Sorry Guys for being inactive in forum, was having health issues . Fine Now

In this span of time i have Change my strategy and moved to cos which are growing at a fast phase, Have tailwinds.Thus have removed cos (Kajaria, Whirpool).

Although I was in a favors of keeping whirpool for a quite long time but as early investor I thought I can take some risk.

I have also created a family portfolio for my parent where i have moved cos(Piramal enterprise, PI industries, HCL, Tata Motors, HDFC bank, RHI magnesita) and added some more Bluechips cos(Divis, Baja finance,) which would be safer for my parents+ Some high risk cos like(Saregama, HCG, NH, KEI, Syngene,)+ Some good midcaps (clean science, Navin flourine, Varun beverages, Radico Khaitan, APL apollo).

My new portfolio is completely based on Variant perception mental model(High focus on tailwinds, growth)

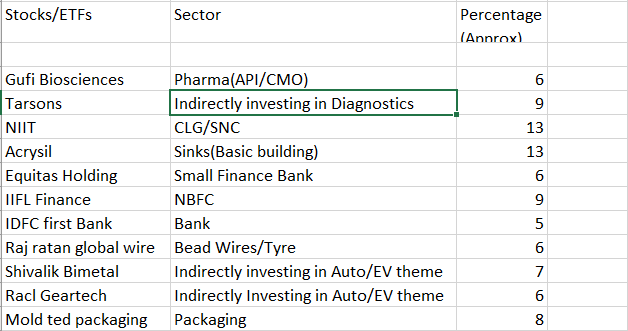

Added some cos and thesis behind them

Moldtek Packaging:

1)Mold-Tek is an B2B Rigid plastic packaging industry Founded in 1985 by Mr J Lakshmana Ra(MD)o and Mr A Subrahmanyan(Deputy MD) and is the Leader In rigid Plastic Packaging.

What Campany Does?

Campany Manufacture Plastic related Items using In mold labelling Technology (IML)(sales:60%) for paints(Asian paints, Berger Paints,Kansai Nerolac, Apollo paints), oil & lubricant(5-7% growth)(sales:24%)(Customer: Castrol,Gulf,Bharat Petro,Reliance,HP,Indian Oil, Exon Mobil),Fmcg (ice cream box,Pumps like sanitiser , inhaler,shampoo Bottle)(sales: 18%)(Customer:ITC,P&G,Cadbury,Himalaya,Haldirams,Britannia,Amul,HUL,Nestle,Dabur,Parle)

IML Technology gives long Branding Life and Mold-tek is the Pioneer in it with 60% market share

10 Manufacturing faciltity with 41400 Tpa capacity

Moats: All mould, Robots used in labelling are produced in House

2) Strength: Extensive experience in plastic packaging, strong customer base with 100 Repaet Order, Innovation and in house development(Adoption of IML tech and Investing in R&D),Fully Backward integrated (use of robots Reduces their cost a Lot),Campany can pass prices Hikes

3)Future plans:Adding high value added products through both product & geographical expansion, entering new segment called injection blow Molding(IBM)(fast growing ,Precision,market Potential:5000 cr year, expected to reach 7-10 % , High margin business) Cater to pharma ,FMCG,cosmetics sector , opportunity size in IML is huge as Paints indutry has no tcompletely shift to IML,

Capex: raises 103.6 cr for expansion of capacity,Expanded Capacity In kanpur, Doubling its capacity in Mysore and Vizag,Opening New Facilities In Sultanpur

4) Key Risk:Sales 35% from asian paints(Not a Big Risk), Raw material price fluctuation(campany can pass on price hikes),dependence on End sector, Competition From Deep Polymer, Cello Wim plast, Time Technoplast,End user Industry Dependence, High Working capital Loans(Paise late aata hai )

5)Finacial :Cagr sales(5 year) : 22%, profit Growth Cagr(5 year):19 %,OPM=20%,ROCE=23.9%,ROE=22.2%,Debt to equity: 0.4,Reserves:Consistent increase in reserve

Size Of Opportunity:Growth In Long Term as more and more cos moved to IML,IBM(2-3 years)

Shivalik Bimetal:

1)Business of joining materials through different methods such as diffusion bonding, cladding, electron beam welding, solder re-flow and resistance welding. They can manufacture multi-gauge and multi-material strips. They primarily manufacture Shunts and Bimetals since 1985.

2) Bimetals: applications of Bimetals in electrical equipments like Circuit Breakers, Overload Relays, Energy Regulators, Light Flashers, Automatic Fuses, Pressure Gauges, Electric Iron, Coffee makers, Washing Machine, Baking Oven, Refrigerator, Water Heater, Fluorescent Light Starters and many similar areas. In Automotive, it’s used in Exhaust manifold Controls, Turn Indicator, Oil Pressure Gauges, Circuit Breakers, Oil Cooling Regulator.

3)Shunts: These are also Bimetal Strips only. It acts as a Resistor and made from two or more alloys consist of different Temperature Coefficient of Resistance (TCF).The demand of High precision Shunt is higher and growing rapidly. This is a key and basic passive component in Electric Vehicles, Electronics of an automobile, Robotics, Internet of Moving Things, Augmented Reality and vertical Farming. There are wide variety of resistors and many suppliers for it. But the specific shunts Shivalik manufactures are mainly used in battery Management Systems (BMS), Intelligent battery Sensors (IBS) and Energy meters. All three are high growth areas.

4)specific kinds of shunts they make (among many other varieties), there are only few major suppliers as its a niche product where they developed expertise over many years of in-house efforts in product development.

5) Have pricing power as shunts are required in Less Quantity , Critical Application Product in BMS,operating in market niche with specialized expertise

6) metals such as nickel and copper forming around 50% of overall cost, operating margin remains susceptible to volatility in commodity prices,90% market share in domestic shut industry

7) Growth trigger: India EV Market to grow at 37% CAGR between 2018-23, Semiconductor shortage, Can increase their export to us a lot,Putting hand in defense sector, good demand of products

RISK:- technological advancements or obsolescence or fall in price of product etc due to high competition

8) Customers: VISHAY dale electronics, export to usa, mexico

Key points from vauepickr: —>shunt resistors we were the first company to enter into shunt resistors. Gear and mechanical approval for vendors take at least 18 – 24 months while electronic approval takes 3 – 4 years.

—>Hall effect sensor are used for high current measurement vs shunk for low current , shunt measure accurate as campared to HE sensors.

Valuation: Entered in Okish valuation

RACL Geartech:

1)Company manufactures high-precision products (various types of transmission gears and shafts) for the premium segment and has reputed global majors such as BMW, Kubota, Piaggio, Yamaha, KTM, BRP Rotax etc. as its key customers.

2)Good growth in export sales

The export sales of the company are continuously increasing and have increased from 59 Cr in FY16 to 142 Cr in FY20 and it formed around 70% of total sales during FY20.

3)Revenue Breakup FY20 :Motorbike & Scooters – 47%,Tractors & Agriculture Equipment – 16%, 3 Wheeler – 14%, Recreational Vehicles (ATV & RTV) – 16%

4) capex: 50 cr

—>have Pricing power in export , in domestic we may suffer in pricing

—> In china regulation issue have let to shutdown although china has better tech than us

—>Value will come down for gears in EV but quality is many folds higher

—>For many of our customers, we are the sole suppliers for many of their products throughout their plant locations.

—>We keep on adding new customers every year

—>Domestic sales haven’t grown for us. Reason for it? The main reason is that we were late into Hero’s and Bajaj’s of the world and these companies have their family member’s company supplying to them.

---->Competition: Hitech Gears, Bharat Gears – majorly mass market players. Hitech gears is getting into new products. Hero Motors is our competitor.

---->Management quality sounds very well

----->RACL Geartech- A Microcap Gem – Phoenix Capital

Growth Triggers:Have to achieve sales growth of 500 cr till FY2025 management is confident about it,Keeps on adding new client every year, they cater to luxuary brand , Export can increase .

Risk:Slowdown in economy,Debt is higher than reserves

disc: Taking position might be good for next 5 years

Valuation : Found to be in range of cheap–> okish

NIIT:

1)a) Corporate learning group(CLG)/Management traning and services(MTS) Like learning technolgy, strategy sourcing, content &

curriculum. Used ony (79 % ROCE),CLG business is a Win win Business, North America, Europe, Asia, and Oceania.

b)Skills& career group(SNC) ,These include Technology, Banking & Finance, Digital Marketing, Data Sciences & Analytics, Professional Life Skills, Business Process Excellence, and Multi-sectoral Vocational Skills. The Company provides these programs in India & China

2)Only Profitable edtech campany,Past history of Niit ws bad but they sold all their bad business, From FY 2023 You will see Roce=80%,Cash Generating Business(Turnaround) situation ,Concall Tell a lot ,Growing =25-30% , EBITDA margin=15-20%

3) Size of opportunity : less than 250 out of 1000 fortune campany outsource their tarining Therfore large Opportunity

4) Supply side Dominant player in world & largest palyer, customer grows from 39 to 58, Free cash Flow business

5)Demerger can happen Soon

RISK: Competiton from its peer like Aptech, Online learning Platform (udacity, coursera,udemy)

My some cos have a high percentage but would try to reduce it to around 8-10%.

Studying some more cos in Bearing sector, Affordable Housing Sector

Remaining percentage I have invested in US cos (Apple, microsoft, Nvidia, Tesla, Google, Amaon, S&P 500 ETF, Salesforces, Coinbase) Apple being highest in percentage (45% Approx) Which Brings my cash down to almost 0.

All types of suggestion regarding my Family Portfolio, My portfolio, US portfolio is highly appreciated.

Thanks in Advance and sorry for any mistakes in the Post

in the question. much love.

in the question. much love.