Mrs Bectors Food Specialities Limited is one of the leading companies in the premium and mid premium biscuits segment in North India and a leading premium bakery player in India.The Company is the sole preferred supplier to some of the Largest QSR Franchises, Cloud Kitchens and Multiplexes in India The Company has a diversified product portfolio of 480 SKUs and constant focus on new launches. The Company has a strong multi channel distribution network PAN India. The Company is expanding

through modern trade and e commerce. The Company is a leading biscuits exporter to 64 countries across 6 continents.

Mrs Bectors Food Specialties Ltd (BFS; CMP: Rs 280; Market Capitalization: Rs 1,655 Cr. crore)

Highlights

-North Indian player in the premium biscuits and bakery market with 4.5 percent market share

-Higher capacity utilization to support margins

-Higher gross margins as compared to peers due to 100 percent in-house manufacturing

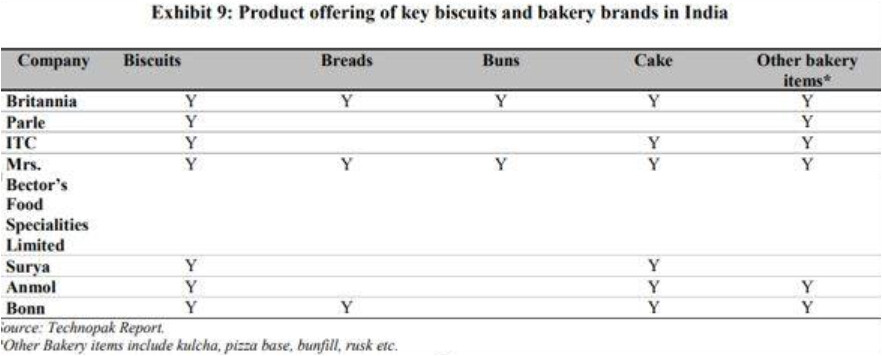

The company is engaged in manufacturing and selling biscuits and bakery products. While the biscuit category is sold under the brand name of “Cremica”, for bakery products, the company uses the brand “English oven”. Bectors Foods specializes in the premium and mid-premium category and caters principally to the market of north India. In the biscuit market it commands 4.5 percent (in FY20) market share while in the branded bread segment, it is 5 percent.

Higher capacity utilization to support volume growth

From 2017 till September 2020, Bectors has invested nearly Rs 260 crore in setting up facilities for manufacturing biscuits and bakery products. As on September 2020, capacity utilization stood at around 72 percent, which leaves room for increasing production. New capacity is likely to come on-stream at the Rajpura facility from April 2022.

Bectors is also likely to invest Rs 100 crore from internal accruals to set up another plant in Dhar, Madhya Pradesh, which will come on-stream from April 2024. The company plans to target newer markets and more retail touch points along with higher presence in the modern trade segment. Higher capacity utilization will eventually add to volumes growth and result in benefits of higher operating leverage.

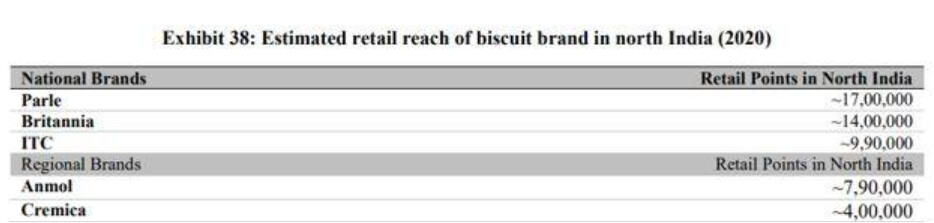

As is apparent from the table given below, Bectors can still target nearly 4 lakh newer outlets which its nearest competitor is currently targeting.

Source: DRHP

Export market to support growth and de-risk business

In the first half of FY21, export of biscuits grew by 39 percent, a much improved performance compared to previous years. Bectors currently exports to nearly 64 countries and in recent times has started exporting to developed markets like Europe, US, Australia and others. After facing some issues with receivables in African countries, Bectors has started focusing on developed countries. With higher export revenues, Bectors is in a position to de-risk its business model, in case of a severe downturn in domestic consumption, especially in the premium category.

Total market size of mid-premium and premium biscuits is Rs 321 billion, which has grown at a CAGR of 12.2 percent in the past five years. The category has grown much faster than the mass category. The market for mid-premium and premium biscuits is expected to grow to Rs 504 billion by FY2025 at a CAGR of 9.5 percent, according to Technopack, which is faster than the overall branded biscuit market growth of 9.2 percent.

North India accounts for 25 percent of the total mid-premium and premium biscuit market. In FY2020, Parle, Britannia and ITC had a combined market share of 57 percent in the premium and mid-premium biscuits market of north India , with Bectors’ share at 4.5 percent. expect Bectors to improve its market share thanks to its higher product offering and capacity utilization along with expansion in retail touch points.

Close to 17percent of Bectors’ sale goes to institutions including the QSR (quick service restaurant) segment, and we expect this segment to add to growth as QSR as a category is expected to do well.

In FY20, Bectors had provided Rs 7 crore as bad and doubtful debts due to the elongated receivable cycle in the African region. Without this provision, margin would have been 13 percent. Because of the company’s relatively newer facility, and lower capacity utilization, return on equity is much lower compared to larger peers.

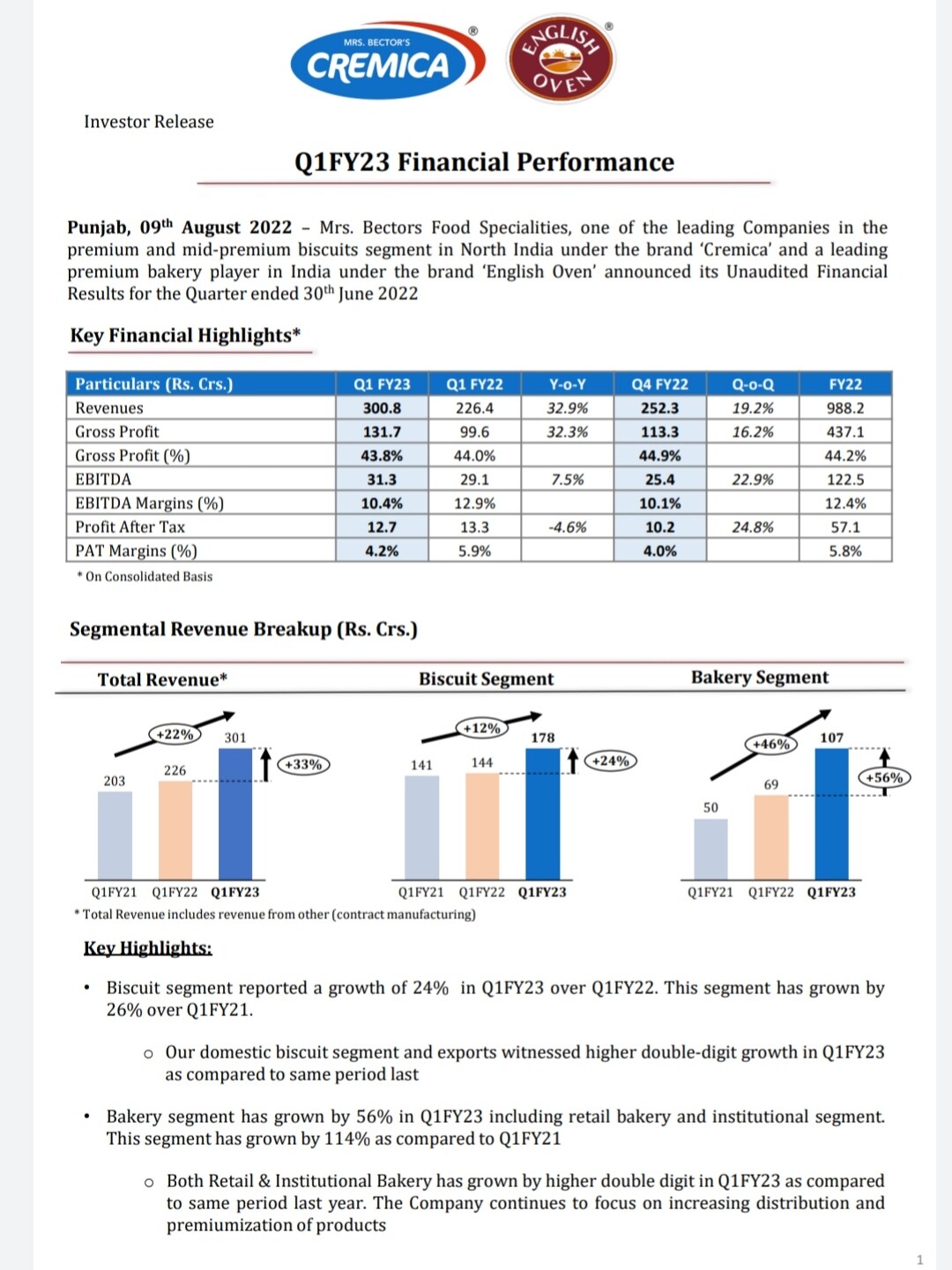

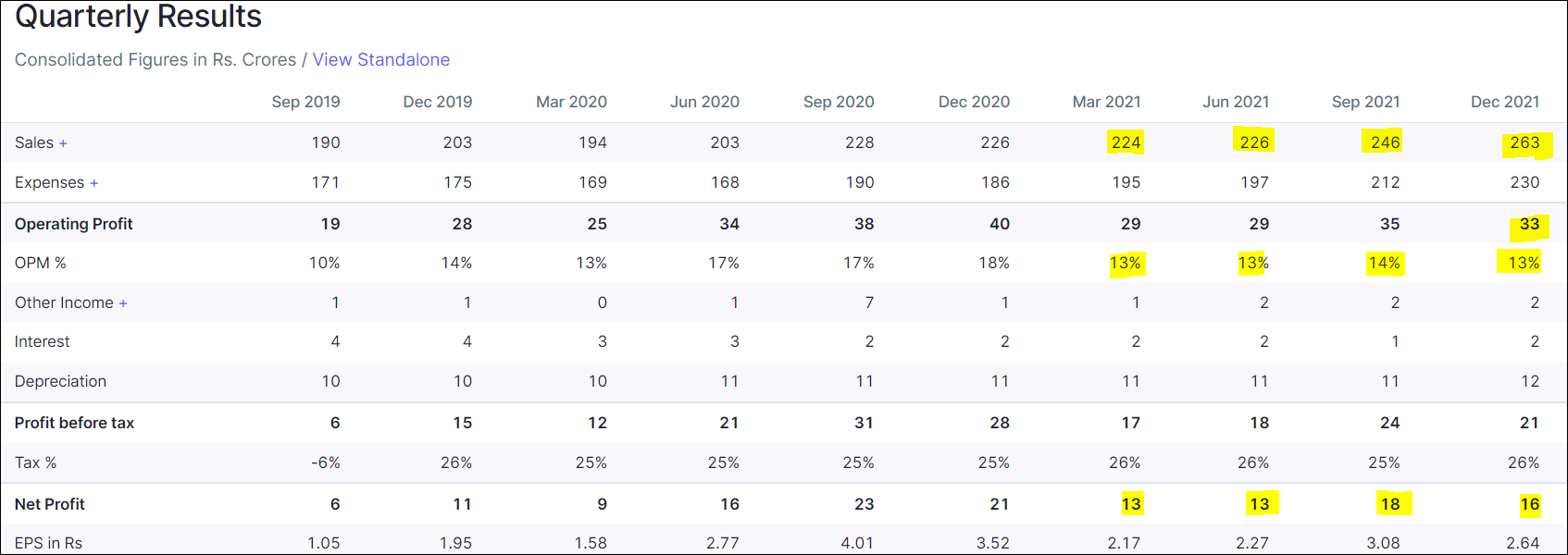

From recent Q2FY22 results,

Highlights

- Top-line growth moderates on high base; margins affected by higher raw material prices

-Company to increase manufacturing capacity, enhance distribution reach

-To further increase price, control costs; retains FY22 margin guidance

-Well placed to outperform industry. Valuations at discount to peers

-Advise investors to add the stock

September 2021 quarter performance

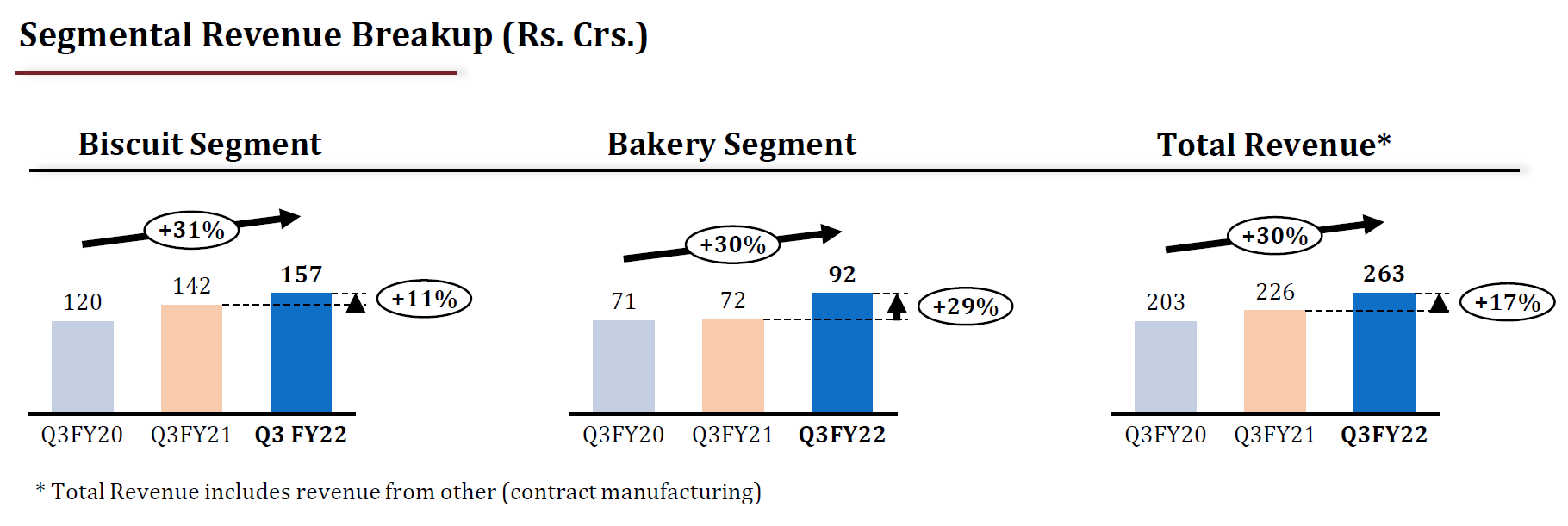

The top-line growth of BFS slowed down marginally to 8 percent year on year (YoY) in the September 2021 quarter from about 12 percent in Q1FY22. The biscuit segment (accounting for about 60 percent revenues) declined by 3 percent in the September 2021 quarter, owing to a high base in Q2FY21.

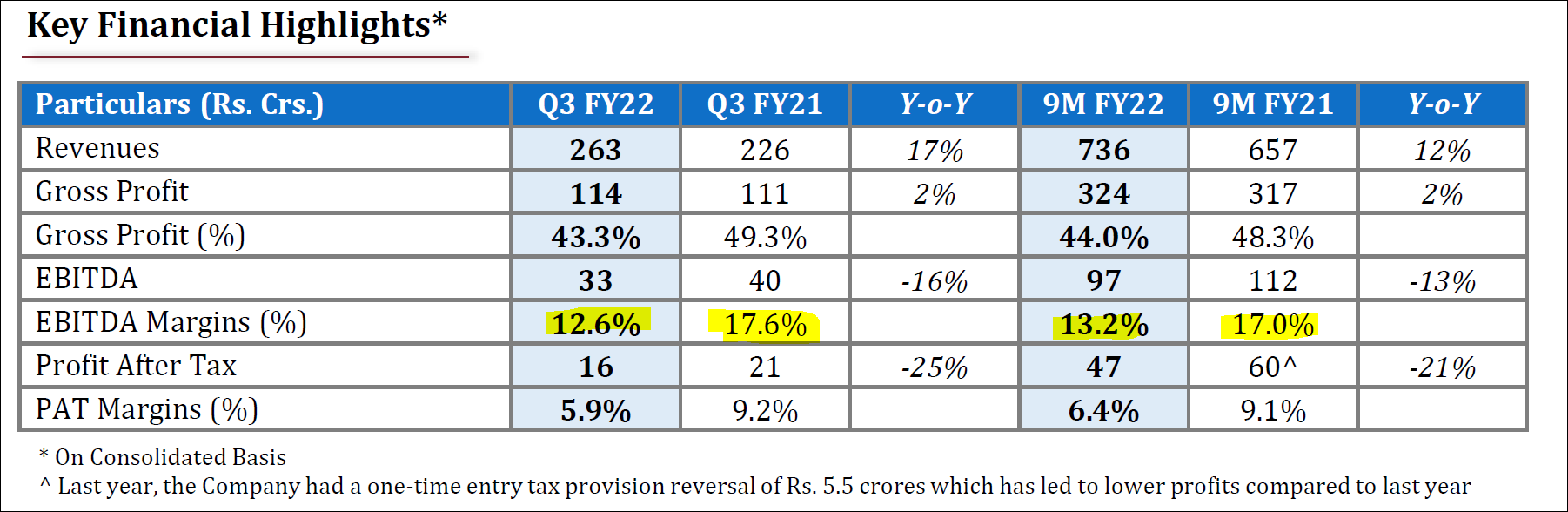

BFS’ gross margins fell about 300 bps on a YoY basis, driven mainly by the steep increase in palm oil prices as well as packaging costs. The EBITDA margins fell by about 240 bps. Net profit declined at a higher rate of 23 percent YoY, as BFS had a one-time gain of Rs 5.5 crore in Q2FY21, owing to entry tax provision reversal.

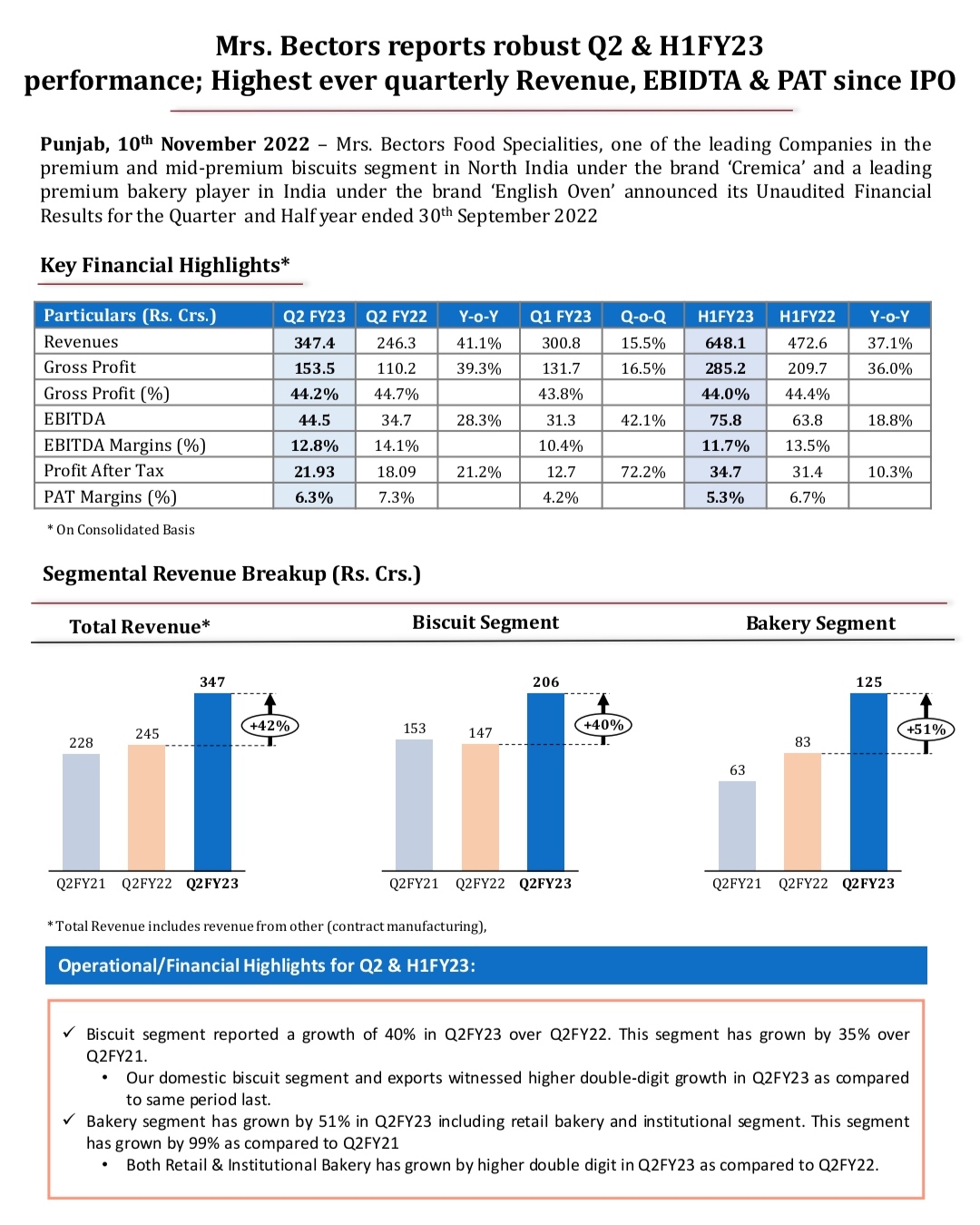

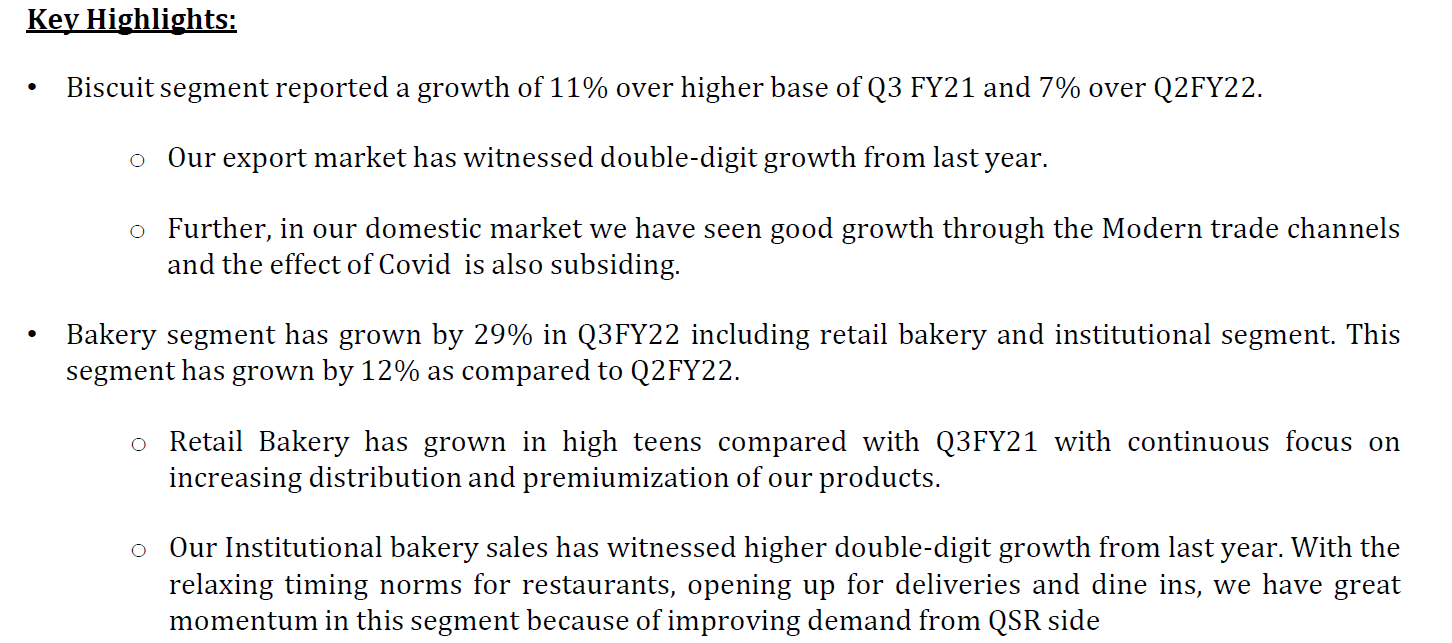

From recent Q3FY22 results,

Management commentary from recent concall -

- Company bought new land in Mumbai for future expansion endeavor

- Outlook is positive, provides 14% sustainable margins

- Capacity utilization is 75-80% part of FY22

- Increase in prices about to kick in for this month.

- Rajpura capacity extension is inline

- New capex expected inline for the next financial year in NaviMumbai.

Details -

Financials

Investors -

stock price is corrected a way higher for the reason increase in raw material prices, however with a promising promotor group, increase in capacity expansion with IPO funds and a promising mega trend theme I could think of reversal in stock price.

Disc: Invested at 350 levels