Need I say more what is the problem?

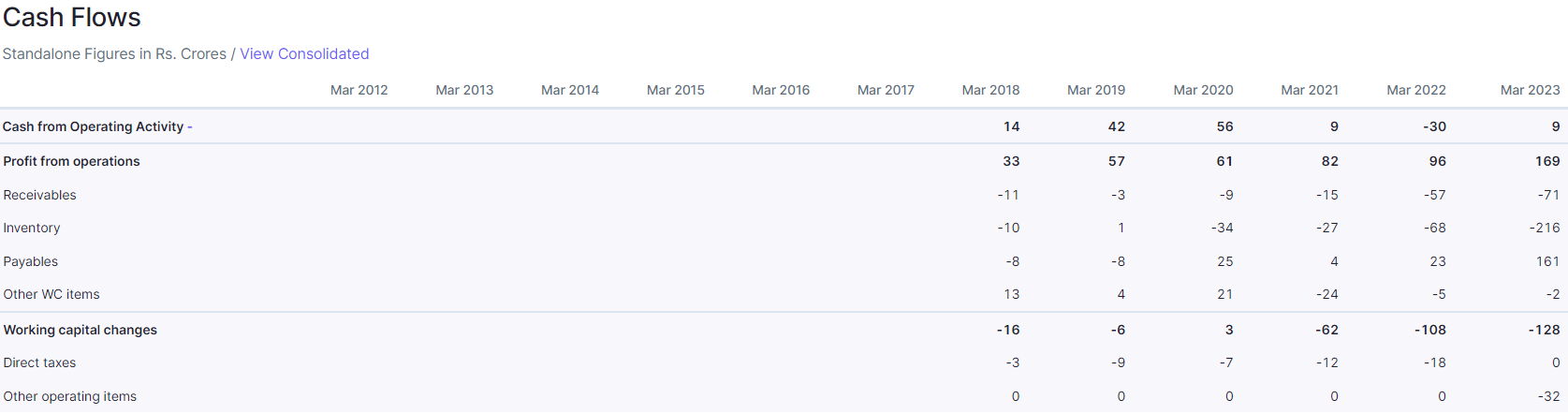

In the concall u may notice the acknowledgement of the same " * MTAR is carrying a high inventory of Rs. 240 crores, with Rs. 72 crores in transit, which they will receive in 60-75 days.

- The company is taking a calculated risk by keeping inventory carrying costs into consideration, and plans to maintain less than 200 days of working capital by the end of the financial year." As these are declared/discussed and corrective measures too are being efforted… Market is discounting it.

Breaking:

GE Aerospace announced today that it has signed a Memorandum of Understanding (MOU) with Hindustan Aeronautics Limited (HAL) to produce fighter jet engines for the Indian Air Force on the sidelines of PM visit to USA.

GE Aerospace is a subsidiary of General Electric which is one of the customers of MTAR Technologies under the Defence and Aerospace segment. GE Aerospace has operated in India for more than four decades with wide engagement in the industry including engines, avionics, services, engineering, manufacturing, and local sourcing.

MTAR has been supplying Hi-Precision Machined, fabricated systems to HAL too.

Will have to see if this news would have an impact on MTAR’s potential orders.

8 Likes

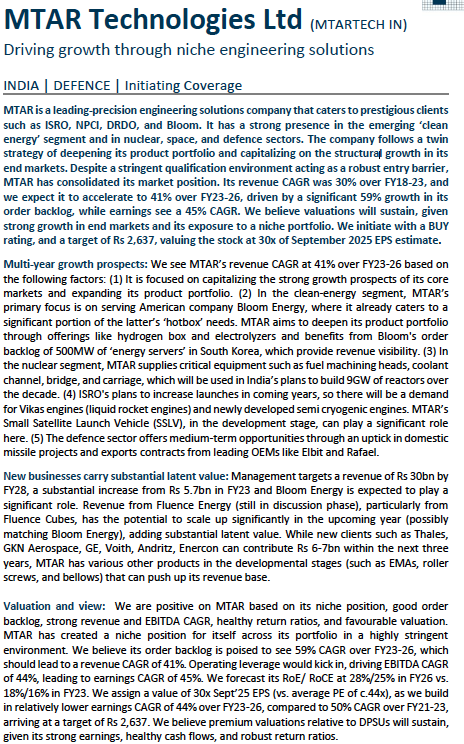

I am glad that the robust revenue growth aspirations of management are getting captured by equity research analysts.

Personally, as long as annual revenue growth remains above 40%, and EBITDA margins are anything above 25%, I am going to enjoy the ride.

8 Likes

Will agree whole heartedly that it was a calculated risk if next year’s PAT is close to cash from operations. If CFO remains poor, then its not a calculated risk, it is a poor business fraught with risk.

BTW acknowledging your business is weak, does not make your business strong.

Absolutely correct. Also this margins would only improve once the mix of nuclear increases. Massive business coming from Nuclear in next few years

3 Likes

how would one value this stock? Seeing that the current PE is 62?

The management projects that they can do 3000 cr revenue by 2028. With 16% profit margin, profit would be 480 cr. Consider pe of 30-35 in 2028. Growth works out to be 20-24% cagr

3 Likes

Keeping an eye on this development “one significant thing is we are now

going to work on the fuel storage systems like Fluence Energy from

US they approached us and we are in advanced discussions with them

that is going to be very big boost to the numbers moving forward over

the next one year or so”

2 Likes

Skimmed through AR22-23. Very strong and coherent narrative. My notes and take aways from AR 22-23:

- Clean Energy will remain the main driver for revenue in near to medium term. MTAR is targeting entire spectrum of Clean Energy (Bloom business, Nuclear, Fuel Cells, Battery Storage, Hydro power, Green Hydrogen etc.). In addition, Aerospace vertical is also a major focus area for growth

- While Bloom business is truly well established and reached alarming proportion for MTAR, contribution from other businesses such as Nuclear is on slow lane due to delays in decision making

- Commercial Space launches are at least 4-5 years away if not more

- Defense and import substitution (roller screws etc.) opportunities are also going to be very small in comparison to Clean Energy

- Sheet metal fabrication business, Cable harness business and specialized fabrication (especially for Hydro segment) can become good contributors going forward. Specialised fabrication vertical shall be operational in a full fledged way from Q2 FY 2023-24

- MTAR is working on the development of cable harnessing assemblies for Clean Energy - Fuel Cells sector and expects qualification process to be completed by H1 FY23-24 Cable harness Batch Production expected to commence from H2 FY 2023-24

- MTAR is in final stages for getting defense license from GOI. They claim post the license they can approach various MNC companies for collaboration to fulfill obligations under Make in India

- While MTAR has developed capabilities of manufacturing Electrolyser (Dispatched 138 units of electrolysers in FY 2022-23), this seems to be slow growth business in near term as Bloom is still demonstrating the enhanced performance of its machines through pilot installations. For green hydrogen to go main stream for Bloom, scale is very important which will bring down the cost of electrolyser significantly as well. Importantly, MTAR is trying to do some back ward integration in this area by Initiating development of Heaters that are used in electrolysers (Currently, heaters are imported; Indigenisation of heaters will enable MTAR to save the costs incurred for manufacture of electrolysers)

- As per MTAR “Our Company does not have dedicated production lines to manufacture identified products and our facilities are fungile across all the sectors that gives us a greater flexibility in terms of utilization of our capacity.”

- In Clean Energy - Fuel Cells sector, majority of raw materials are procured from customer directed sources and the company will entering into price contracts with vendor an year ahead; any subsequent increase in price is a pass through. In certain instances, specifically in Space sector raw materials are directly procured and supplied by our customers. The Company doesn’t have any long-term contracts with any of our raw material suppliers, however, we have maintained long term relationships with our major suppliers that enable us to obtain good quality raw materials within the prescribed timelines (is this the reason for excess inventory???)

- The company is in final stages of discussions with Fluence Energy that is into battery storage systems for supplying enclosures to their batteries. It has potential to generate Rs. 150 - 200 Crs over the next couple of years, once the discussions are materialized. Looks like it will be a slow ramp up with Fluence as current focus is only on battery enclosures

Narrative is indeed very strong and management is making all right noise in AR. Let us see if execution turns out to be equally strong.

Management promises to track over near to medium term:

- Reduction in WC from 230 to 200 days (end of FY23-24) and eventually to 170 days (2-3 years later)

- Growth in Aerospace vertical - MTAR is guiding overall 40% YoY growth (15-20% from ISRO and 45% - 50% YoY growth in revenues from Aerospace vertical from MNC customers)

- Up to 500Cr worth of orders from civil Nuclear Energy (timeline is not clear)

- The company targets to execute around Rs. 120 – Rs. 130 Cr orders in products category ( ball screws, roller screws, water lubricated bearings, ASP assemblies etc…) in FY 2023-24

- Quantum of revenue growth from Sheet Metal, Specialized Fabricated Structures and Cable Harness business

- EBITDA of 28% +/- 100 bps.

- closing order book of at least Rs. 15,00 Cr by end FY 2023-24

- Revenue growth from new customers like GE Power, Collins Aerospace, Thales, GKN Aerospace, Fluence etc. over next 2-3 years. This is critical to reduce the massive dependence on Bloom

- Growing topline to 3000 Cr over 5 years

Just my 2 cents to aid understanding of MTAR business

Disclaimer: Invested, biased and could be susceptible to willful blindness. No investment advice. Please do your own due diligence.

20 Likes

India’s state-controlled nuclear power industry is considering allowing greater participation of private firms, with an aim to developing small modular reactors to help decarbonize industry.

Can this be a future opportunity for MTAR?

The current product portfolio of MTAR in Nuclear includes complex assemblies such as fuel machining head, drive mechanisms, bridge and column and coolant channel assemblies, among others. These products are supplied for the new pressurized heavy-water reactors (PHWR) & existing ones too.

Even if some company other than MTAR gets to develop small modular reactors, the critical assemblies involving high positional and dimensional accuracy would eventually come from MTAR, given that it’s already been a established and reliable supplier to existing reactors.

MTAR previously had signed a MoU in Space for design and development of a two-stage to low-earth orbit all-liquid small satellite launch vehicle powered by semi cryogenic technology with a payload capacity of 500 kilogram. So the ambitions of MTAR are well known. May very well expand these ambitions into Nucelar too.

Disclaimer: Invested, biased.

5 Likes

New development at bloom energy but at present I don’t know how much MTAR get’s benifit in this value chain

Opportunity for this for bloom energy seems to be large

2 Likes

June-23 Numbers Out here -

| June-23 | YOY (Jun-22) | YoY% | QoQ (Mar-23) | QoQ% | |

|---|---|---|---|---|---|

| Income | 1525.00 | 910 | 68% | 1963.00 | -22% |

| Net Profit | 203.00 | 162 | 25% | 310.00 | -35% |

if anyone is planning attend concall tomorrow and gets chance to ask question. please ask what mgmt thinks about shareholding pattern. I understand this has been discussed here as incative family promoters but now we are at bit worry stage. excluding pledging, its just 33%. what kind of risk we see if this trends continue and they enter below 30?

3 Likes

I was going through the Investors presentation for Q1 there is mention that they received 87 crores from Bloom energy at first week July

My question here is whether this amount would have been already added to the revenue of Q1 or will it be added to the revenue of Q2. As the amount is nearly 50% of the Q1.

1 Like

If things are so good at MTAR then why promoters are continuously reducing their stake?

4 Likes

They are also human and they also might have ambition. What’s the use of money and big company if they are not enjoying their life with the money they have.

In this case, the promoter who sold is non-active promoter. As long as company is doing well, we should not be looking each activity with microscope and sense of suspicion.

DISC: Invested.

4 Likes

MTAR Technologies reported strong consolidated quarterly results for June 2023, showing significant growth in net sales and net profit compared to the same period in 2022. The company’s stock also performed well, delivering impressive returns over the last 6 and 12 months.

-

Net Sales: Rs 152.56 crore in June 2023, up 67.64% from Rs. 91.01 crore in June 2022.

Net Sales: Rs 152.56 crore in June 2023, up 67.64% from Rs. 91.01 crore in June 2022. -

Quarterly Net Profit: Rs. 20.34 crore in June 2023, up 25.41% from Rs. 16.22 crore in June 2022.

Quarterly Net Profit: Rs. 20.34 crore in June 2023, up 25.41% from Rs. 16.22 crore in June 2022. -

EBITDA: Rs. 38.62 crore in June 2023, up 34.28% from Rs. 28.76 crore in June 2022.

EBITDA: Rs. 38.62 crore in June 2023, up 34.28% from Rs. 28.76 crore in June 2022. -

EPS: MTAR Tech EPS increased to Rs. 6.61 in June 2023 from Rs. 5.27 in June 2022.

EPS: MTAR Tech EPS increased to Rs. 6.61 in June 2023 from Rs. 5.27 in June 2022. -

Share Price: MTAR Tech shares closed at Rs. 2,292.55 on August 10, 2023 (NSE), with significant returns over the past 6 and 12 months.

1 Like