My own view is that it all depends on one’s risk appetite and time horizon. Over longer term obviously quality small & midcaps will do better than blue chips simply because large companies don’t have too much headroom to grow. If you want to take out money in an year, it might not be a good idea to put it in small caps but if you are ok to stay invested for 10 years, imo small/midcaps should be fine. Of course won’t put 100% of my money in small & mid caps but 20-30% should be fine.

That’s where I differ. The disruption is happening from an area which is outside their core competence. Best they can do it partner with the new age companies & enjoy some benefits for a while…

Can you pls explain in details how the disruption will help these new age companies transform in world class top retail bank of India? It would be really nice to know from someone working closely in same area. Also i am hearing lot of disruption to FMCG brands also by new age trends and companies. If you can throw some light or details on that also, it will be really helpful for us. Thanks

1 Like

Please start with some youtube videos on fintech. (Start with this maybe - https://www.youtube.com/watch?v=nuC-UGxmAks). Read about fintech in China also.

To simplify - Basically, banks make money by charging higher interest on credit which is more than interest they give out on deposits. The processes by which they decide interest rates & credit limit are very basic and this will undergo a lot of disruption with better data and modelling. [There will soon be more differentiation in rates at which credit will be provided to different people and businesses. Having better risk modeling using ML on a variety of data points makes a lot of difference. Also different types of loans and customisations will become available]. Now, in my view the traditional banks in the beginning will tie up with the new age companies as they see value in what they are doing (Eg: Flipkart-Axis credit card. Btw Flipkart is also tracking over 500 data points of its customers to build up a risk profile and will soon start underwriting). Over time, the new age companies will start bypassing the banks more and more and control more of the financial services value chain as they will provide much superior customer experience, convenience and lower costs.

India is a young country which is largely unbanked. So, new age companies won’t even have the difficulty of moving people away from the traditional banks. Lots of people will start using different apps for different financial services before they even enter the traditional banks. Lot of future growth projection of existing banks is assuming these ppl will start with using the traditional banking system which might not happen

2 Likes

Not sure about what you are referring to in FMCG. Middle men will get cut out everywhere first (basically people connecting value creators with customers). Disruption in Manufacturing will be much slower imo though robotics and automation is improving fast

Interesting points, however still in US, a chase bank or wells fargo rules in deposits, a discover, american express or chase rules in credit cards even though deposit rates are close to 0 and loan rates are 2 percent or less. Insurance is still in hands of Geico, new york life etc etc which all are almost century old companies and none of them is a new age, maybe discover is a relatively newer one. Amazon still is king in its area of operations but not many Americans use apps etc. Of any new age companies for their finances. Infact they are wary of new names and look at apps with suspicion. If what you say were to happen, then India maybe first democratic nation where such huge disruption would happen in banks. I do not follow china as it is way too different than us. I may be wrong. But US has more start ups, a better ecosystem for disruption but still old is gold there. Would be nice to know your thoughts. It will be good to learn from someone whose thoughts are very different. Pls note although my points differ from yours, but i am discussing to learn from a new viewpoint. Thanks

2 Likes

@alexander HDFC Bank alone is close to a 100Billion dollar market cap at over 6Lakh crore.

HDFC is close to 40Billion dollars.

HDB is to list soon. Getting a banking licence is an extremely difficult task. Becoming a payments bank and an nbfc is a far more realistic assumption. The RBI will not just give licenses to any financial services start-up. Edelweiss itself could not get one (as they were rumoured to do so)

3 Likes

with so much talk of disruption… i can only quote anecdotal evidence that disruption is evident, but that no way means that companies that disrupt will mint money in long term. A short term spike is always possible based on sentiments.

- Internet - it was a revolution that changed the world. which internet provider has been a multibagger ?

- Mobile phones - it has changed the way people communicate. Which mobile company is minting money ?

- Airplanes - It completely changed the way people travel. But which airline has been consistently growing?

while one can speculate a small amount of his portfolio in such picks, one must stick to quality names that have proven track record.

3 Likes

Interesting discussion.

Comparison with China may not be accurate as the banks state owned, savings deposit rates in banks are capped so as to remove threat of competition. Because these rate caps are so low, it has led to the success of peer-to-peer lending networks and associated fintech.

2 Likes

Watch Aditya Puri’s interview, like I said b4 CF’s and profits matter.

It isn’t the most innovative that wins. HDFC Bank example shows that. ICICI was more innovative and they moved into retail before HDFC. In contrast, HDFC always took calculated risk, they only moved into an area after it has been tested by others, and only where they see profits, unlike most startups who keeps on expanding topline without worrying about where the profits will come from as long as VC funding is flowing. And once HDFC got into an area, with a profitable business model, they delivered the best execution to become the top, or close second, in that area. They could give such execution because of the people driving the bank and its culture. So innovation alone is not enough, it has to be combined with excellent execution, that is where HDFC has already proved itself and that’s why market gives them a premium.

3 Likes

Correct. In this regard I would request everyone to read HDFC Bank 2.0 by Tamal Bandopadhyay. Its ebook is on sell today on Kindle. I bought it and just read the foreward by Nandan Nilekani. I so far think that this book can address the concerns expressed in this thread.

4 Likes

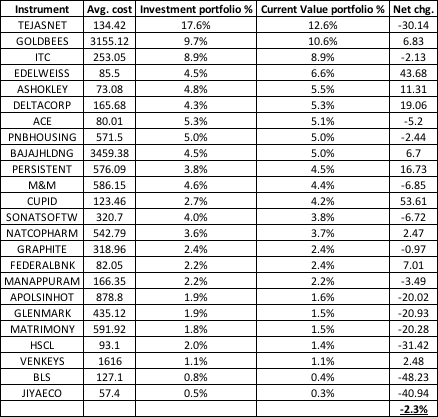

My current portfolio -

Lessons for myself from my investing in the last few months -

- Averaging downwards - When a stock is falling continuously understand more deeply why it is falling before averaging downwards (Tejas)

- Allocation - Do not allocate more than 10% to any stock. Allocate minimum 2% and maximum 10%. Normally allocate 5% => Portfolio should have about 20-25 stocks

- Have a few largecaps in the portfolio to give it stability as it will be very volatile with only small caps

- Do not buy random stocks because they are attractively priced / friend suggested without sufficient understanding (BLS, Jiyaeco, Glenmark)

Other actions to do in the next few months -

- Invest more in PF

- Reduce exposure to FD and invest in a little real estate / debt MFs

1 Like

I would tend to disagree here… 20-25 stocks is too diversified a portfolio.

5-10 stocks should do…

3 good stocks out of 10 will cover all your returns

1 Like

Maybe once I have more experience and knowledge, i can reduce to 10-12… Currently i have lots of hits and misses as you can see… Diversification is more protection against downside. Also, my portfolio value is significant now

Your lessons quite reflect my own lessons from Mr. Market… and to add to it below are some more lessons :

- when any stock falls in the portfolio, ascertain its reasons and get out at the earliest if the fundamentals have changed.

eg - dhfl and rel cap. I suffered from a huge ownership bias.

I am now quite more conscious and ask my self at every step - is this decision affected by ownership bias ? - always book profits (even if partial).

A bird in hand is worth two in the bush.

Its much more important to NOT make any profits than to make any losses. Capital protection is very important.

Eg - i bought dhfl around 250 and didnt even sell anything even after it hit 600.

2 Likes

This Coronavirus correction has been terrible for me. Have lost ~40% of my portfolio value since I started.

Currently planning to realign my portfolio as below -

Safe - HDFC Bank(10%), ITC(10%), Bajaj Holdings(10%), IT basket (HCL, Persistent, Sonata) - 10%, CDSL(5%),

Little Risky - Cupid(10%), Zee(5%), NOCIL(5%), Delta(5%)

Cyclical bet - Nalco and resources sector/PSUs basket(15%)

Remaining - Cash (15%)

In consideration to deploy cash:

Paper basket - Seshasayee & paper sector (5%)

PVR/ Inox (5%), Avanti (2.5%), IDFC(2.5%)

Any feedback is appreciated. I am willing to take moderate risk. I am ok to lose 20% value to have a chance to make 10-15% on average over 10 years. -40% is hard to recover from I guess. Luckily this money lost is not affecting anything major in my life.

@hitesh2710 Sir, I should have heeded your advice earlier ![]() I may have learnt the lesson to buy quality stocks the hard way (hopefully). Adding HDFC bank now

I may have learnt the lesson to buy quality stocks the hard way (hopefully). Adding HDFC bank now

I am thinking of a new framework to think of companies -

1.Dividend stocks - Give stability to portfolio

20-40% of the total portfolio depending on market scenario

5-10% investment / stock => 2-8 stocks

Atleast 3% div yield for past 3 yrs and projected to increase in future

High visibility of steady future revenue and profits (no cyclicals)

Bigger companies with mCap > 5000 Cr

Hold:

SJVN

ITC

PowerGrid

COALINDIA

Watchlist:

BSE

Thyrocare

Hero Moto

GAIL

Sun

2. Consistent compounders - Accumulate at opportune moments and hold for long term for consistent value growth

25-50% of portfolio depending on market. As a rule prefer this over Dividend stocks if both types are available

Min 5% and Max of 12.5% per stock =>2 to 10 stocks

Target = 10-15% CAGR growth

Consistent High ROE > 15% + Consistent Sales growth of atleast 10%

Fair to Low valuation relative to its intrinsic value

No management red flags

Big market - High scope for future growth

Strong moat which can last for long

Big companies in a core sector : Market cap > 5000 Cr

Holdings

Bajaj holdings + Mah scooters

HDFC. bank + HDFC

Watchlist

HCL

3. Cyclical bets - Buy during downturns and sell when things are going well

0-20% of the portfolio depending on opportunity

4% per stock maximum, max 2-3 sectors with 2-4 companies per sector

Target = 3-4x potential in a 3-5 yr cycle

OPM should be near the lows when buying and should be at historical high when selling

No debt i,e, ability to survive during downturn. Preferably pick lowest cost producers in the market if everyone has debt

Preferably high BV which gives some lower bound

Fair management which gives out dividends

Always pick a basket of stocks as these are commodities majorly and behave similarly

Holdings

Vedanta

ONGC

ASHOKLEY

M&M

ACE

Watchlist stocks and sectors

Papers

Eicher motors

Maithan Alloys

Oil India

Nalco

NMDC

Indigo

4.Future stars - Risky bets with big potential

20-30% of portfolio

1% to 5% allocation per stock depending on conviction and risk => 4-10 stocks

Target = Min 4x in 5 yrs if investment thesis plays out

Smaller companies with mCap < 5000 Cr

Riskier the company lesser the allocation %

Accumulate upwards as story plays out

Holdings

Sonata Sw

Persistent sys

Zee

Cupid

Nocil

CDSL

IDFC

DELTACORP

VENKEYS

Natcopharma

TV Today

Watchlist stocks

Bombay Burmah

ION Exchange

Avanti Feeds

5. Short term undervaluation plays

10% to 20% of portfolio

2.5% - 5% per stock, Max of 4-5 stocks based on opportunity

20% to 50% upside in 6-9 months

Downside should not be more than 20% per stock

Holdings

PNBHOUSING

EDELWEISS

MANAPPURAM

GLENMARK

APOLSINHOT

MATRIMONY

Watch List

Cochin shipyard

DB Corp

PVR, Inox

Justdial

Newgen Software Technologies Ltd

Zensar Technologies Ltd

BALAMINES

Hexaware Technologies Ltd

I want to sell (but haven’t) -

PNB Housing, Edelweiss (Too much debt)

M&M and ACE (Don’t really have conviction)

Glenmark, Natco pharma (Don’t really understand pharma)

Apollosinshot (Shouldn’t have bought this in the first place. Bought it based on a planted ET article initially)

Other Cyclicals - I’ll hold now as no point booking losses at such lows

I’ll invest more in good stocks - HDFC, ITC, Bajaj Grp, Zee, CDSL, SJVN,

Little money in Cochin shipyard, DB Corp, Sonata, Cupid maybe

Selling and booking losses is difficult… Have been postponing.

Please share your thoughts on this approach.

Thanks for sharing your thoughts, I have a few comments on which I would love to know your thoughts.

- The cyclical bets and undervaluation part of the portfolio can be combined into one category, the basic idea is to take cyclical bets when they are available at a bargain

- Dividend stocks: SJVN, BSE, GAIL are very cyclical businesses and should belong to the cyclical part of the portfolio. You can use variance in operating margins to quantify the degree of cyclicality in a business. Alternatively, look at EPS trends over a decade.

- M&M & Eicher belong to auto sectors which is cyclical but are not deep cyclicals (like NALCO, NMDC, etc.).

- Future stars: NOCIL, Venky’s, Deltacorp, Avanti feeds are cyclicals

- Losses: It is more prudent to book losses than profits. Don’t look at your buying price, but look at your estimate of value 5 years down the line for each company and allocate accordingly. If it involves booking profits/losses, then so be it!

Going through your thread, it seems that you are changing your investment rationale according to share price movements, which can be bad for long term returns. Pick up a strategy and stick with it. Also, you might want to think if you are switching to GARP because it has done well in the recent past or it resonates with your personality. GARP stocks tend to do well in risk off environments, and cyclical bets tend to pay off in roaring bull markets. Hope it was useful!

Cheers

Harsh

1 Like