@Lynch,

Very valid points. The only thing I would like to add is that 60 P/E on TTM is not on normalized margins and I think it is possible to do 14% kind of margins on normalized basis given their GM will be in 45% range. Thus 100-120 Cr PAT range is expected so it is 30-35 times FY 24. However, this too is fairly priced in my view

Discl: Invested with decent allocation

9 Likes

Have been tracking and adding this. I think the Company has really just got started on expansion over the last 2-3 years and there is a lot of headroom for growth. A PE of 60x on TTM basis for a good FMCG company is not a stretch in my view. Just as an aside, personally I like their products too :).

2 Likes

rather than PE i would value this on sale/mcap like other fmcg value as long as co is growing its margin and reaches to 14-15% opm.

most of fmcg are trading at 6-9 mcap/sales value where as MBF is trading at 3x mcap/sales while MBF has lower opm. At current opm and growth situation I would see MBF fairly valued at 4x mcap/sales

4 Likes

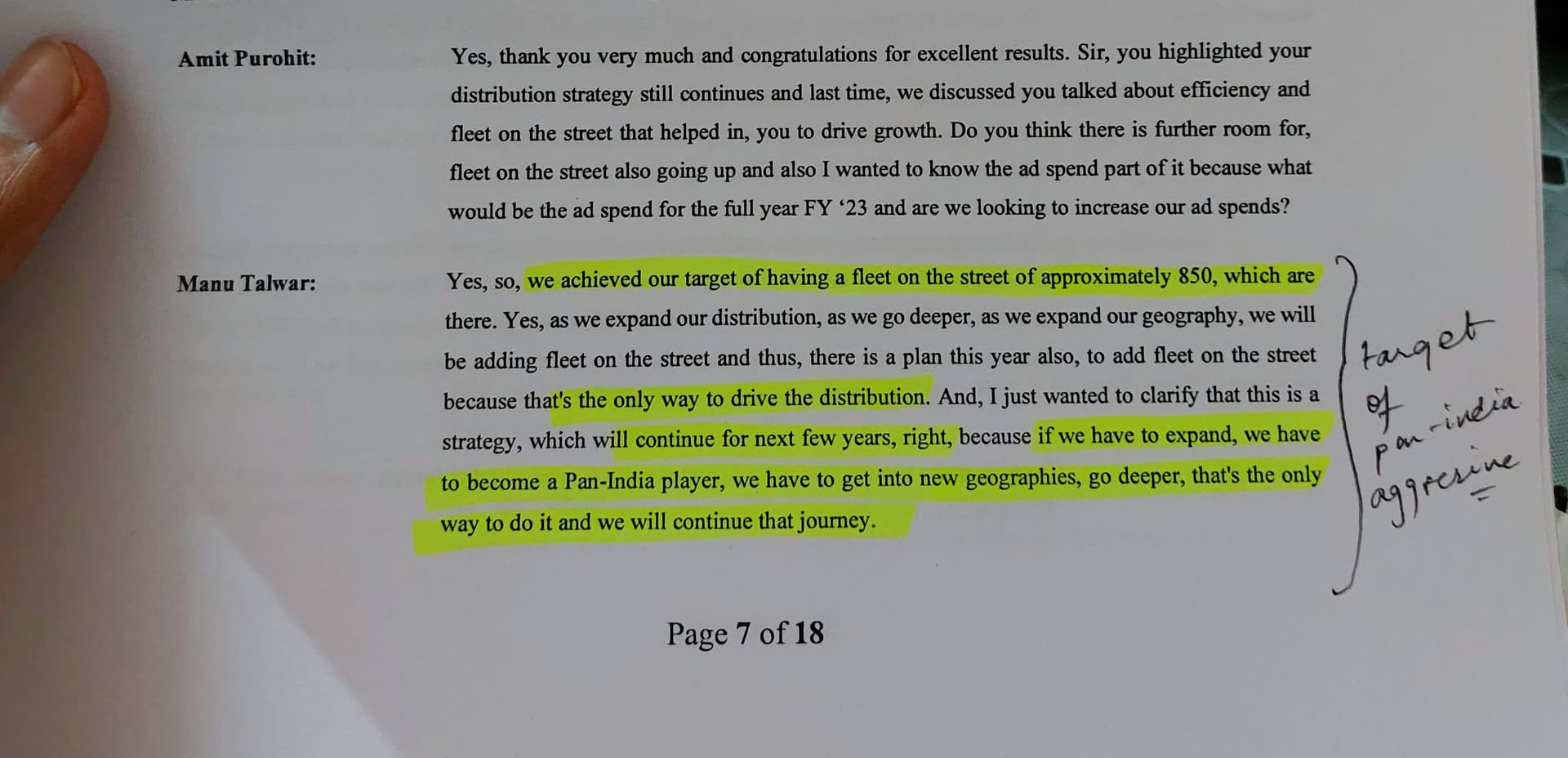

Mrs Bector Q4FY23 Concall Summary

2 Likes

Valuation at 50 P/E shouldn’t be such a big concern for the small cap consumer company which is expected to grow volumes in high teens (17%-19%). Some strong pointers for FY 23-24:

- Valuation at less than 30 Price to cash flow from operations

- Strong working capital cycle with ability to convert cash in less than 40 days

- Potential to grow revenues at 25-35% (Company itself indicated reaching 2400-2500 crores in next 2 years)

- Expansion in south and west is going to play a significant role, so lot of headroom for growth.

- Company’s stock price is in stage 2 and hence indicates strong buying momentum.

Disc: Planning to invest in the business.

13 Likes

Penning down aftermath of exiting bector. I averaged bector at around 290rs buy price and bector performed very well and is close to 900 now. I exited bector between 750-850 and while I try to reason this with good opportunities available in Pharma and chemicals, some parts in banking sector and IT, all the while bector valuation continuing to increase , I feel it was a wrong decision with very long term view. While it’s selling at premium, I have seen some companies like Varun beverages, polycab justifying their premium and providing solid growth and while one can do discounted cash flow, sometimes , the effect of improving margin and sales growth and product portfolio expansion can have great effect on a company which no one can predict, especially if it can sustain for even 2-3 years of company life. If fund houses upgrade valuation on these grounds, people can sit on mouthwatering profits and understand true meaning of compounding. While there’s such a possibility in bector and I may be missing it having no plans to reenter, hoping this message serves relieving dilemma amongst existing investors and serves me as a decision to critique sometime in the future.

Disc : Completely exited.

12 Likes

I think having some knowledge of charts help, if one assumes that the fundamental aspects of the business reflect in the price, and as such, charts present what the price is doing, consolidating after a good run up, or is there some selling, or decent profit booking is happening with considerable volume, are there any patterns forming etc etc.

An investor who understands fundamentals and is also aware of technicals may want to stay without selling completely, or reduce position, if he believes the valuations are not sustainable.

If one understands a business more, a company can become a truly long term investment, and as such, one can sit through months and months of consolidation, because there isn’t much selling happening, and many are sitting on their positions, so to speak.

One can even look at the fresh purchases being made at such an elevated price levels.

And we have such technofunda practitioners here in VP, not necessarily with a long term view, but who understand the business and take appropriate entries and exits based on charts.

I have some elementary understanding and I am learning, and I am getting benefited by this approach.

Not invested in Bectors but have been in a similar position of booking early profits without knowing that a fall or the selling isn’t big, and that I can check a few more things to come to the decision of selling completely.

7 Likes

Great to see your honesty. May be you can start looking at v-stops in technicals, they seem to work more often than not. A good funda-techno combination could help you not exit stocks just because they have gone to a higher valuation.

1 Like

Of course, exit plan also depends on the objective of the investment. My reply was in general, and depending upon the objective, risk appetite, time, one can wait and see what happens too, if one feels that the price may go even higher, and is reluctant to sell.

If selling is tough for seasoned investors, it sure is for me.

1 Like

Yes. I have been stickler of 3 approaches so far.

- Opportunity cost : Value investing approach.

- Peter Lynch quote : If you’re going to sell it if it goes down by 10%, you should sell it today. This is again based on value approach.

- Periodic rebalancing. But again based on above two principles.

Otherwise I would mostly keep them untouched. But yea, I should probably look at some technicals and maybe as basic as momentum score offered by many websites or explore V-Stops mentioned by you. Will try to keep that in mind. Thanks for your input guys @Vinay_Garg @ChaitanyaC

1 Like

Hi all,

Bectors Food management is bullish for their presence as a pan India company.

2 Likes

I am holding and also trying to accumulate more as my conviction increases.

1 Like

I believe company is good and follow cookie cutter model. They can replicate established model of production and distribution to many cities. After last quarter result stock price popped up and stays at around same price. It happens, when company report good numbers but stock price do not react to earning to fill valuation gap. It happens to me in Syrma SGS Technologies. Two quarters good numbers but stock price stay at same. However which 3rd result it just blast. We need to be patience with these types of good, high growth, small companies where growth highway is big.

Disclosure: Invested in both companies and holding

9 Likes

Thanks a lot for sharing such great insights, I also feel the same company recording good nos., and also seen in the perspective of 2 years from IPO till today it also gained market share in all segments, and also their is a synergistic effect going on of Increasing advt. spends and doubling distribution.

3 Likes

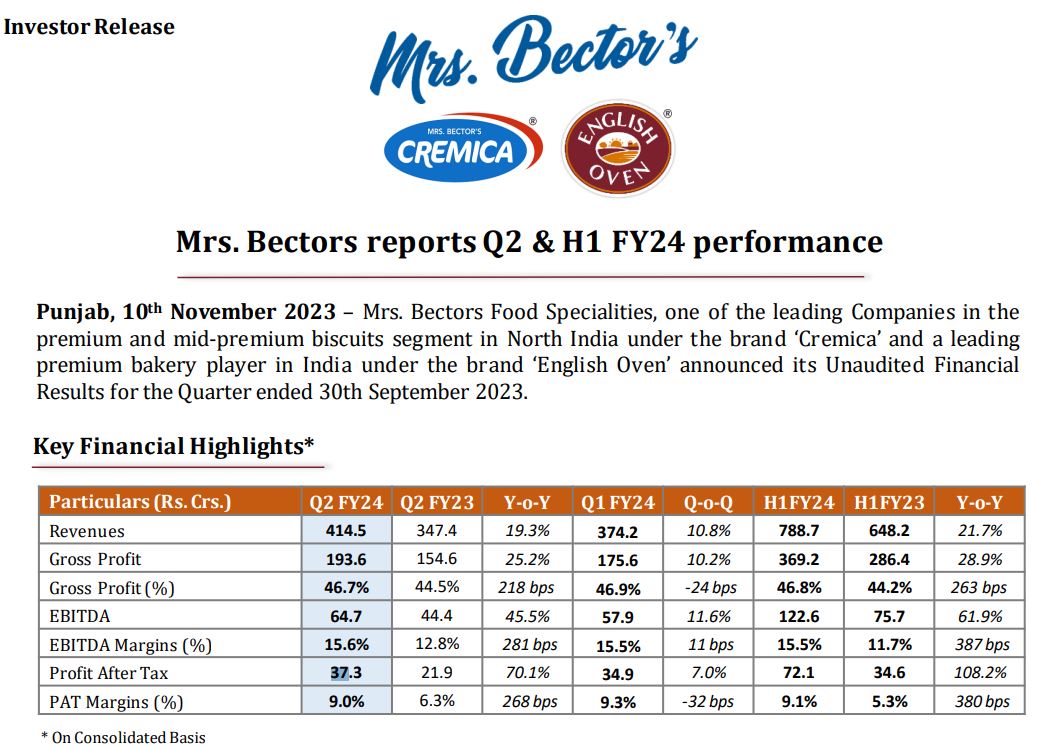

Mrs Bector foods Q2FY24 numbers-

Revenue +10.8% QoQ/ 19.3% YoY

EBITDA +11.6% QoQ/ 45.5% YoY

EBITDA margins 15.6% vs 15.5% QoQ & 15.6% vs 12.8% YoY.

PAT +7% QoQ/ +70% YoY.

Segment growth-

Biscuits +25% YoY stands at 259cr

Bakery +12% YoY stands at 140cr

6 Likes

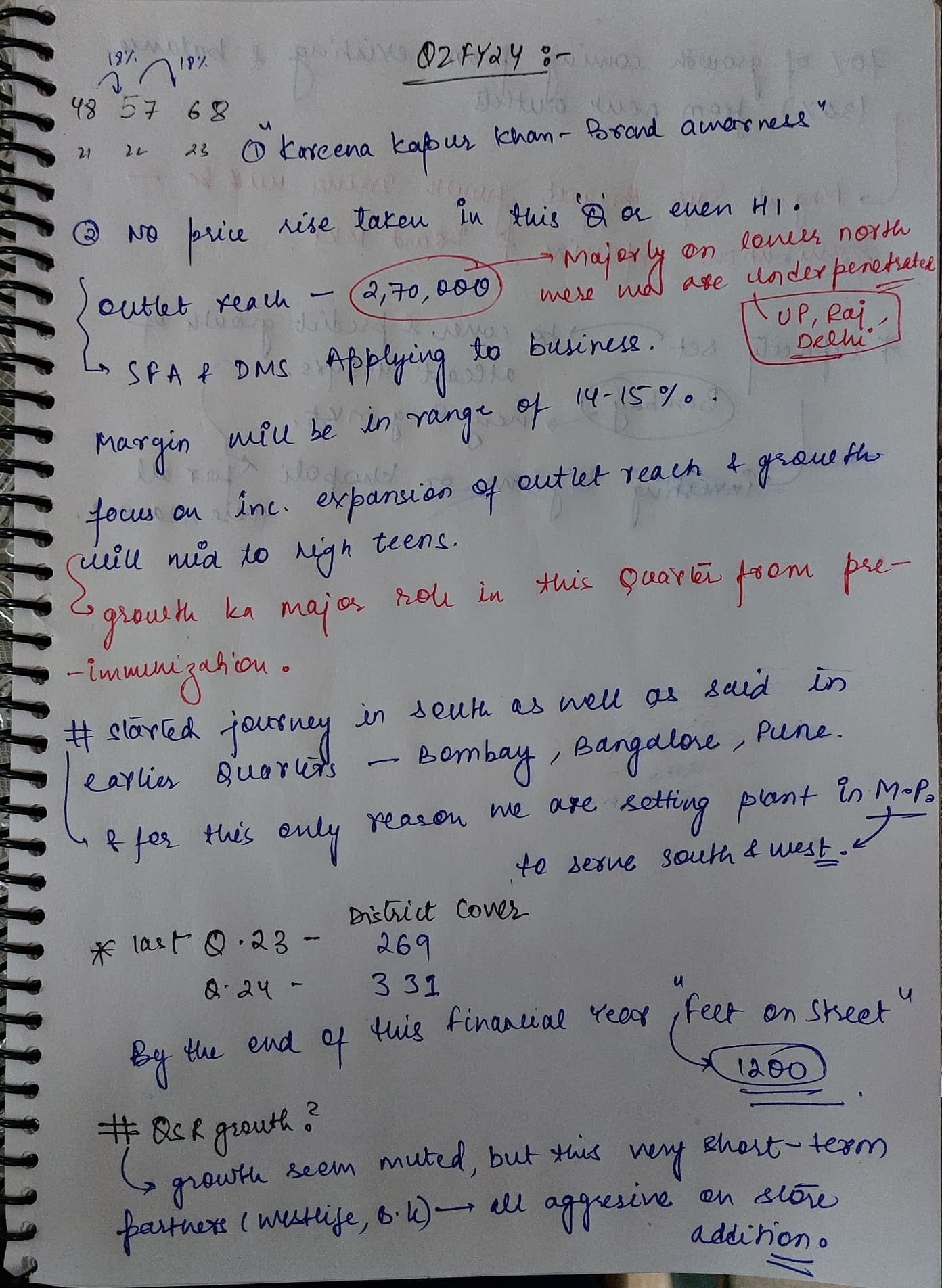

Mrs Bectors Q2FY24 Concall Summary

2 Likes

Hi all,

Operating Leverage for bector’s food will kick in some time but they are really investing and focused to be giant. Here is highlight from Q2FY24 concall , the most important thing the growth comes in this quarter the 70% of it is from existing outlet guess when the new outlet starts kick in .

14 Likes

Source - Official Linkedin Channel

Our sourcing strategy is to have the right product at the right price and make sure they are sourced in a trusted way,” said Andrea Albright, executive VP, sourcing at Walmart, as she spoke about Walmart’s vision of sourcing $10billion worth of goods from India annually by 2027.

Anoop Bector, MD, Mrs Bectors Food added, “Walmart’s utmost confidence in the capabilities of Mrs Bectors is always giving us a morale boost to take this association to new heights. We are not just transnational vendors to Walmart, but strategic partners who are working together to achieve a common goal. From humble beginnings almost 45 years ago to becoming one of the largest CPG exporters from India, we hope to inspire the manufacturing ecosystem in India, especially encouraging everyone to take measures to become a socially conscious manufacturer and of course Women entrepreneurship. We are taking additional measures in developing capabilities both in home and in the USA to be able to deliver the right product at the right time, at the right cost to Walmart."

8 Likes

the company products started available here in UAE in small supermarket earlier this product was available only in big size supermarkets which are located in the MALLS to taste the product i could not find it in super markets so i went to big mall and find this product i recentley noticed in small supermarket and i got surprised the company is agression mode to increase the retail outlets the cremica biscuits displayed next to Britania and itc products price is cheaper comapare to other big brand just want to share the information

11 Likes