This may not be revenue but outstanding payment …

1 Like

@Ashish_Munjal Thanks, Still not clear which quarter this will show in the quarterly result Q1 or Q2?

Hello everyone,

There is seasonality in business in first quarters. What could be the reason of that?

@ankit_george

Disc: i have a tracking position.

1 Like

Few insights from Q1 Fy24

Missed the first few minutes. Kindly check the concall for complete info

- Fluence energy asking MTAR to manufacture in Europe and USA. Company exploring the plans

- orders from bloom received that are to be executed by end of Dec. Further orders for next CY expected in Q2 or Q3

- 40:60 would be the fraction of revenue in H1 and H2 FY24

- for clean energy, expect to do 590 cr revenue in clean energy in FY24

- revenues from space to be 70 CR in FY24

- need a new facility for Fluence business. Overall margins to be same as bloom business. But comes with Operating leverage and so overall better Ebidta

- current revenue of Nuclear segment is 180 cr. Expect 500 crs of revenues coming in by end of the year (from 2 nuclear plants). Orders for 10 more reactors to be given out soon ( called mega projects, to be executed by private players instead of NPCIL)

- 28% margin target to be achieved for the FY24

- Working capital days to be 200 days by FY24 end, thanks to operating leverage, monitoring, etc.

- Defense license enables us to directly supply to Army, Navy. Enables us to work with Multi national. To receive the license soon( in few days)

- Capex for FY 24 to be 40-45 cr icluding 20-25 cr for Fluence energy.

- 10 more crore for Fluence in next FY

- Nuclear 60, space 70, Defense 15, products and others to be 125 crs. ( personally expect the guidance to be revised upwards or at least over achieve)

- added about 20 people to work on SSLV. Cost is reasonable, as they’re working in existing facilities. No major cost other than mna power

- Working with lot of defense organizations in India. In the process of qualification

- Gross margins are to be around 60% on average

- Fluence energy factories to be outside in US and EU. Some employees would be posted there. The project is very large revenue base. Large interest from the customer

- gross margin to improve to 52% in next quarters from 49% currently, driven by higher domestic share

- diversifying the revenue across customer base

- reiterated 3000 cr revenue target by Fy 28 With more diversified revenue.

- Fluence shortlisted MTAR as the only supplier. Looking at 10000 units ( of energy storage units) for US, once ramped up in US

Disc : invested

Not a comprehensive coverage of the call. Please listen to the concall for more insights

Thank you

10 Likes

Because they know the company does not make cash flows and will never make cash flows.

1 Like

Mr. Srinivas Reddy delves deeper into the company’s performance and future projections:

Bloom Hot Boxes and Sheet Metal: In Q1, they produced 950 Yuma hot boxes with 32 electrolyzers. They have a clear dispatch plan from Bloom for the current financial year. In Q2, they plan to produce 418 Yuma hot boxes, 440 Yuma Santa Cruz hot boxes (an advanced version of Yuma), and 66 electrolyzers. In Q3, they aim for 1,144 Santa Cruz hot boxes and 44 electrolyzers. In Q4, they target 1,718 Santa Cruz hot boxes. They also anticipate new orders for electrolyzers by the end of the year.

Santa Cruz: This is an advanced version of Yuma that generates 65 kilowatts as opposed to Yuma’s 50 kilowatts. They’ve worked with Bloom over the past quarter to make design changes to increase the output of the Yuma unit.

Ebitda Percentage: They had given a guidance of 28% ± 100 basis points and continue to maintain this margin guidance for FY24. The EBITDA margin for this quarter is at 22.4% and is expected to improve quarter-on-quarter based on higher revenues.

Order Book: As of June 30, they have a closing order book of 1,078 crores. They received orders worth approximately 50 crores in the first quarter. They expect major orders from clean energy, nuclear space, and defense in the upcoming quarters.

Defense License: Their defense license has been cleared by the Ministry of Defense’s committee. They expect to receive the license by the next week, allowing them to supply directly to the Air Force, Navy, and associate with multinationals for major defense projects.

New Collaborations: They have two significant collaborations in the pipeline: Fluence Energy and Enerven. Fluence Energy is in the final stage of releasing a letter of intent for 1,000 units with prototypes, which will be executed in FY25. They expect to export to Asian countries, Australia, and New Zealand. They are also in discussions about establishing branches in Europe and the USA, which could generate substantial revenues for the company.

Energy Storage Systems: They are in discussions with two companies, Fluence Energy and Enerven. Fluence Energy is in the energy storage system sector and is close to releasing a letter of intent for 1,000 units with prototypes. Enerven uses nickel-hydrogen batteries instead of lithium, offering another exciting prospect in the energy storage system.

Product Development: They have submitted the first articles of Road exclusively to DRDO, which has been tested under various conditions. They are also supplying four different types of Electromechanical Actuators (EMAs) this financial year, amounting to about 7.5 crores. The business of EMAs will grow year-on-year. They are also starting a new product called “dielectrics” this quarter, which has a potential business of about 250 crores per year.

7 Likes

Profit guidance of 145-150 cr. FY 24 Forward pe is ~50. I’d say it’s reasonable for a Co growing at 40-50% CAGR

2 Likes

I was even wondering the same. The revenue recognition accounting policy also does not shed light. Curious to understand

Per AR22-23 pg 39, co expects to fund this through internal accruals and debt. They expect to maintain same debt equity ratio of 0.23

1 Like

Grant of Industrial License (Defence) from Government of India/ Ministry of Commerce & Industry/Deptt.

4 Likes

Most of the Govt organizations complete orders in Q4, that’s why Q4 is the strongest quarter and Q1 will see very less deliveries to Govt customers.

1 Like

The stock is trading close to the previous high it made in Dec 2021 and nil returns in last 20 months. I believe this price will act as support unless the whole market corrects

Valuation wise the Co is trading at 50-55x P/E (Management guidance of 145-150cr profit, which I believe they’ll revise upwards soon). The management has provided great details in Annual report and combined with the positive commentary shared by the Co in latest quarterly concalls, I believe they can grow at 30-35% Cagr until FY28.

So I belive the Co is fairly valued and can give 25%+ cagr returns for next 4 years (being on the conservative side)

Just wanted to share these few points for the benefit of everyone

Praveen

Disc: No reco. Holding the stock in PF

5 Likes

First time since I followed MTAR from last 2 years seen revenue guidance missing this much. now 18% growth instead of 45%. Mr Reddy said this below in last Qtr concall. Not questioning company’s long term story here but little bit of faith on Mgmt is lost. I continue to hold and will add on dips.

3 Likes

My sense is (and I could be wrong here) this is likely due to Bloom Energy pushing its order delivery dates to future. Situation in US is really difficult right now due to sky high interest rates which is choking new investments by all businesses and even putting current plans on hold. If it is indeed this reason then this pain will linger for next 2-4 quarters at least if not more. Let us see how market discounts this tomorrow.

4 Likes

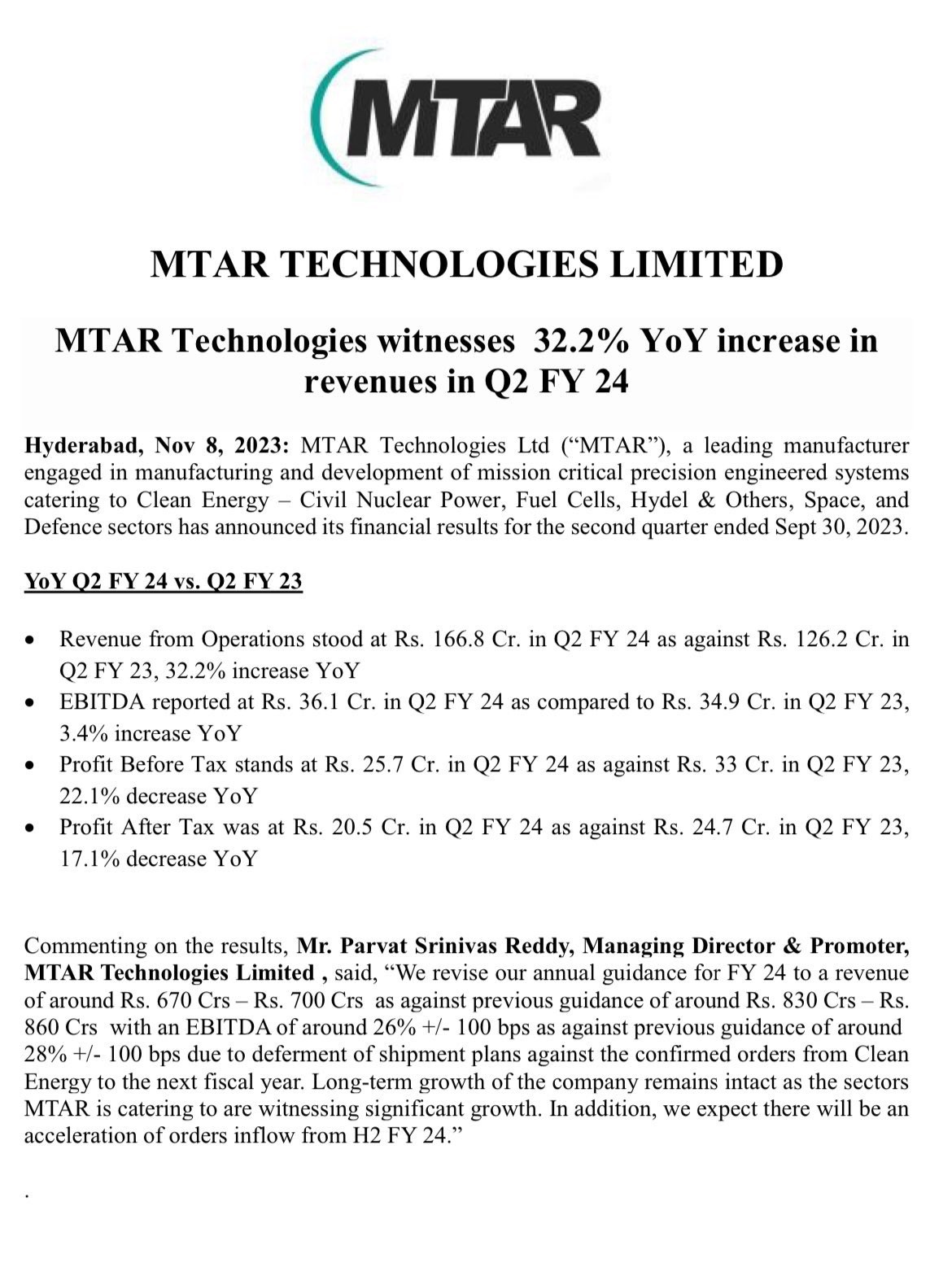

Mtar Technologies just announced their financial results for the three months from July to September 2023.

Here’s how their business did compared to the same time last year:

- They made 32.2% more money from their operations.

- Their earnings (EBITDA) increased by 3.4%.

- The profit before tax decreased by 22.1%.

- The profit after tax dropped by 17.1%.

Mr. Parvat Srinivas Reddy, explained that they had to change their financial expectations for the whole year. They now think they will make around Rs. 670 Crs to Rs. 700 Crs, which is less than they thought before. This change is because they had to delay sending out some of their orders to the next year. However, he still believes the company will grow in the long run because the areas they work in are growing. They also expect to get more orders in the second half of the year.

1 Like

I have exited the stock as of yesterday. I’m not comfortable with holding a 65+ PE stock with a 15% growth in top-line! Will keep it in my watch-list though and add it if things seem better.

4 Likes

The MTAR Technologies Ltd Q2 FY24 Earnings Conference Call discussed several key points:

Performance Overview: MTAR Technologies reported revenue of ₹166.85 crores, with a 3.4% year-on-year increase in EBITDA at ₹36.1 crores for Q2 FY24. However, there was a decrease in profit before tax and profit after tax compared to Q2 FY23.

Order Book and Growth Projections: The company anticipates a healthy order inflow in the second half of the year from new and existing customers in the clean energy, nuclear, and defense sectors. This is expected to maintain the closing order book around ₹1,400-1,500 crores. They have received around ₹80 crores of order inflows in Q2.

Clean Energy Sector - Bloom Energy: MTAR is focusing on the production of Santa Cruz block 2 hot boxes for Bloom Energy, moving from the previous Yuma model. There was a deferment of shipping plans from Bloom, impacting MTAR’s short-term growth. The company expects to ramp up production of Santa Cruz block 2 in the coming quarters. They also mentioned ongoing negotiations with Fluence for a substantial order.

Domestic Business Outlook: The company expects a significant pick-up in domestic business, particularly in the nuclear sector. They also highlighted the ongoing projects and the expected increase in revenues from these domestic ventures.

Financial Aspects: The company is working on reducing networking capital days by the end of the financial year. There was a mention of a sharp reduction in payable days due to liabilities paid for inventories purchased in previous quarters.

Guidance for FY24: MTAR aims to generate revenue of around ₹600-700 crores by the end of FY24, with an EBITDA margin of 26% ± 1%. This guidance reflects the current business scenario and the company’s strategic focus areas.

Investments and Future Plans: MTAR is investing in enhancing its product portfolio and expanding its customer base. The company is actively participating in the space and defense sectors, with a focus on import substitution opportunities like ball screws, water-lubricated bearings, and roller screws.

Challenges and Adaptability: MTAR discussed adapting to changes in technology and market demands, particularly in the clean energy sector with Bloom Energy. They emphasized their readiness to meet evolving customer requirements.

Open Invitation for Plant Visits: The management invited investors to visit their facilities to witness the company’s advancements and future project developments firsthand

10 Likes

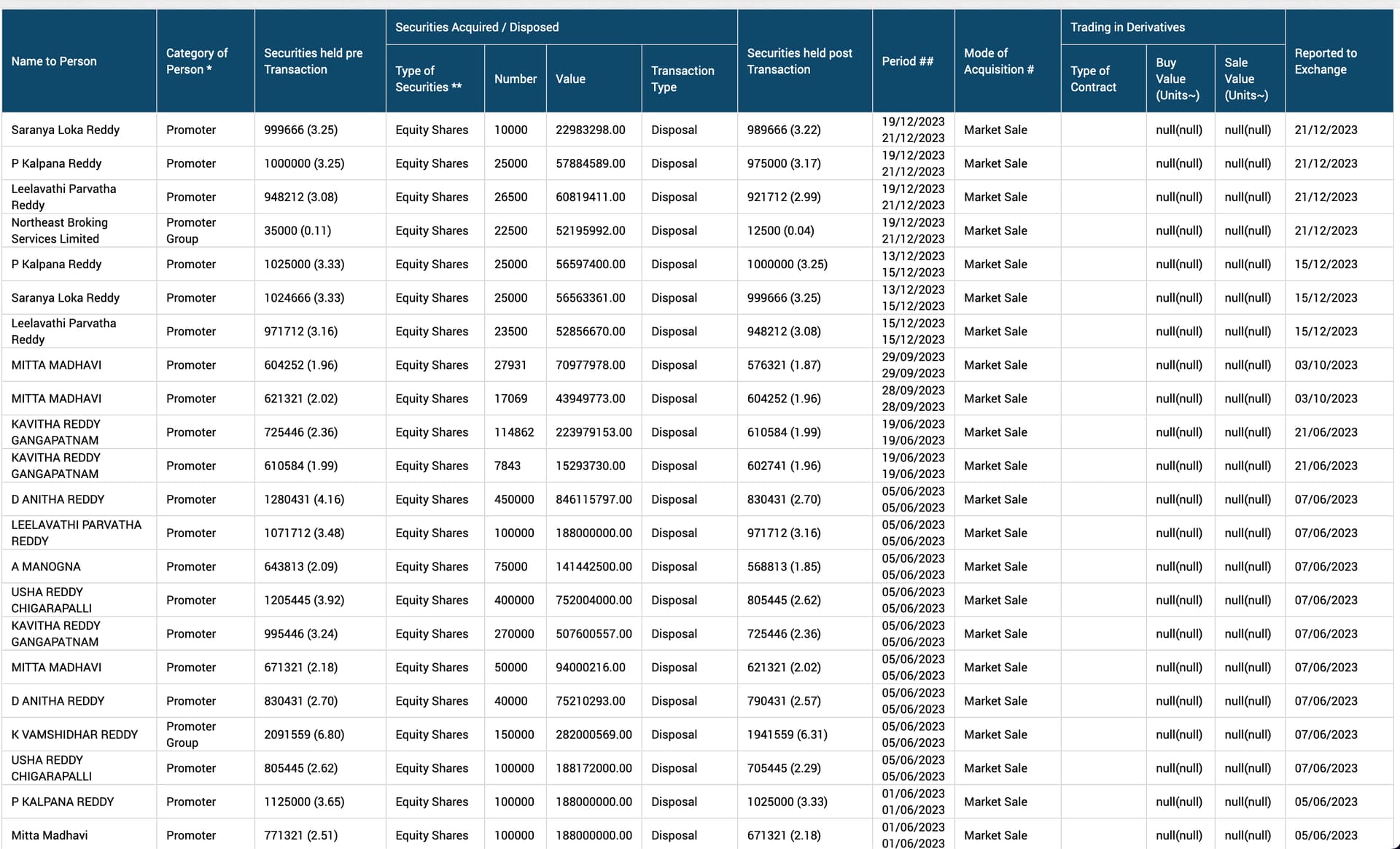

In many companies, I see some promoters selling and others buying. However, MTAR promoters have been on a selling spree since a long time, more such in this December.

Makes me a little bit cautious.

1 Like

I believe those selling promoters are not the active management … I guess, but the selling shares are transferred through gift from the MD. Hence the promoters are cashing out at regular intervals, which is might not provide any direction about the business activities…

I think they are significantly cashing out, and even today two people from Reddy family disposed share. Could this be preventing the share price from going up? I don’t see any point in holding a 67 P/E company where promoters keep on disposing in the open market.