declining over the decade. Here are Sales over capital employed numbers over a decade declining possibly due to intense competition-

Talking of 10% growth/8% PAT margins, seems reasonable. However consumer durable raw material prices have been very volatile and 7% OPM on TTM basis reflects that. Price to Book? Other than financials, I am not sure why do we need to compare P/B. Accounting differences make it hard to compare different companies. Also, consumer durables have intangible assets in big/small brands which book value does not account for.

My post was essentially not against Whirlpool as an investment but an attempt to emphasize on growth expectations for every high PE stock Aditya has recently entered.

The argument I was making earlier was that PE isn’t a reliable metric of being expensive when margins have contracted, assuming the contraction is transitory and not structural. So if Whirlpool’s margins have fallen to 4-5%, PE will automatically look higher.

So I turned to two valuation metrics that don’t depend on EBITDA margins, price/sales and price/book, to see if they further provide confirmation that Whirlpool is expensive. I highlighted how those ratios actually are in the realm of reasonable.

Thanks for sharing, this is a useful data point, and perhaps offers an argument that Whirlpool shouldn’t be valued as high as historic averages due to the declining relative metrics

Thanks @Chins for these reason That’s why I have said that i am not completely getting out of whirpool . I have also some thesis behind it for years if it happens then it will be good

Guys I have 1 Question

After studying music label saregama i am really impressed by the growth coming in it

and same applies to neogen, navin flourine, clean science , tata elxsi

Should I buy them at this valuation or should wait(can miss the bus )

Suggestions @BejgamNishanth@Investing_Diaries@KP2018@navvod@Mudit.Kushalvardhan@Chins and any person from this amazing committee who can help