Thanks a lot for this insight really feels like company management walks the talk.

2 Likes

Hi Shreya,

The company is expanding in ever manner be it distribution, product profile, manufacturing sites, geographies etc. And considering today’s situation company has a huge runway ahead because of very low market share as compared to leaders, but due to aggressively expanding and also premium brand vis-a-vis good brand recall it is gaining market share.

7 Likes

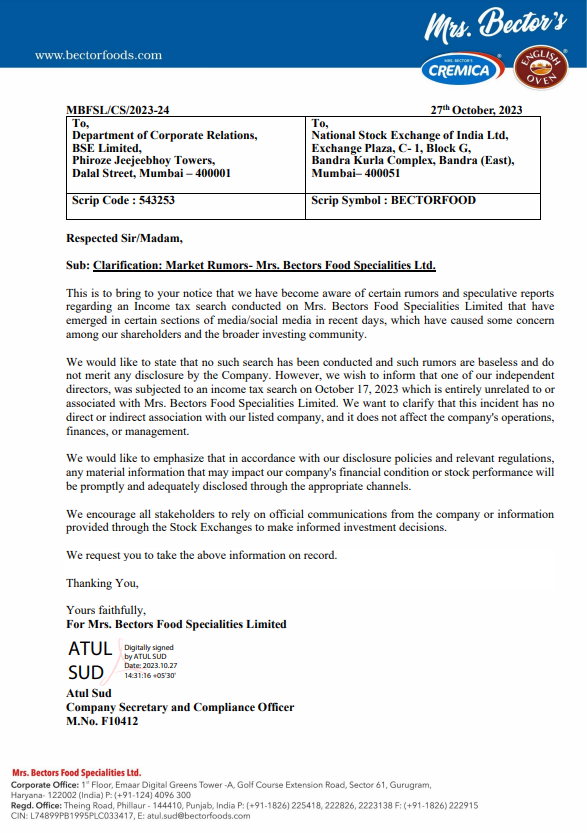

Came across this news - Income Tax: I-t Raid On City’s Leading Business Groups Ends | Ludhiana News - Times of India (indiatimes.com)

Does anyone have additional information regarding this?

1 Like

Interesting developments under co; I have been tracking the company since day 1 of the IPO listing, invested, and exited with decent profits earlier, but I never stopped the habit of tracking this company. With the recent developments at co, expansion, distribution and the promising promoter group, it looks very interesting opportunity again now & so, finally I resized the allocation at 1100 levels.

1 Like

Small scuttlebutt for English Oven bread last weekend-

Went to 2 Reliance grocery stores in Dehradun and found out that both Reliance fresh and Reliance smart Point only keep English Oven as their primary bread.

No Bonn, No Ellora and No Britannia.

Asked the store managers of both the stores and found out that restocking of breads happens every other day with almost no expiry.

I went ahead and bought a couple to breads to see for myself and not gonna lie, it was pretty damn good.

Disc- Invested around current levels.

16 Likes

Thanks for sharing such valuable information!

1 Like

Bectors Foods scuttlebutt #2, This time for Cremica-

Yesterday, I went to 17 local grocery stores and 4 large grocery stores in Dehradun- Prerna, Bachat, Suvidha and Reliance.

For local grocery stores, only 3 out of 17 stores kept Cremica biscuits. Upon asking the reason, almost every shopowner said that customers wants “brand” and their highest sales Brit and Parle are about 95%. Cremica maybe 2-3%.

But this was not the case with larger grocery stores. Apart from Suvidha, all 3 stores kept Cremica and post talking to managers, got the same feedback that people do consume the brand but it is limited.

In large stores, they did gave “Buy 1-Get 1” for family/value packs biscuits and cookies.

Also, surprisingly found their premium cookies with local chaiwalas also.

The most standout thing with Cremica biscuts in general is their matt finish packaging which does give a lux feel.

And in the end, as always, I ended up buying 2 cookies and 1 biscuit and I can guarantee you this, once the wrapper is removed, you cannot spot the difference between Britannia and Cremica.

PS.- Avg shelf life of Cremica products is broadly 1-2 months for larger retail stores and 2-3 months for smaller retail stores.

18 Likes

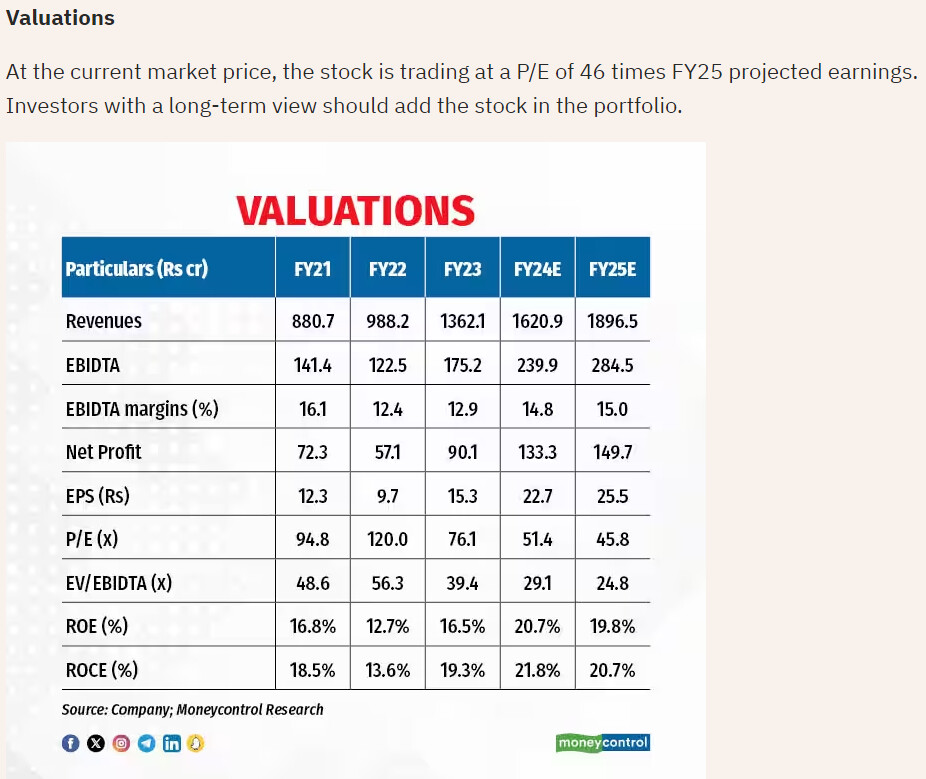

Thanks sir for your beautiful insights. I am tracking this counter and in my personal opinion the products are at par with other fmcg majors such as britannia, itc etc however what i want to ask about is valuation, is the current valuation justified?

Britannia has decades of presence and a good brand to show for itself hence it commands a PE of 50 however cremica is much newer and still commands similar PE to britannia despite the fact that britannia has a well established B2C business while cremica has just started building it and has a long way to go. Your thoughts on this plz. Also what according to you would be a right entry point in this stock if one has a horizon of at least 5 years?

I don’t think it is as simple as that. 5 years can be considered as long time too. A lot can happen in both the business of a company, and with us too. After 2 years, you may not want to hold the stock for any reason.

Valuation while expensive today, which is again subjective, might not be the same as the company grows, and if the company indeed grows, the price does not fall much, it may in fact move up absolutely or relatively. One way to gauge this is to look at demand. Not that this gauging is perfect or it can be done quickly, but we will have some idea of looking at the valuation from the point of view of participants, if we follow the price. So if a business is growing, and can grow, price can go up for continuously.

The opposite is also true, if indeed the future growth of the foreseeable future is reflected in the current price, then the price may fall some, but there could be time correction.

So one can have a position, follow the business, take actions in accordance with price/demand/market.

Not invested in Bectors, following the thread, have a position in Britannia.

1 Like

I understand that, I had always been interested in Titan and wanted to add it in my portfolio but i never got the opportunity to add it as it always seemed little expensive and never fell considerably. Though from a completely different industry i think cremica too is showing similar signs…not falling much and growing well.

2 Likes

@rochakjain02 , Thanks for sharing such a detailed on ground checks, i also found one thing that small retailer started giving shelf space to cremica with one or two biscuits varient but supermarkets having all varities and supermarket ranging from reliance smart point to other local as well.

3 Likes

Hi @ConsistentLearners Quick question bro, which city and store is this?

hi, this is from Delhi in my nearby store.

1 Like

Bectors reports Q3 2024 earnings

Net Profit up 23.6% at ₹35 cr Vs ₹28 cr (YoY)

Revenue up 17% at ₹429 cr Vs ₹368 cr (YoY)

EBITDA up 20% at ₹61 cr Vs ₹51 cr (YoY)

Margin at 14.2% Vs 14% (YoY)

4 Likes

Compared to other FMCG companies, the results aren’t bad QoQ at revenue level.

The reason for decline in profit needs to be seen as I am assuming raw material inflation should not be a factor. Yet to see press release.

I think the strong market reaction could also be due to the very sharp run-up this stock has seen over the last 10 months.

Interesting to know the Management commentary on margins going forward, how well they are managing the distributor expansion and contribution from overseas operations (Walmart, UAE etc) going forward.

Disclosure: Invested at 1,000 level. Keenly following this stock to add more once the Management commentary is out.

5 Likes

Higher mateircal cost leading to lower OPM from 16% to 14% is spooking the market. but i think thats overreaction.

2 Likes