No one is valuation expert! Whatever you did is correct!

Good Con call.

-New Business segment inside E-Commerce would be Real Estate portal. Not only auctioning portal but a value added services. This is for Private sector and Rural bank NPA properties; Public Sector banks are yet to come on this portal, will take time

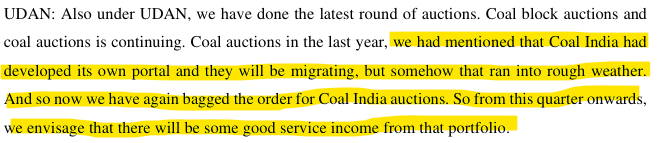

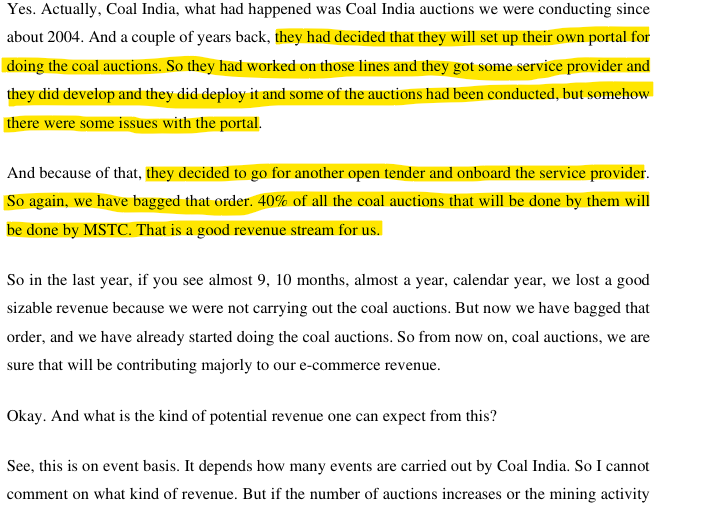

-Coal India back to business for using MSTC as auctioning portal for another 2 year, ~30% blocks will be sold on MSTC.

-Scrap JV business, details were not given much

3 Likes

Coal India I thought was 40% blocks on MSTC. More important is its back. You have covered major points. Thanks

2 Likes

-

The Ministry of Environment, Forest and Climate Change (MoEF&CC) notified the Environment Protection (End-of-Life Vehicles) Rules, 2025 vide S.O. 98(E) dated 06th January, 2025 for environmentally sound management of end-of-life vehicles. The rules are based on the principle of extended producer responsibility (EPR) where producers of vehicles are given mandatory EPR targets for scrapping of end-of-life vehicles. The rules cover all types of transport and non-transport vehicles, except agricultural tractor, agricultural trailer, combine harvester and power tiller.

-

Under the said rules, producers have been mandated to fulfil the obligation of Extended Producer Responsibility for the vehicles that the producer has introduced or introduces in the domestic market, including vehicles put to self-use to ensure the specified scrapping targets. Producers have been provided annual targets for scrapping of End-of-life vehicles starting from the year 2025-26 for the vehicles put in the market 15 years ago in case of transport vehicles and 20 years ago in case of non-transport vehicles.

-

Registered Vehicle Scrapping Facilities (RVSFs) have been mandated to receive unfit vehicles or End-of-Life vehicles for scrapping and must carry out treatment, depolluting, dismantling, segregation and scrapping activities. They are required to send all the recovered and segregated materials from End-of-Life vehicles to the registered recyclers or refurbishers, co-processors for recycling and reuse of components or materials, in case RVSF does have recycling or refurbishing facility. They are further required to send all non-recyclable or non-refurbishable materials and non-utilizable hazardous materials to Common Hazardous Waste Treatment, Storage and Disposal Facility authorised under Hazardous and Other Wastes (Management and Transboundary Movement) Rules, 2016.

-

Designated Collection Centres by producers are required to handle the End-of-Life Vehicles in an environmentally sound manner and send them to Registered Vehicle Scrapping Facility. Registered owner of the vehicle or bulk consumer is required to deposit the End-of-Life vehicle at any of the producer’s designated sales outlet or designated Collection Centre or Registered Vehicle Scrapping Facility within a period of one hundred and eighty days from the date the vehicle becomes the End-of-Life vehicle.

-

Under the rules, Central Pollution Control Board (CPCB) in case of producer and State Pollution Control Board (SPCB) in case of RVSF and bulk consumer may, after giving an opportunity of being heard, suspend or cancel their registration, in case of violation or non-compliance of any provisions of these rules. Returns in respect of obligations provided under the rules are required to be filed by producer, bulk consumer and RVSF on centralised online portal.

-

CPCB has been mandated to undertake periodic inspection and audit of the producer to ensure that such facility is complying with the requirement under the provisions of these rules. CPCB may undertake or cause to be undertaken by an authorised agency the periodic inspection and audit of the Registered Vehicle Scrapping facility. CPCB may take necessary actions against violations or for non-fulfilment of obligations under these rules against a producer or Registered Vehicle Scrapping Facility or any other person.

-

Similarly, SPCB has been mandated to undertake periodic inspection and audit, or cause to be inspected by an authorised agency, of the RVSF to ensure compliance of the rules. SPCB is required to undertake periodic inspection and audit, or cause to be inspected by an authorised agency, of the Registered Vehicle Scrapping Facility to ensure the compliance of these rules and may take necessary actions against violations or for non-fulfilment of obligations under these rules against a Registered Vehicle Scrapping Facility or bulk consumer or any other person.

-

In case, producer or Registered Vehicle Scrapping Facility or bulk consumer fails to comply with the provisions relating to handling and scrapping of End-of-Life vehicles in environmentally sound manner under these rules, are liable to pay environmental compensation for causing loss, damage or injury to environment or public health.

-

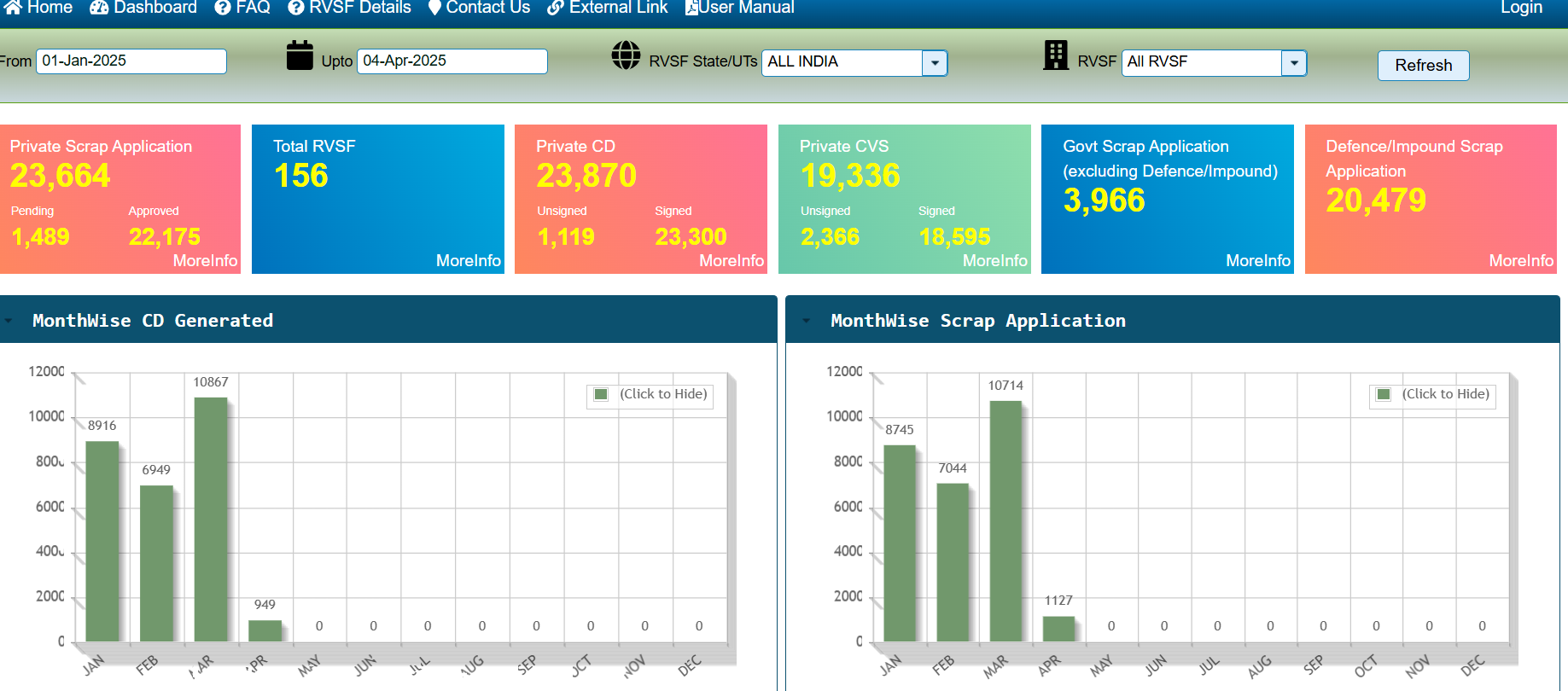

Ministry of Road Transport and Highways (MoRTH) has formulated the Vehicle Scrapping Policy for creation of an ecosystem to phase out older unfit and polluting vehicles. The policy targets scrapping of unfit and polluting vehicles strictly based on their fitness. Under this policy, a network of Registered Vehicle Scrapping Facilities (RVSFs) is envisaged across the country. As on January 2025, 84 RVSFs are operational in the country.

-

MoRTH notified the Motor Vehicles (Registration and Functions of Vehicle Scrapping Facility) Rules, 2021 prescribe for registration of Registered Vehicle Scrapping Facility (RVSF), criteria for scrapping vehicles, scrapping procedure, audit and certifications for functioning of RVSFs. In addition, RVSF is required to comply with the guidelines ‘Environmentally Sound Management of End-of-Life Vehicles’ issued by CPCB.

-

MoRTH notified the Central Motor Vehicles (Twenty Third Amendment) Rules, 2021 vide GSR 714 (E) dated 04.10.2021, which provide that if a buyer of a new vehicle submits ‘Certificate of Deposit’ of an end-of-life vehicle then the Registration fee on the new vehicle will not be levied. Further, MoRTH under the Central Motor Vehicles (Twenty fourth Amendment) Rules, 2021 vide GSR 720 (E) dated 05.10.2021 provides for concession in the motor vehicle tax upto twenty five percent in case of non-transport vehicles and fifteen percent in case of transport vehicles.

6 Likes

Current valuations seem very reasonable, even if growth is slow from here this seems like a good opportunity.

Any fundamental reason for the sharp correction?

Disc: Tracking

the reason for derating could be due to coal india which is one of their prime clients is developing their own portal for eauctions

1 Like

I think coal India has decided to come back to external agencies instead of their own portal. I am not sure is it temporary or permanent strategy. Recently MSTC got work award for 2 years from coal India.

mstc coal India.pdf (638.6 KB)

From q3 call:

Discl; invested 5% of PF.

6 Likes

Started combing through the PSU rubble to find if a proverbial baby or two were thrown out with the bathwater and stumbled upon this.

Prof. Bakshi’s article is a great pitch however this doesn’t seem to have the most desirable of network effects since it seems to lack fragmentation of bidders and suppliers.

Not sure how much incremental trust is required/brought to the table by MSTC since the supply(and demand to an extent) seems to be concentrated and from trusted entities for most verticals.

This has naturally manifested in suppliers using their own platforms/presence of strong competition in general

Management lethargy in the midst of all this is worrying too.

Can’t seem to find any updates on the datacenter/fintech changes in the articles of association. It has been over a year and I was hoping for a financing platform integration into the auction for buyers and sellers to be live by now.

Also, any directive(wrt the scrappage policy directive for govt vehicles) issued by the govt doesn’t seem to be mandatory/legally binding/enforceable in court.

In order to facilitate seamless scrapping of such vehicles, it is proposed that the e-auction

platform developed by Metal Scrap Trade Corporation Limited (MSTC) which is a Mini Ratna

Company-I PSU under the administrative control of Ministry of Steel, be used to conduct e-auction of such vehicles.

Note: Quote from the linked directive, emphasis mine.

So, it seems like MSTC’s prospects hinge on the relationship of each state with the Ministry of Steel and the perhaps the relationship/beef between individual high ranking officials of the State govt and MSTC/Ministry.

All this is my preliminary understanding and I could be massively wrong. Please do correct me.

Disc: interested and researching; might buy anytime; not invested

5 Likes

Is there any way of calculating how much Coal Auction is going to happen in next 2 years, and how much MSTC can make through commission ?

Do we see any potential trigger areas for MSTC ? Coal auctions is a consolation - i.e. we thought its gone out , but it has come back to an extent.. The data center/fintech seems opaque - i.e no details of the plans and what can be projected..

Any triggers you see?

Disclaimer: Invested from 2023.. added later on the up…A small portion of my Portfolio. Trying to find out whether I should hold (any long term expectations) or close out

2 Likes

Another growth trigger of 30-70 crore per annum through EPR credit platform. I just took the market of Plastic EPR and put up a 0.5% fee of the EPR value which should get traded on the platform. Rubber and other commodities would be extra

6 Likes

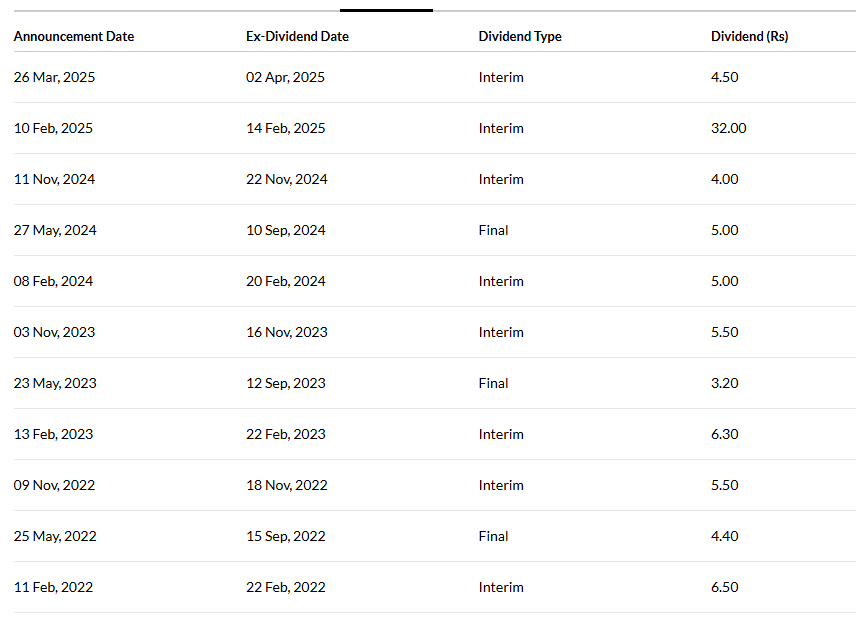

A thought I had looking at the low valuations - at a P/E of 17 and a dividend yield of 7.5%, this might be a stock where you are ‘paid to wait’ for the upside to play out! Please share your thoughts.

Please note that the unusually high optical dividend yield is due to the recent disinvestment of FSNL. Under normal circumstances, the dividend yield is typically around 3–4%.

5 Likes

Thanks for pointing that out.

PS: REC was one such stock where I ‘came for the dividend but stayed back for the capital gains’!

MSTC Ltd nominated by DGFT, Govt. of India to conduct e-auctions for Gold TRQ under Rule 194 of GFR, 2017.

- Service includes online administration of TRQ allocation for gold bullion & other commodities.

- Agreement with a domestic entity, no related party transactions involved.

- Revenue generated from transaction fees paid by bidders per e-tender.

- Management expects a fair volume of business from this initiative.

3 Likes

Hi, hasn’t Prof Sanjay Bakshi’s fund entered around Q3/Q4 2024 and exited earlier this year?

Yes. Looks like that. I have also exited last year.

1 Like

Hi everyone (@Prathamesh_Adhikari, @axsubram, @Pranshinv and others)

Looking for views on MSTC Ltd.

The stock had a strong run in 2024 (almost 2×) and then corrected sharply. Recently, WisdomTree picked up around 0.5%, but the price still drifted lower. Technically, the weekly EMAs (10/30/50/100/200) are still compressed, and the stock has been consolidating around the ₹470–520 zone for months.

Fundamentally, MSTC seems interesting because:

- It’s now India’s authorised EPR trading platform operator,

- EPR + Carbon Credit opportunity is estimated at ₹8–10 lakh crore ecosystem over time,

- The business model is asset-light with high operating leverage.

Questions for the group:

- Why do you think the stock is still weak despite this macro tailwind?

- Is the current consolidation healthy, or does it signal more downside?

- What’s your view on MSTC’s FY25–27 earnings potential from the EPR platform and recycling business?

- For long-term investors, is this a solid accumulation zone or would you wait for stronger confirmation?

Any informed opinions, charts, or industry insights would be really appreciated.

Thanks in advance!

3 Likes

I will try to answer as per the questions you asked

- I think the company is mostly misunderstood, it is a platform business but without any steady transactions which gives very lumpy PAT/EPS

- with limited technical knowledge, yes it looks healthy

- I can tell you about Tyre recycling, the current EPR certificate get traded for 2-3 Rs/Kg, you can multiply that by total India domestic tyre production in tons to get the annual trading volume and may be consider 1-2% commission as revenue

- as retail investor, patience should be our edge, so either we need to wait for the strong earnings visibility and enter or just enter when the stock is valued at zero growth in earnings -which pretty much is the case right now

2 Likes