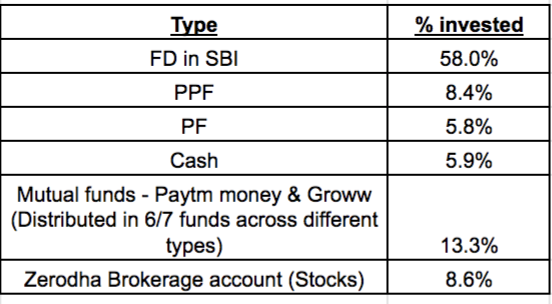

I am able to save ~2% of my total portfolio value every month from my salary. Don’t have any property or car. Have sufficient health insurance for me & my wife. No children. Parents are not financially dependent on me.

I used to keep all my money in FDs till February/March this year post which I have started investing in MFs & stocks. Current Mutual funds portfolio is down 5% and stocks are down ~20%

I plan to work for another 25 years & want to make money for all the usual goals - house, car, children, retirement etc.

You should buy a home for yourself if not owning one, which should be your first goal. Keeping money in FD and not owning home is bad idea. Don’t get too much enthusiastic for indian stock market at this stage.

Since you already hold mutual fund investments, the number of stocks that you own ideally may come down to 14-15 in which you have high conviction and you must try to include steady compounders and stalwarts in your portfolio Eg Asian paints , pidilite etc .

Disc - I am not a sebi registered analyst and this is not a recommendation. Pls do your own research before investing

If you have only around 8-9% networth in equities, you should switch to a high quality portfolio of companies like hdfc bank, asian paints, pidilite, bajaj fin, page inds, 3m, etc and keep doing SIP kind of buying for next few years and get good compounding…

sell all your holdings below 3% and invest into high quality names as suggested.

dig into your GoldBees and to a SIP from there into these high quality names.

Get a Car and house for yourself. Dont think of these purely in terms of “value investing”. They provide the security, comfort and convenience required in life.

Not every thing in life has to be seen from a “paying cents for a dollar” perspective.

Shift from FD’s to some good liquid or debt fund and again start a stock or MF SIP from that.

On Blue chips-

Most of the good companies suggested above are trading at very high PE ratios… I am a little apprehensive as I am not sure at such big scale they will grow as much as is being assumed over the long term… I work in one of the new age companies in Bangalore & have a view that disruption is happening in every sector and will have a big implication on all major sectors be it finance, retailing, manufacturing etc. (This is -ve for existing players as they are not the ones disrupting. Their tech is very poor and business models are not agile. HDFC bank’s app was down for 5 days once!!)

I am also investing in equity MFs which hold these high quality stocks anyway… I am assuming the fund managers know what they are doing

I will buy a house in the next year… the rates are very high so waiting to save some more before buying …

Will explain the rationale behind all stocks soon… I basically look for low PE and strong fundamentals

New age companies are mostly PE money driven and loss making. Comparing them to HDFC is like comparing a newly discovered planet to Earth. If any of those new age companies become sustainable, biggest beneficiaries would be the PE guys. Beyond a level of scale and growth, any new age company has to come to terms with reality as they need to operate in the old world. I would refrain from comparing them to proven stalwarts even though their app remain down for a month. Some of those new age companies would find themselves lucky if HDFC ever agrees to buy them out in their struggle for growth fund and sustainability.

@hitesh2710 sir, would like your views more on this. how the % allocation of networth invested in equities is correlated to the stocks in the portfolio?

In a hypothetical scenario, if the % allocation is say 20% or 30% or 50%, will your recommendation would have changed?

Pardon me, if this is not the right thread to ask this question.

Here the assumption is that the person is learning the ropes of investment and because there is low confidence as is usually the case at the beginning of the journey (and which is also the case after learning too much of it ) its futile to take too many risks in small/midcap space. So the prudent approach is to start with solid companies and as more confidence is there, get more into small and midcaps.

when you first start, its much better to start with quality names. the aim at this stage should be Capital protection than finding out multi baggers.

i think you have realised the pain, your stocks are -20% in a few months while nify has been flattish almost.

Theories of disruption will always be there…i am in my early 30’s so havent seen the tech bubble myself but you see the fact is, internet and technology has really changed the world, but that really doesnt make internet companies some multibagger ? unless ofcourse u r pretty sure of investing in a next google, chances are you are going to get a dud.

Pe ratio itself is not the only metric which should be used for valuation. Even I was wrongly overfixed on pe ratio initially. Pls see this video by Bharat bhai of ASK

I suggest you read the capital allocation thread and Hitesh bhai portfolio thread @hitesh2710 for practical knowledge on investing that has helped me a lot in understanding investing concepts. He has answered a lot of questions of beginners like us in a very practical and approachable manner .

Disruption is a risk however quality companies are very agile and responsive generally just as an example ,hdfc bank and bajaj finance invest heavy in technology to stay relevant.

Recommend you to read Saurabh Mukherjea book "the unusual billionaire " as it contains stories of quality companies like Asian paints , HDFC bank , Berger paints , Marico , page industries . You can also read " one up on wall street " book by Peter Lynch which is the most relatable book to how Indian stock markets work .

Disclosure- I am not a sebi registered analyst and companies stated here are just examples. Pls do your own diligence before investing .

While I agree that HDFC is a sustainable business while the startups are highly risky, HDFC bank is not all that big that they can buy these companies. HDFC bank market cap ~ $40 bn… Paytm is looking at around $16-18bn valuation now, PhonePe is looking to separate from Walmart with a ~10 bn valuation next round… All have plans to enter banking space, disrupt it & own it… Look at China - Alibaba & Ant financial etc. I really don’t know what will happen but I don’t see the same old banks dominating the financial ecosystem of India in the next 10-20 yrs …

HDFC bank is trading at a PE of 27 & PB of 4. This is a lot of future growth baked into the valuation already. Hence my apprehension.

What are valuation parameters for Paytm or PhonePe? Hdfc Bank is a profitable model of many years whereas new age start ups are yet to show money. These banks will reinvent themselves.

While i respect your views but these startups with no profits can see their valuation erode at same pace. No doubt one in ten or fifty could be next alibaba but that will be more gamble than investing. For PE guys they know that risk and kind of drive these businesses to some extent, so they are significant owners than investors…that’s how I see it…btw if u are really that concerned about valuation of HDFC bank, then what would you say about these new age companies…

Banking is a long term business and Banker will be the key show man as seen clearly in case of HDFC Bank,Kotak Bank…

The examples quoted here like PhonePe, Paytm, I am curious to see the CF’s/profits to study if the models sustain in long run. I see lot of criticism by Walmart shareholders when Walmart acquired Flipcart which had -ve CF’s. Let’s see how the future turns out to be for the new age fintech firms and also the expensive buyouts by bigger gaints. AS RJ always says, in the long run the businesses are valued based on steady CF’s and predictability of the same over a long period of time( Same is seen in few FAANG Stocks( Face book, Apple, Amazon, Netflix, Google) ).

Coming to Ant Financial by Jack Ma if I understand correctly, the book is for MSME loans and not retail atleast from what I read. Disruptions are possible and retail investors can catch up in the listed space and also get lucky by having a good management over a really really long period of time. Having said that, HDFC twins are known for quality and at any day there would be buyers for them at a premium as long as the book has good risk, growth is evident, management walks the talk. RBI has certified officially more than once that HDFC Bank, ICICI Bank, SBI have grown so big they are too big to fail. HDFC Bank is probably the highly valued bank in the world

Mr Market is Supreme, Price Discovery will happen eventually( - ve / +ve ) and going by history not to forget expensive stocks could remain expensive.

-If you are looking for Internet Companies in listed space, Check out Infoedge as case study.

<<No recommendations from me, Just my views after reading the communication in this thread>>.

Sorry. I am no expert to say with conviction that HDFC bank is overvalued etc… but I have this view that it is definitely not as solid as far as future growth & dominance is concerned as most people believe. (I am biased due to working in these new age companies for the last 5-6 yrs and see the inevitable direction of where it is heading)

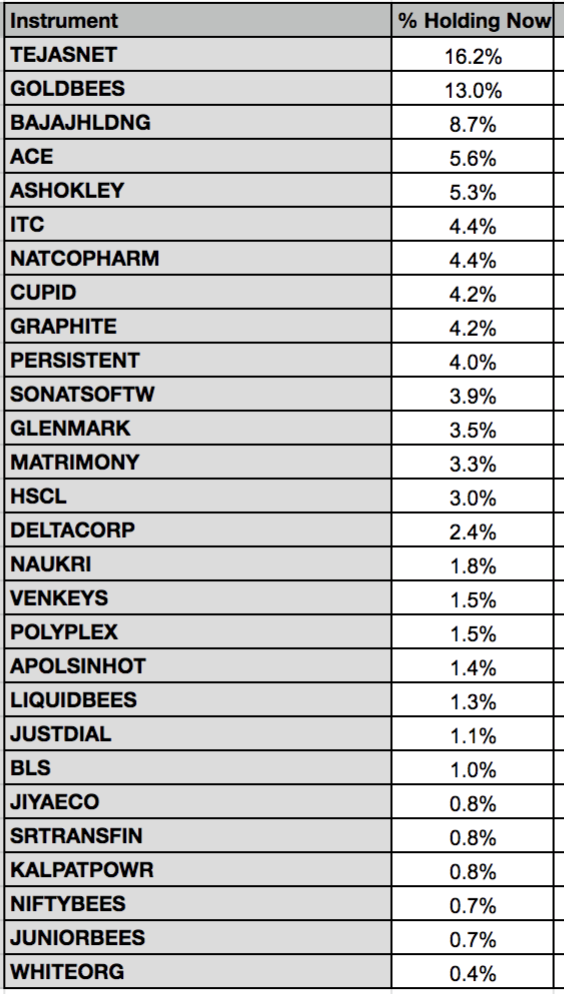

Anyway sharing below how I picked stocks listed above -

TejasNet - I know this company from my undergrad days (2009) as they used to come for campus placement. Have friends who worked there. Management is solid. AR has full disclosure. It has strong tailwinds in terms of make in india in the telecom sector and the upcoming investments in 5G over the next few years. It has zero debt and has been consistently profitable since 2012. Its PE is around 7 now & PB is 0.6!! Most of the book value is cash & receivables. A large chunk of receivables outstanding is from BSNL (which I am betting won’t default on the payment as it is a PSU & tejas management has also said there is no risk of default as government has promised this apparently).

Other risks involve competition from multinationals & risk of failure in international markets where it is venturing now. With these risks also, I feel Tejas should be atleast 2x of its current CMP as this is not a risky company that can default easily. They have globally less than 1% share in their addressable market and they can only grow from here. They have high repeat customers. Getting new customers is difficult for them though which they are trying to improve by hiring more senior Sales people with global connections (Paul Harrison)

Goldbees - Bought these as all my stocks were tanking and thought this might be a good idea. It is flat as of now

BajajHolding - Safer investment… copied from Parag Parikh fund… Again bought it to give more stability to my holdings

ACE - Leader in cranes. PE is 15. They are growing new product lines also profitably. 2 new products (patented) which no one has will be introduced soon. Seems to have potential with India needing to build so many buildings in the next few years

Ashokley - Stock has taken a beating due to drop in sales. I think next half will be really good with BS6 transition making ppl buy more. Longer term, I think this is just riding the Indian GDP growth story… but the problem is electric vehicle disruption here. These guys are tying up with international companies to introduce electric buses etc… so am hoping they won’t be left behind

ITC - High PE but am betting even with e-cigarettes this is a safe company as they have a monopoly on smoking. Again bought this as my smaller companies were bleeding too much

Natcopharm - No proper due diligence

Will edit this and write more later as I am feeling tired now (have fever). Thanks for your replies. Please keep them coming.

you have beautifully captured your thoughts and I am totally in sync to it.

Its worthwhile to stick to high PE + high quality and sustainable growth companies with a moat rather than wandering for low PE,Cigar butt or even value buys.

The companies that @hitesh2710 sir mentioned are the gems of Indian market and they will continue to outperform their small and mid cap brothers and sisters

These names are boring, if some advisor advises these companies, then the investor will ask “ismain naya kya hai”…

In the turmoil for the last 1.5 yrs, those who stuck to these names(including me) have been able to withstrorm the storm.

In addition to the books suggested, I would recommend following Basant Maheshwari.

) its futile to take too many risks in small/midcap space. So the prudent approach is to start with solid companies and as more confidence is there, get more into small and midcaps.

) its futile to take too many risks in small/midcap space. So the prudent approach is to start with solid companies and as more confidence is there, get more into small and midcaps.

but am betting even with e-cigarettes this is a safe company as they have a monopoly on smoking. Again bought this as my smaller companies were bleeding too much

but am betting even with e-cigarettes this is a safe company as they have a monopoly on smoking. Again bought this as my smaller companies were bleeding too much