Do you guys know anything about recent selling?, is it because of this above disinvestment?

There are NOT a lot of positive catalyst going for MSTC in short term from my perspective right now but can list many on the negative side.

- E-commerce: Management has failed to articulate where the growth will come from given the headwinds of Coal India business going away, private sector revenue growth will take time, gestation of new initiatives will take time (e.g. recycling of other electronic items, etc)

- Vehicle scrappage - market was pricing this to happen much sooner than even management was expecting. Mgmt kept on reiterating that this will take time given infrastructure is not set up. Even when it kicks off, this space will be highly competitve both from JV with Mahindra as well as listing of scappage vehicles is concerned

- High growth from the divested FSNL business kept MSTC’s numbers look attractive on a consolidated basis than they were in the last 2 earnings updates.

- You now had a business trading at mid 20s PE, with almost no growth in the near term and no great articulation from management from a vision perspective.

I have attached my write-up from early this year incase helpful

MSTC Limited _Ex…pdf (245.9 KB)

3 Likes

While I’m not a valuation expert, my rough estimates suggest that with a projected PAT of ₹160 crore for FY25 (₹40 crore in Q1), and applying multiples of 10-15 along with cash reserves of ₹1400 crore, the market capitalization would be in the range of ₹3000-₹3800 crore.

The current Mcap is 4800 cr with PE of 22. It might correct some more from these levels (not a expert!). Feedback welcome!

4 Likes

Current vehicle scappage policy is not without flaws…Cars to be Scrapped Based on Pollution Levels Not Age

1 Like

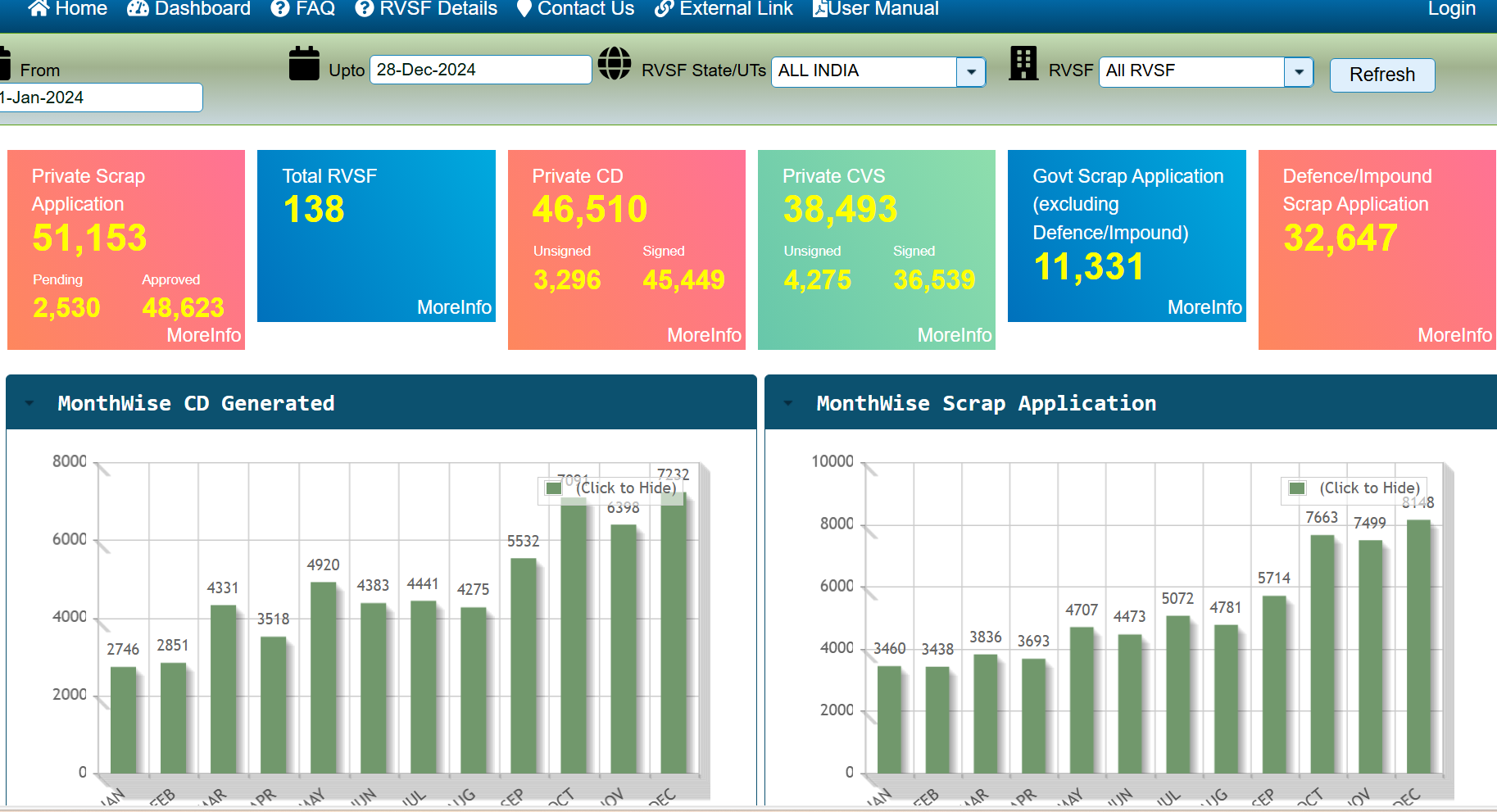

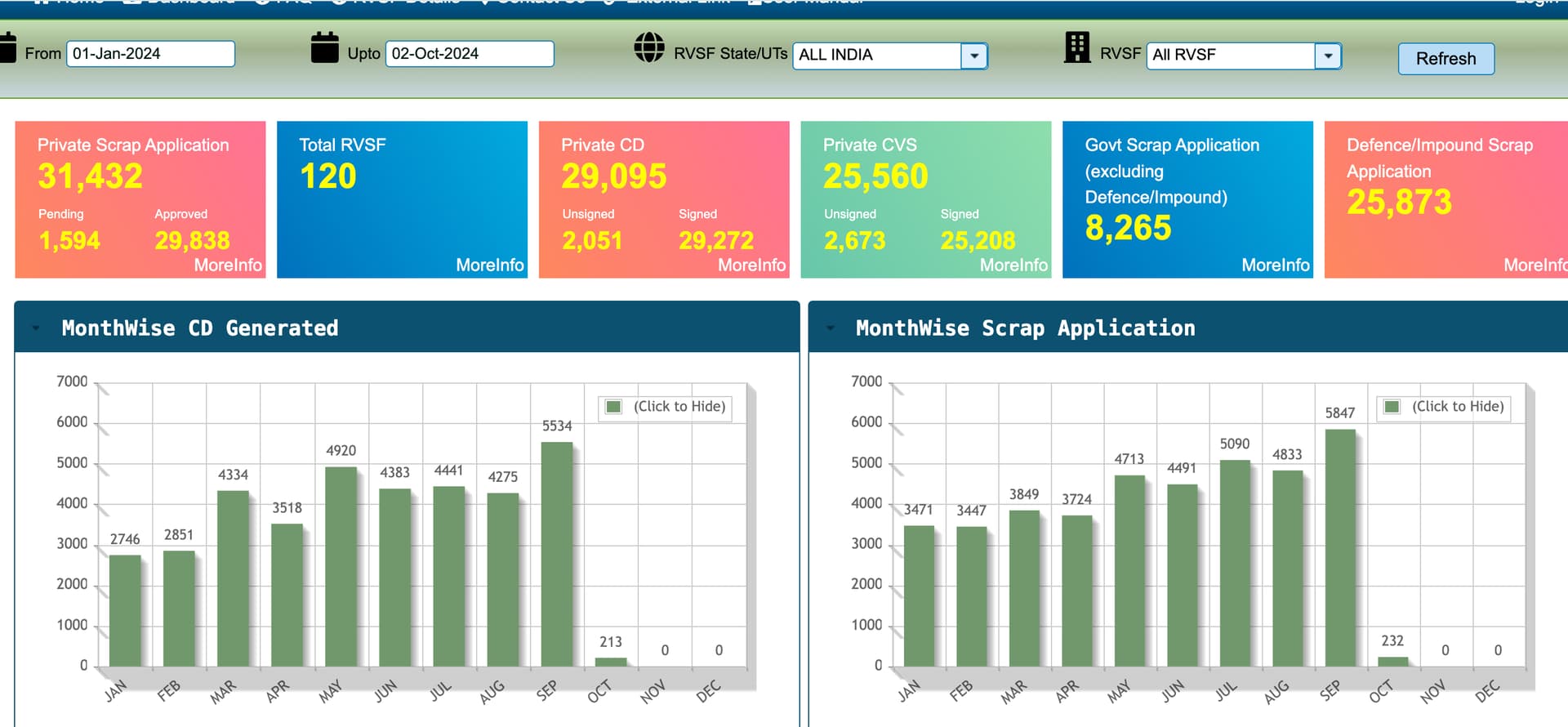

I took out this year`s scrapping data for CY24, forget about MSTC share but the total vehicles which have come for scrapping to all the 120 facilities all India (Certificate of Deposit) is 31K, whereas MSTC would have a share of around 8K so 35%

too low for any meaningful business profit.

1 Like

just see the actual data of vehicles scrapped, it comes to 8K vehicles this year, so your assumption of 0.7M vehicles needs to be revisited

This research is as of March this year when Mgmt expected scrapping of old vehicles to pick up post election. I clearly overestimated this helped by mgmt bullish views after I spoke to them.

Just FYI, the 0.7m is for FY 2026, still probably optimistic number but just incase.

Also, I do not plan to update these numbers until MSTC declines substantially to me margin of safety. If and when I do, happy to share on this forum.

3 Likes

cool, makes sense. I invested into this, around 300-350; that had a great margin of safety

also, I feel the E-commerce business is totally unpredictable, as it is at the mercy of Govt announcing divestification or spectrum sale kind of intiatives, hence a PE of 15, is a little high.

MSTC ideally should be a good PSU bet which is guranted to work over next 5 years and pays a heafty dividend

2 Likes

Mind you, post divestment MSTC margins and return metrics are really attractive. Question is the direction and growth of the company.

Question - Are you still holding? If yes and you think 15x PE is too high, why not sell given where it is trading versus ride it all the way to the bottom?

2 Likes

I did some profit booking at 900-920 region; purely looking at the high PE.

and you are right, FSNL divestment should give a good exceptioanlly high dividend- it is attractive on that basis as of now.

2 Likes

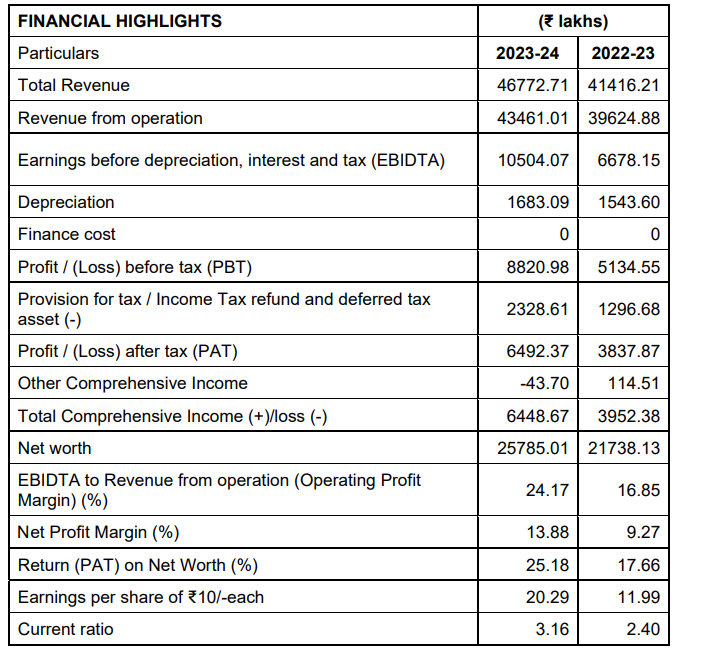

FSNL Highlights

FSNL has a networth of around 257 crores against which MSTC has realized Rs.320 crores.

Realization was assumed on higher side seeing the growth in last 3-4 quarters.

2. Coal India has started itz own platform as they are aware of their major customers. Major clients of MSTC seems to scrap dealers and PSU which is allowing them to fetch 40% of revenue. To have huge numbers of scrap dealers at various locations in India for online auctions seems to be MOAT for MSTC which i believe.

3. Vehicle Scrappage Policy is taking his own time to get implemented but it will be implemented in next 2-3 years .Till that time if MSTC is able to cater Government vehicles all over India, it should also reasonable topline to MSTC. On monthly basis the numbers are increase of vehicle scrappage.

4. Extract from transcript “So that is the organic growth of, finding more clients or finding more entities, who are into e-commerce of the kind of things that we already are doing. And apart from this, we have also been working at integrating services. So that is a separate line of business, which would be a somewhat inorganic growth, which would build upon what we are doing and are developing more upstream or downstream activities. So that’s two ways that one thinks of growing, which is what MSTC has also been.”

“It should start happening. The revenue stream should start happening from new initiatives in Q3 I mean, things that we are working on at this point of time, So Q3,Q4 onwards, there should be significant.” (extract of Transcript June 24)

“We have also embarked on a very ambitious plan for building and enhancing capacity in terms of domain expertise, both in terms of manpower and in technology. We are quite confident that this approach shall show tangible results, tangible benefits, in Q3, Q4 of FY 25.” (extract of Transcript March 24)

As per the commentary of Management ,Q3 /Q4 should be the period where some new business should materialize and sale of FSNL in Q2 seems to be that direction. It enables to have cash in the books for future opportunities.

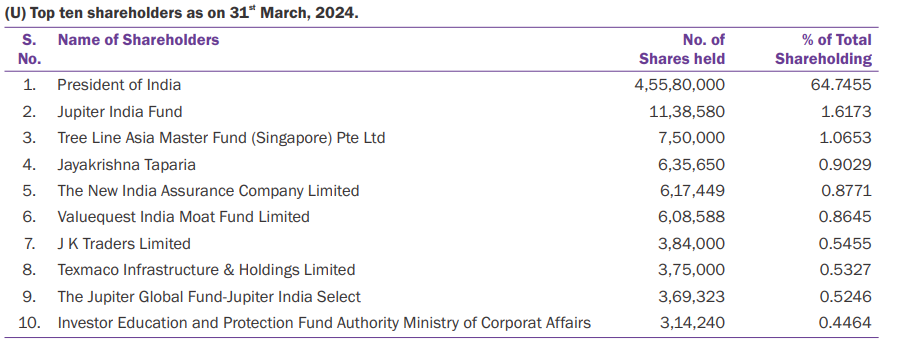

New India Assurance Limited seems to selling spree in last many quarters and major sell off in last quarter may be from his end. Shareholding patters for Sept 24 will be key to watch.

Another Selling shareholder is Quant Mutual Fund in Aug 24 month which has been acquired in June 2024.

“I am just Eagerly waiting for Walk the Talk by CMD…”

6 Likes

Thanks mate. I had started building quantity & sold it. Twice. As both the times, I wasn’t sure of value, as growth is lumpy & the stock had run up much ahead of fundamentals was what I thought. Also, the second time Coal India business went away. Not sure if we can model this business with much confidence even though it has come down significantly. Because we can’t forecast EPS over the next 2-3 years with much confidence, it becomes useless to look at TTM PE. No doubt the opportunity is huge but even the competition is coming quicker & exponentially. Management talks on too many things too vaguely. Sometimes they talk about inorganic growth without much clarity, sometimes they talk about datacentre business without any focus. A platform business, e-commerce, great balance sheet, cash rich. But how to look at future growth is the question & depending on that how to value?

3 Likes

Hi All,

Finally built a sizeable position in MSTC today. With the decent moat, optionality due to huge cash, 0 debt, it’s a quality franchise. Even though not too cheap, available at a reasonable valuation (may be because of the government stamp). Bought it with the timeframe of 5+ years. Hope to see management showing us what we envision this business could accomplish.

Disc: Invested, biased.

Hi Akshay,

What are the opportunities we see for MSTC to grow from here?

Just Govt sell-side ecommerce - MSTC seems to be charging very small amounts - What can we factor/project?

Vehicle scrapping - Seems to be taking sweet time (Further other players like Tata motors are also in the market I guess).

New initiatives - Is there a clarity on what the new initiatives are ?

Anything else?

Pl share the info/factors if possible . Will be very helpful

Disc: holding - decent portion of pf and evaluating whether to hold or get-out.

Hi Anand,

MSTC annoys us no doubt. As I mentioned above, I myself had built a small position & sold, twice. Nothing’s changed but I have committed myself to this story as I think long term story is still beautiful. If you have found a better opportunity, no harm in moving out. I might do the same in the future. As of now, I think I am going to stay with MSTC at least for the next 5 years.

My rationale as of now (Because I have a history of not staying with MSTC):

- I had cash & MSTC at the current valuation, seemed much better than most of the other opportunities outside of what I am holding. Pretax earnings yield of ~8% + 2.5% starting div yield. 0 debt, doesn’t need much working capital to grow, negative cash conversion cycle, very high return ratios, decent moat, platform businesses have inherent scaling. What’s lacking right now is a laser sharp focus from the management & fire in the belly of the management.

- Very low charging on the GMV is an edge & creates barrier to entry.

- I anticipate that the stock may not perform upto my expectations for the next 1-2 years & I am OK with that. Rather the stock may decline from here by 10-20 odd percentage & I am also OK witht that.

- I think the recycling side of things should get sorted over the next 2-3 years. I am here to hold for at least 5 years unless there is a big negative event or I spot some other better opportunity.

- The extra cash in the business may get distributed which will even lower my purchase price.

- Low working capital requirements may mean growing dividends for a growing business over a very long period.

- This business has a potential to give BEL like returns over long term (5 years+. The story might be a multi decade story).

Of course, I could be wrong & might sell tomorrow but the business seems a quality business, available at a reasonable valuation, decent moat, big & ever growing TAM, optionality due to cash.

5 Likes

Thanks @AkshayBharde for sharing your thoughts.

Could you perhaps list down the anticipated growth triggers and unexpected negative triggers?

ps - I am currently studying the business and trying to build conviction. thanks!

●

Key Highlights of Q2 FY '25:

○

Sale of FSNL (100% subsidiary of MSTC): The transfer is expected to close within 60 business days from October 24th, 2024 when the SPA was signed.

○

Operational Performance: MSTC exceeded INR 476.16 billion in transaction value through its e-commerce and marketing verticals during H1 '24-'25.

○

Financial Performance:

■

Standalone PBT: INR 111.50 crores in H1 '24-'25 compared to INR 158.99 crores in H1 '23-'24.

■

Standalone PAT: INR 83.48 crores in H1 '24-'25 compared to INR 113.08 crores in H1 '23-'24.

■

Consolidated PBT: INR 108.72 crores in H1 '24-'25 compared to INR 136.40 crores in H1 '23-'24.

■

Consolidated PAT: INR 118.29 crores in H1 '24-'25 compared to INR 105.95 crores in H1 '23-'24.

●

Key Projects:

○

Ongoing:

■

Spectrum Auctions: Managing the e-bidding portal.

■

Coal Block Auctions: Ongoing with various tranches completed.

■

Mines and Mineral Block Auctions: Being conducted in various states.

■

Exim Platform: Actively used by Indian Oil and ONGC Group of Companies.

■

Deep Portal: Stable portal used by DISCOMs for PPUs.

○

Upcoming:

■

FM Width Radio Wavelength Allocation: Expected in Q4 FY '25.

■

Digitization of KPKB Retail Operations: Likely to start by the end of the year.

■

E-auction of Timber from Chhattisgarh Forest Department: Auctions expected to start in Q3 FY '25.

■

Listing Portal for NPA Properties (non-PSB): Ready and operational soon.

■

Infrastructure as a Service: Modules developed for clients to be offered as infrastructure, targeting sectors like recycling, mining, and e-commerce.

■

ERP for Mineral Sector: Software for pre- and post-auction activities integrated with client databases.

■

Scrap Sale Agreement with BPCL: Exclusive contract to handle scrap sales for BPCL’s marketing division.

●

Financial Performance Discussion:

○

Standalone: The decrease in revenue is primarily attributed to a decline in e-commerce revenue, particularly e-auction and e-sale.

○

Consolidated: The improved performance is attributed to FSNL’s performance, which is now categorized as a discontinued operation due to its upcoming sale.

○

Other Income: Reduced due to non-receipt of dividends from FSNL in H1 '24-'25.

●

Q&A Session:

○

Competition from GeM Portal:

■

GeM’s mandate for government procurements has impacted MSTC’s e-procurement earnings.

■

MSTC differentiates itself by offering customized solutions and end-to-end services for high-value items and specialized procurement needs, particularly in scrap auctions.

■

MSTC believes GeM’s standardized model may not cater to all requirements.

○

Utilization of FSNL Sale Proceeds:

■

The sale is expected to close around January 15th, 2025.

■

Utilization plans will be determined after the sale’s completion, considering factors like advanced tax payments to the government.

■

Decisions will be made through internal management and board meetings, and will be communicated publicly.

○

BPCL Contract:

■

Exclusive contract for scrap sales from BPCL’s marketing division.

■

Expected scrap value of approximately INR 100 crores per annum.

■

Revenues will be generated on successful sales, and are expected to materialize from Q4 FY '25 onwards.

○

Listing Portal for NPA Properties:

■

Targeting private, rural, and cooperative banks that lack a standardized NPA disclosure system.

■

MSTC will provide an integrated listing and bidding platform, aiming to create a market for these NPAs.

■

Competition exists from PSB Alliance’s portal, but MSTC believes its platform offers superior transparency and competence.

■

Currently, these banks primarily manage NPA sales through informal methods such as phone quotations and limited client outreach.

○

Future Growth Plans:

■

Focus on expanding into new areas like infrastructure as a service, data centers, and ERP for the mineral sector.

■

Targeting clients who require customized solutions and value MSTC’s expertise and experience.

■

Revenue generation from these new ventures is expected to take a few quarters to materialize.

○

Infrastructure as a Service:

■

Offering scalable, cloud-ready hardware on a plug-and-play basis to meet IT requirements.

■

Targeting small and medium-sized organizations, including government departments, MSMEs, and micro companies, who lack resources for private cloud services.

■

Leveraging MSTC’s existing relationships and reputation to provide a cost-effective and secure solution.

■

Offering services like virtual data rooms, with plans to potentially develop a large data center in the future.

○

ERP for Mineral Sector:

■

Providing a comprehensive software solution for pre- and post-auction activities, including mining, delivery, and integration with client databases.

■

Building upon experience gained from mineral block auctions and targeting state-owned mining companies.

■

Offering a customized software solution with various revenue models, potentially hosted on MSTC’s infrastructure.

4 Likes